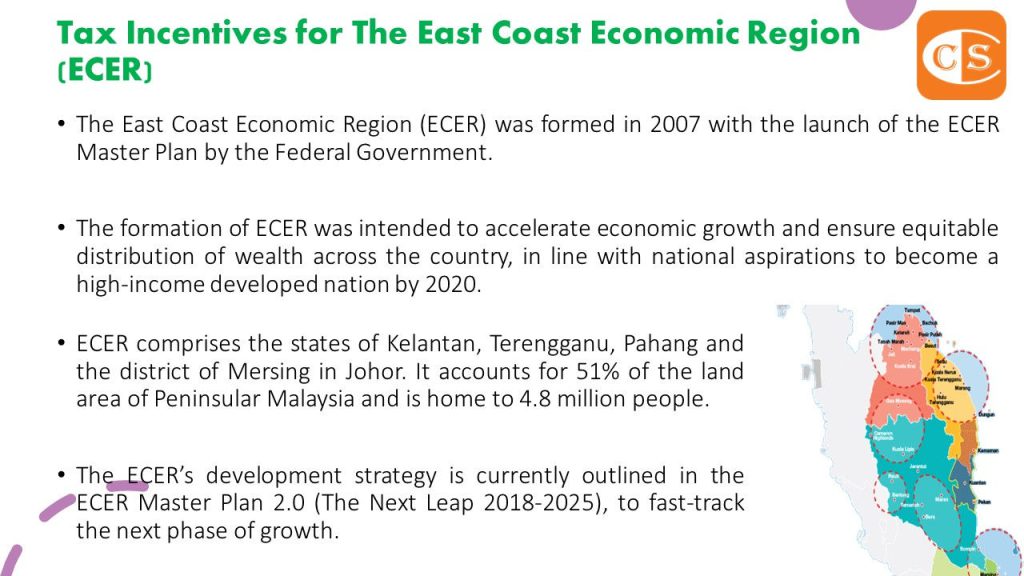

1. The East Coast Economic Region (ECER) was formed in 2007 with the launch of the ECER Master Plan by the Federal Government.2. The formation of ECER was intended to accelerate economic growth and ensure equitable distribution of wealth across the country, in line with national aspirations to become a high-income developed nation by 2020.

