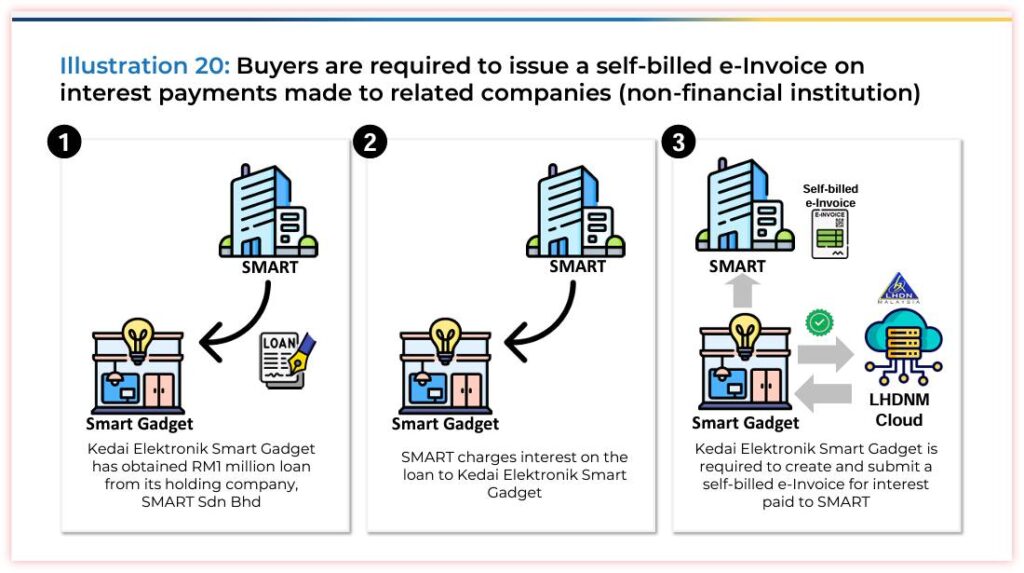

Example based on Illustration 20:

Tech Grow Solutions Sdn Bhd, a subsidiary company, has obtained a loan of RM1,000,000 from its holding company, Innovate Tech Berhad.

The loan details are as follows:

– Loan amount: RM1,000,000

– Interest rate: 5% per annum

– Loan tenure: 3 years

– Interest payment: Made annually

In this scenario:

1. Innovate Tech Berhad (holding company) provides the loan to Tech Grow Solutions Sdn Bhd (subsidiary).

2. Tech Grow Solutions Sdn Bhd is required to create and submit a self-billed e-Invoice for the interest paid to Innovate Tech Berhad.

3. For the first year, Tech Grow Solutions Sdn Bhd would issue a self-billed e-Invoice for RM50,000 (5% of RM1,000,000) to Innovate Tech Berhad.

Advice to taxpayers:

1. Understand the requirement: Recognize that interest payments to related companies (non-financial institutions) require the issuance of self-billed e-Invoices by the borrower.

2. Timing of self-billed e-Invoices: May issue the self-billed e-Invoice when the interest payment is due or paid, whichever is earlier, in line with your accounting method (accrual or cash basis).

3. Accurate calculations: Ensure the interest amount is calculated correctly based on the loan agreement terms.

4. Proper documentation: Maintain a copy of the loan agreement and any other relevant documents to support the self-billed e-Invoices.

5. Separate from principal: Only issue self-billed e-Invoices for the interest portion, not for repayments of the principal amount.

6. Consistent practice: If interest is paid regularly (e.g., monthly, quarterly), establish a routine for issuing self-billed e-Invoices at the same intervals.

7. System integration: Consider integrating the self-billing process into your accounting system to automate and streamline the process.

8. Clear communication: Ensure both the borrowing and lending entities understand the self-billing arrangement for interest payments.

9. Tax implications: Be aware of any tax implications related to inter-company loans and interest payments.

10. Transfer pricing considerations: Ensure the interest rate is at arm’s length and complies with transfer pricing regulations.

11. Handle changes properly: If there are any changes to the loan terms (e.g., interest rate changes), reflect these accurately in subsequent self-billed e-Invoices.

12. Compliance checks: Regularly verify that your self-billed e-Invoices meet all the requirements set by LHDNM for format and content.

13. Group-level consistency: If you’re part of a larger group of companies, ensure consistent treatment of inter-company loan interest across the group.

14. Reconciliation: Periodically reconcile the self-billed e-Invoices issued against the loan agreement and actual payments made.

15. Staff training: Ensure relevant finance staff understand the process and requirements for issuing self-billed e-Invoices for inter-company interest.

16. Seek professional advice: If you’re unsure about any aspects of self-billing for inter-company interest, consult with a tax professional or LHDNM.

17. Stay informed: Keep up to date with any changes in e-Invoice or tax regulations that might affect inter-company loan arrangements.

By following these guidelines, companies can ensure they’re correctly handling e-Invoice requirements for interest payments on inter-company loans, maintaining compliance with tax regulations while accurately documenting these financial transactions.

基于例题20:

子公司 Tech Grow Solutions Sdn Bhd 从其控股公司 Innovate Tech Berhad 获得了100万令吉的贷款。

贷款详情如下:

– 贷款金额:100万令吉

– 年利率:5%

– 贷款期限:3年

– 利息支付:每年支付

在这种情况下:

1. Innovate Tech Berhad (控股公司) 向 Tech Grow Solutions Sdn Bhd (子公司) 提供贷款。

2. Tech Grow Solutions Sdn Bhd 需要为支付给 Innovate Tech Berhad 的利息开具并提交自开电子发票。

3. 在第一年,Tech Grow Solutions Sdn Bhd 将向 Innovate Tech Berhad 开具金额为5万令吉 (100万令吉的5%) 的自开电子发票。

给纳税人的建议:

1. 了解要求:认识到向关联公司(非金融机构)支付利息时,借款人需要开具自开电子发票。

2. 自开电子发票的时间:根据您的会计方法 (权责发生制或现金制),在利息到期或支付时开具自开电子发票,以较早者为准。

3. 精确计算:确保根据贷款协议条款正确计算利息金额。

4. 妥善保存文件:保留贷款协议和其他相关文件的副本,以支持自开发票。

5. 与本金分开:仅针对利息部分开具自开发票,不针对本金还款部分。

6. 保持一致的做法:如果利息是定期支付的 (例如每月、每季度),则应建立以相同间隔开具自开电子发票的常规。

7. 系统整合:考虑将自开电子发票流程整合到您的会计系统中,以实现流程的自动化和简化。

8. 清晰的沟通:确保借款和贷款实体都了解利息支付的自开票安排。

9. 税务影响:注意公司间贷款和利息支付相关的税务影响。

10. 转让定价注意事项:确保利率符合公平交易原则并符合转让定价规定。

11. 正确处理变更:如果贷款条款有任何变更 (例如利率变更),请在后续的自开电子发票中准确反映这些变更。

12. 合规性检查:定期验证自开电子发票是否符合LHDNM规定的格式和内容要求。

13. 集团层面的一致性:如果您隶属于一个大型集团公司,请确保集团内公司间贷款利息的处理方式保持一致。

14. 核对:定期根据贷款协议和实际付款情况核对开具的自开电子发票。

15. 员工培训:确保相关财务人员了解开具公司间利息自开发票的程序和要求。

16. 寻求专业意见:如果您对开具公司间利息自开电子发票有任何疑问,请咨询税务专业人士或LHDNM。

17. 随时了解最新信息:随时了解可能影响公司间贷款安排的电子发票或税务法规的任何变化。