Update: The Ismail Sabri Government Budget is no longer applicable. Malaysia’s national budget for 2023 was re-tabled again in February 2023.

To Download Revised Budget 2023 Speech and some other related publications – https://www.ccs-co.com/post/budget-2023-malaysia-madani

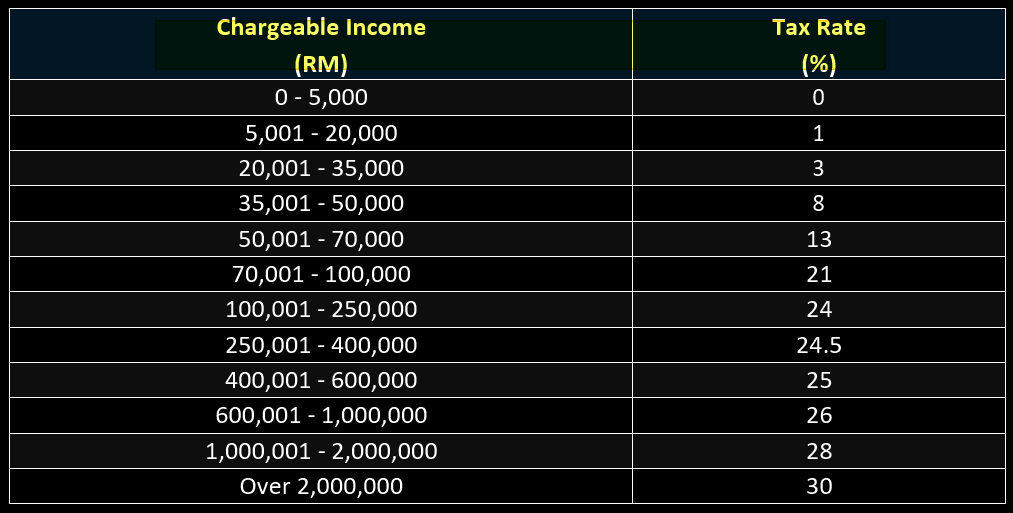

Current Position

Tax is levied on the chargeable income, i.e. on the amount remaining after deducting from the total income all personal reliefs.

A graduated rate of tax is applied to the chargeable income of resident individual taxpayers, starting from 0% (on the first RM5,000) to a maximum of 30% (on chargeable income exceeding RM2,000,001) with effect from YA 2020 onwards.

This tax rate ranges from 0% (on the first RM5,000) to a maximum of 30% (on taxable income exceeding RM2,000,001). From the Assessment Year 2016 to the Assessment Year 2019, the maximum tax rate was 28% on chargeable income that was greater than RM1,000,000.

From the year of assessment 2021, the following are the income tax rates:

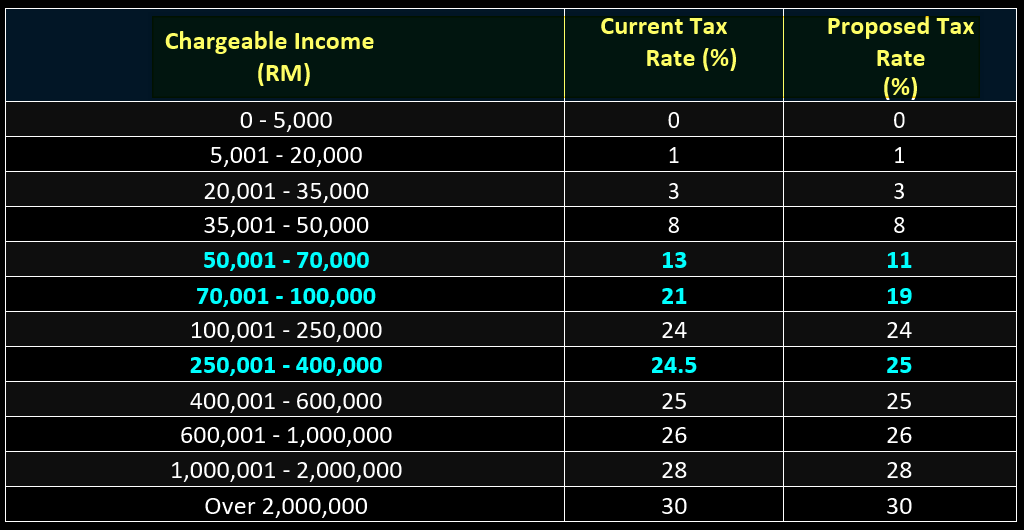

Proposal

Reduction of Tax Rate

It is proposed that the resident individual income tax rate be decreased by 2% points for each chargeable income band between RM50,001 and RM100,000 in order to address the high cost of living and to improve the amount of income that can be spent freely by Rakyat with middle-incomes.

Rises in the Tax Rates

It has been suggested that the individual income tax rate for resident individuals who fall within the chargeable income band of RM250,001 to RM400,000 should be increased by 0.5% points.

