Starting 1 July 2025, rental or leasing services officially become a taxable service under the Malaysian Service Tax Act 2018.

If your business rents out shops, offices, machines, event spaces, or equipment — you may be affected.

Here’s what the public needs to know:

1. When did rental and leasing become taxable?

Any person providing rental or leasing services, once their total taxable services exceed the threshold.

![]() 4. When to register?

4. When to register?

Based on Section 12 & 13 of the Service Tax Act 2018:

- You must register once your total taxable services exceed RM1,000,000 over any 12-month period (past or expected).

- The application must be submitted by the last day of the following month.

- If you don’t apply, Customs has the power to register you automatically, and late registration is an offence.

![]() 5. What if your customer is exempted from paying tax (e.g. sublet cases)?

5. What if your customer is exempted from paying tax (e.g. sublet cases)?![]() Under the Service Tax (Amendment) Regulations 2019, Regulation 10(1A), when you issue an invoice to someone exempted under Section 34, your invoice/e-invoice must clearly state:

Under the Service Tax (Amendment) Regulations 2019, Regulation 10(1A), when you issue an invoice to someone exempted under Section 34, your invoice/e-invoice must clearly state:

- Their name and address

- Their SST registration number

- The amount of service tax exempted

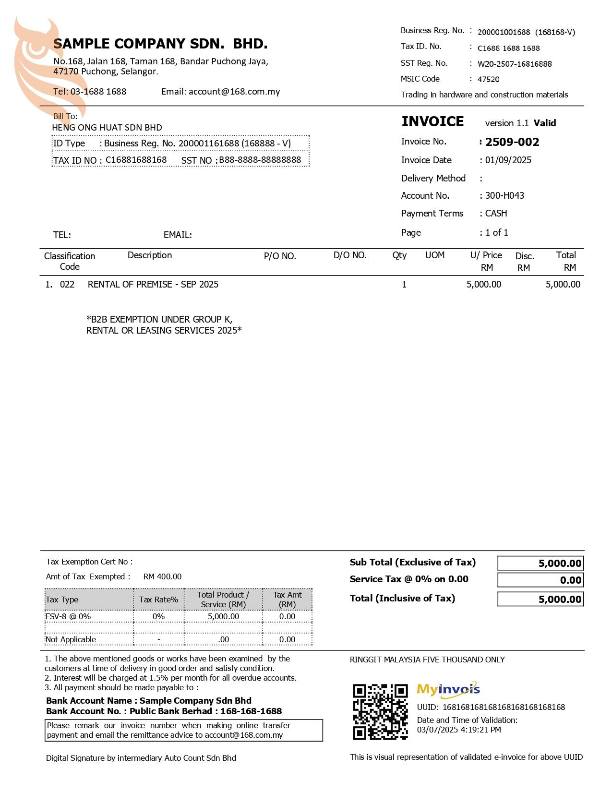

![]() 6. What does a compliant e-Invoice look like?

6. What does a compliant e-Invoice look like?

The sample e-Invoice that shows 8% service tax includes:![]() Taxpayer details

Taxpayer details![]() Customer SST registration number

Customer SST registration number![]() Service description and period

Service description and period![]() Proper classification and breakdown of SST

Proper classification and breakdown of SST![]() Exemption details (if applicable)

Exemption details (if applicable)

![]() This format meets both LHDN’s e-Invoice standards and the Customs SST compliance requirements.

This format meets both LHDN’s e-Invoice standards and the Customs SST compliance requirements.

If the Supplier shares a visual representation of the e-Invoice:

Some data fields (e.g., TIN, MSIC Code, etc.) can be excluded.

However, the QR code must be embedded in the visual representation.

In short:

If you rent, lease, or sublet commercial property or equipment — and your business crosses RM1 million in rental income — you must register for SST, charge 8%, and issue compliant e-Invoices from 1 July 2025 onwards.

【电子发票 + 8% 服务税:出租/租赁行业一定要懂的7件事】

从 2025年7月1日起,出租或租赁服务正式被列为马来西亚的应税服务。

无论你是出租商店、办公室、活动场地、设备或机械 —— 你都可能需要缴 SST 服务税,并开具电子发票(e-Invoice)。

以下是大众一定要知道的重点:

![]() 4. 什么时候要注册?

4. 什么时候要注册?

根据《服务税法令》第 12 和 13 条:

- 一旦达到门槛,你必须在接下来的月底前申请注册;

- 如果你没有注册,关税局有权强制注册你;

- 拒绝注册或延迟注册,属于违法行为。

![]() 5. 如果客户是免税对象(如再转租用途)怎么办?

5. 如果客户是免税对象(如再转租用途)怎么办?![]() 根据 2019年《服务税(修正)条例》第 10(1A) 条,当你的客户是 免征 SST 的公司(如 sublet 情况),你开出的发票/电子发票必须包括:

根据 2019年《服务税(修正)条例》第 10(1A) 条,当你的客户是 免征 SST 的公司(如 sublet 情况),你开出的发票/电子发票必须包括:

- 客户的名称与地址

- 客户的 SST 注册号码

- 豁免的服务税金额

![]() 6. 什么是合格的电子发票?

6. 什么是合格的电子发票?

这张含 8% 服务税的电子发票样本内容包括:![]() 服务提供者资料

服务提供者资料![]() 客户 SST 注册号

客户 SST 注册号![]() 出租服务详情(项目与期间)

出租服务详情(项目与期间)![]() SST 明细与分类

SST 明细与分类![]() 若有豁免,也列明豁免金额

若有豁免,也列明豁免金额

![]() 它同时符合 关税局 SST 发票规定 和 LHDN 电子发票架构标准,合规无误。

它同时符合 关税局 SST 发票规定 和 LHDN 电子发票架构标准,合规无误。

7. 供应商分享视觉呈现的电子发票

某些数据字段(例如,纳税人识别号、MSIC 代码等)可以被排除。

然而,二维码必须嵌入在视觉表示中。

![]() 小结:

小结:

只要你的公司涉及出租/租赁商用产业、机械、设备等,并且年租金收入超过 RM1,000,000, 2025年7月1日开始,你就得着手注册征税、开电子发票,并依法报税!

Credit To Varrenz Seok – by providing a sample of e-invoice