3. As a result, the government has provided tax incentives for the ECER

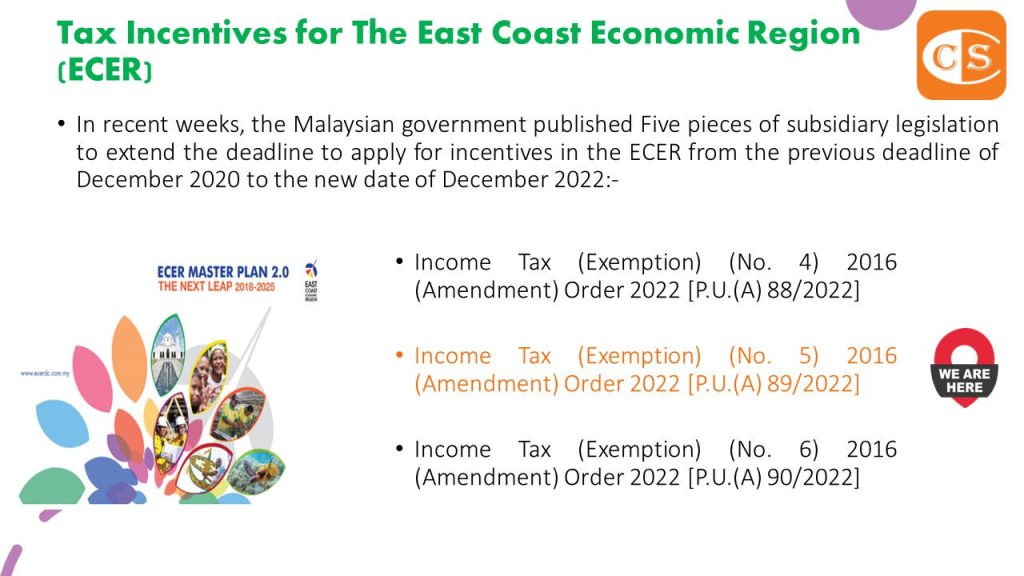

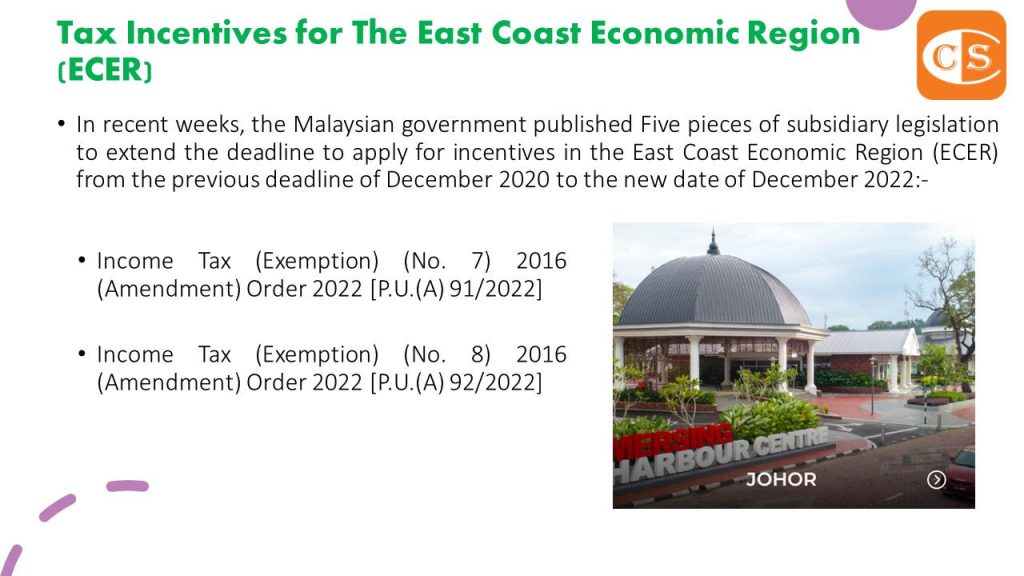

4. In recent weeks, the Malaysian government published Five pieces of subsidiary legislation to extend the deadline to apply for incentives in the ECER from the previous deadline of December 2020 to the new date of December 2022:-

👉 Income Tax (Exemption) (No. 4) 2016 (Amendment) Order 2022 [P.U.(A) 88/2022]

👉 Income Tax (Exemption) (No. 5) 2016 (Amendment) Order 2022 [P.U.(A) 89/2022]

👉 Income Tax (Exemption) (No. 6) 2016 (Amendment) Order 2022 [P.U.(A) 90/2022]

👉 Income Tax (Exemption) (No. 7) 2016 (Amendment) Order 2022 [P.U.(A) 91/2022]

👉 Income Tax (Exemption) (No. 8) 2016 (Amendment) Order 2022 [P.U.(A) 92/2022]

👉 To Download All – https://t.me/YourAuditor/2928

5. Under the Income Tax (Exemption) (No. 5) Order 2016 (‘P.U.(A) 158/2016’), a qualifying person is exempted from paying income tax on statutory income derived from a special qualifying activity that is equal to the rate of allowance specified by the Minister, which shall not be less than 60% and not more than 100% of the qualifying capital expenditure incurred by the qualifying person for such period of consecutive years as the Minister may determine.

6. Join our Telegram – https://t.me/YourAuditor

🌻🌻🌻🌻🌻🌻🌻🌻

1. 东海岸经济区(ECER)于2007年随着联邦政府推出东海岸经济区总体规划而成立。

2. 组建东海岸经济区的目的是为了加速经济增长,确保全国财富的公平分配,以符合国家在2020年成为高收入发达国家的愿望。

3. 因此,政府为东海岸经济区提供了税收激励措施

4. 几周前,马来西亚政府在宪报颁布了5项附属立法,将申请东海岸经济区 (ECER) 税收优惠措施的截止日期从之前的 2020 年 12 月延长至 2022 年 12 月:-

👉 2016年所得税(豁免)(第4号) 2022年(修正)指令 [P.U.(A)88/2022]

👉 2016年所得税(豁免)(第5号) 2022年(修正)指令 [P.U.(A)89/2022]

👉 2016年所得税(豁免)(第6号) 2022年(修正)指令 [P.U.(A)90/2022]

👉 2016年所得税(豁免)(第7号) 2022年(修正)指令 [P.U.(A)91/2022]

👉 2016年所得税(豁免)(第8号) 2022年(修正)指令 [P.U.(A)92/2022]

👉 下载 – https://t.me/YourAuditor/2928

5. 2016年所得税(豁免)(第5号) 指令 (“P.U.(A)158/2016“) 规定,符合条件的人士从特殊合格活动中获得的法定收入可免交所得税,该收入相当于部长规定的津贴率,该津贴率应不低于合格者在部长可能确定的连续几年内产生的合格的资本支出的60%,也不高于100%。

6. 加入 Telegram 群 – https://t.me/YourAuditor

🌼🌼🌼🌼🌼🌼🌼🌼🌼🌼