Here’s a look at how the proposed tax rate stacks up against the current tax rate on individual income:

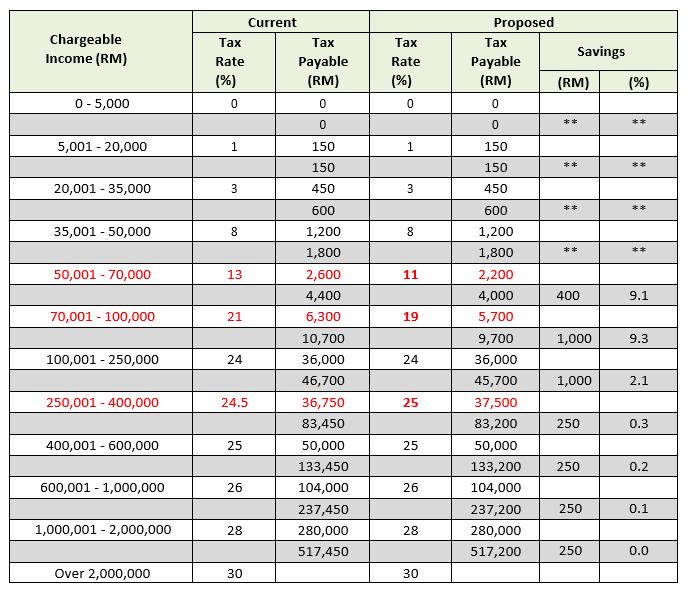

The following are illustrations of how individuals’ income taxes can be reduced due to rate changes:

Note: ** not relevant

Effective Date

From the year of assessment 2023.

Example 1

Nadia, who is resident in Malaysia for the year 2023, as a Finance Director, she has employment income of RM96,000 for the year ended 31.12.2023.

In that year, she made the following contributions to :

- EPF – RM 10,560

- SOCSO – RM 297

- EIS – RM 97.20

Nadia does not has any other tax reliefs.

Computation of Nadia’s Chargeable Income for YA 2023

As Nadia –

- is resident in Malaysia;

- is entitled to a deduction for self and dependent relatives under paragraph 46(1)(a) of the ITA; and

- has chargeable income exceeding RM35,000

she is not entitled to the personal rebate of RM400 for YA 2023.

Income Tax Payable by Nadia for YA 2023

Because the tax rate has been lowered, Nadia will pay less income tax on the same amount of Income, which will result in an increase of RM653 in the amount of money that Nadia has available to spend.

Example 2

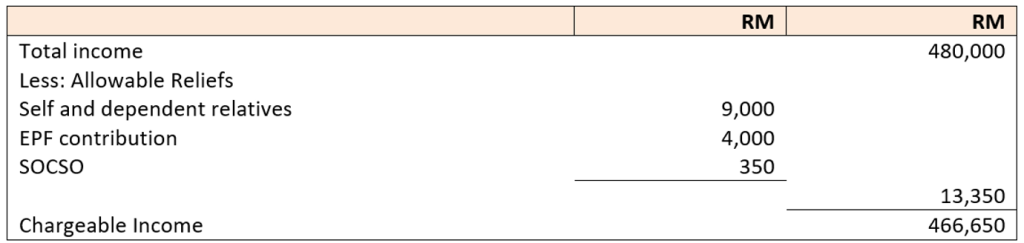

Cindy, who is resident in Malaysia for the year 2023, as a CFO, she has employment income of RM480,000 for the year ended 31.12.2023.

In that year, she made the following contributions to :

- EPF – RM 52,800

- SOCSO – RM 297

- EIS – RM 97.20

Cindy does not has any other tax reliefs.

Computation of Cindy’s Chargeable Income for YA 2023

As Cindy –

- is resident in Malaysia;

- is entitled to a deduction for self and dependent relatives under paragraph 46(1)(a) of the ITA; and

- has chargeable income exceeding RM35,000

she is not entitled to the personal rebate of RM400 for YA 2023.

Income Tax Payable by Cindy for YA 2023

Cindy’s circumstance is special since she benefits from both the tax rate reduction and the 0.5% tax rate rise on a portion of her income as a result of her high income.

Nevertheless, Cindy still saves RM250 in income tax for the same salary, providing her with an extra RM250 in spending money.

Example 3

Lala, who is resident in Malaysia for the year 2023, as an Accounts Executive, she has employment income of RM54,000 for the year ended 31.12.2023.

In that year, she made the following contributions to :

- EPF – RM 5,940.00

- SOCSO – RM 267.00

- EIS – RM 106.80

Lala does not has any other tax reliefs.

Computation of Lala’s Chargeable Income for YA 2023

As Lala –

- is resident in Malaysia;

- is entitled to a deduction for self and dependent relatives under paragraph 46(1)(a) of the ITA; and

- has chargeable income exceeding RM35,000

she is not entitled to the personal rebate of RM400 for YA 2023.

Income Tax Payable by Lala for YA 2023

In terms of earning power, the social classes in Malaysia are classified into three different income classifications – B40, M40, and T20.

B40 is the Bottom 40% of the Malaysian household income. They earn less than RM4,850 per month.

Lala’s income falls within this category, and it is clear that the proposed individual income tax rate has no benefit for her.

But, during the Budget 2023 speech, Tengku Zafrul said that due to the government’s concern for the poor and B40, cash assistance under the Department of Social Welfare and BKM for the year 2023 will exceed RM10 billion.

To Download Budget 2023 Speech and some other related publications – https://t.me/YourAuditor/3276

Our website's articles, templates, and material are solely for reference. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Any reliance on such information is therefore strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/