The Service Tax reintroduced on 1 September 2018, is a consumption tax administered under the Service Tax Act 2018 and its subsidiary legislation.

Service tax is imposed on prescribed services known as “taxable services”.

A person who provides taxable services exceeding a specified threshold of taxable service value must register under the Service Tax Act 2018 and is known as a “registered person” who must charge service tax on the taxable services provided to their customers.

The Food and Beverage Guidelines, dated 26 June 2023, have been withdrawn and replaced with the updated Guidelines issued on 16 April 2024 (“latest guidelines“), which can be downloaded below:

This guide is prepared to enhance understanding of the service tax treatment on providing food and beverage services.

The latest guidelines issued by the Royal Malaysian Customs Department (JKDM), provide further clarification on the scope, tax rates, and responsibilities for F&B operators.

Key Points:

- The scope of the Service Tax covers services provided by restaurants, bars, cafeterias, coffee shops, catering services, and food courts with characteristics of a restaurant.

- The threshold for SST registration for F&B operators is exceeding RM1.5 million within a 12-month period.

- The standard service tax rate for the provision of food and beverages is 6%. However, effective March 1, 2024, services other than food, beverages, telecommunications, parking, and logistics have been increased to 8%.

- Other services provided within the Food and Beverage Area (FBA) such as facility rentals, entertainment, cigarette sales, and alcoholic beverage sales are subject to an 8% rate. Package-related services (e.g., wedding packages) will follow the main service rate of 6%.

- Bakery sales at cake shops and packaged food sales (e.g., at convenience stores) are not subject to SST as they do not have restaurant characteristics. However, franchise counters selling food are subject to SST if the franchisor requires registration.

Calculation Example:

Delicious Burger Restaurant has achieved sales of RM1.6 million in 12 months.

The price of a burger with a drink is RM10.60.

The service tax to be imposed is RM0.60 (RM10 x 6%).

Delicious Burger Price: RM10.00

SST @ 6%: RM0.60

Total: RM10.60

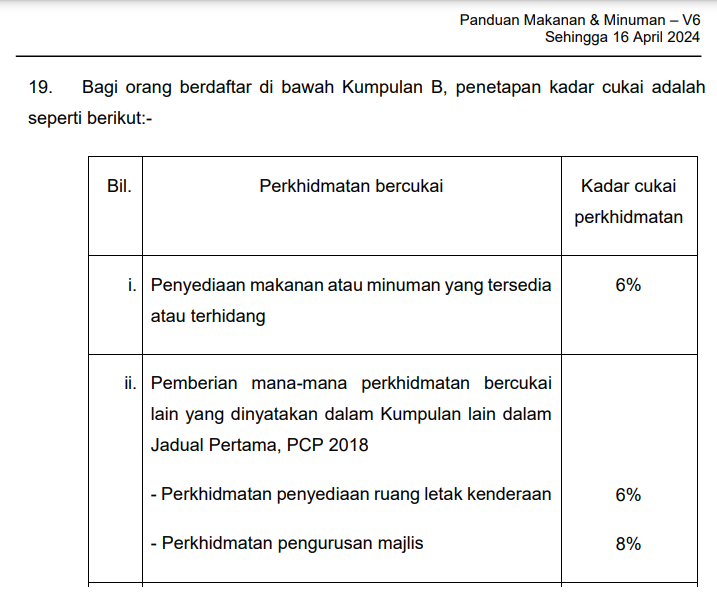

Paragraph 19 of the Food and Beverage Guidelines issued by JKDM touches on the determination of service tax rates for taxable services provided by registered persons under Group B, First Schedule, Service Tax Regulations 2018.

In detail, the prescribed service tax rates are as follows:

1. 6% Rate for:

– Provision of food or beverages that are available or served

– Provision of parking space

– Food and beverage packages including event management

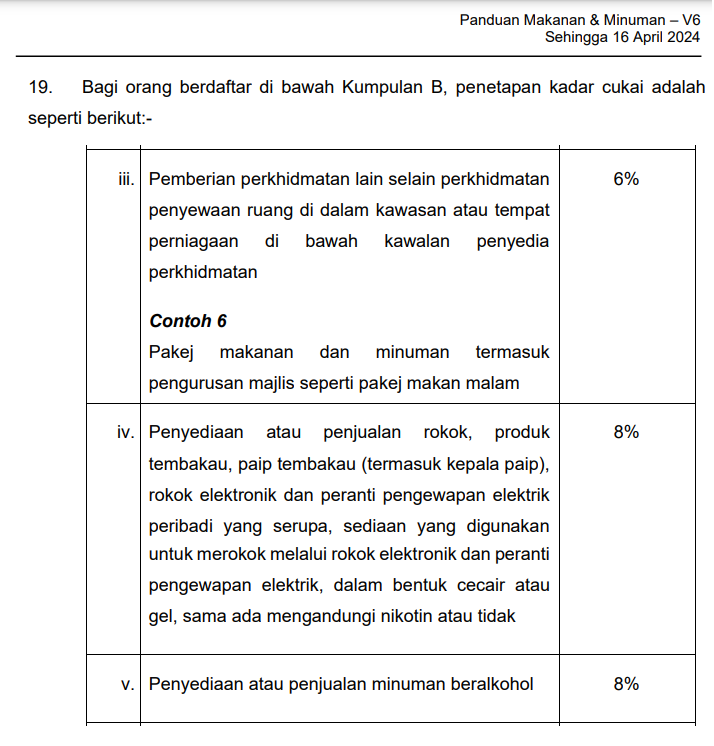

2. 8% Rate for:

- Provision of other services apart from space rental within areas or premises under the control of the service provider. For example, facility rentals, entertainment such as karaoke, amusement parks, live cooking services, and so on.

- Provision or sale of cigarettes, tobacco products, vape, and electronic smoking devices whether containing nicotine or not

- Provision or sale of alcoholic beverages

- Provision or sale of non-alcoholic beverages (e.g., mineral water, canned/bottled/carton drinks)

Although there is a difference in service tax rates between 6% and 8%, the determination of these rates is based on the type of taxable service provided and not subject to the primary service of the food and beverage operator.

However, there is an exception, which is the packaged taxable services provided, will be subject to the service tax rate based on the primary service offered by the registered persons under Group B.

For example, if a restaurant offers a wedding package that includes food, beverages, event management, entertainment, and hall rental, the entire package will be subject to a 6% rate because the primary service offered is the provision of food and beverages.

Therefore, it is important for food and beverage operators registered under SST to clearly understand the types of taxable services provided and the correct tax rates to ensure compliance with the Service Tax Act 2018.

Note to F&B Operators:

– Ensure annual sales value and register for SST if exceeding the threshold value

– Apply tax according to the type of service provided, whether 6% or 8%

– Service tax accounts based on the date of payment received

– Issue tax invoices and file SST-02 returns within the prescribed period

In conclusion, it is important for F&B operators to understand the scope of services, correct tax rates, and comply with the Service Tax Act 2018 requirements to avoid any penalties.

Further information can be obtained through the SST website at the link https://mysst.customs.gov.my or by contacting the Customs Call Center.