Recent changes to the Form C

Recent changes were made to Form C by the Inland Revenue Board in preparation for the YA 2022.

One of the most critical changes is for those businesses participating in transfer pricing arrangements. As a result, the disclosure items have been significantly expanded to cover new areas.

These new areas include stating the characterisation of your company by reference to its functional profile, the business restructuring undertaken by the group during the year, and whether or not your company engages in cash pooling activities, performs any research and development activities, owns any intellectual properties, or participation in cost contribution arrangements,

Concept of Cost Contribution Arrangements (CCAs)

The Malaysian Transfer Pricing Guidelines explain:

A CCA is a framework (in the form of a contractual agreement) agreed upon among business enterprises to share the costs and risks of developing, producing or obtaining assets, services or rights and to determine the nature and extent of the interests of each participant in those assets, services or rights.

- Each participant’s proportionate share of the overall contributions to the arrangement will be consistent with the participant’s proportionate share of the overall expected benefits to be received under the arrangement.

- The participant would be entitled to exploit its interest in the CCA separately as an effective owner, not a licensee.

- Where a taxpayer enters into a CCA with its associated persons, the arrangement should reflect that of an arm’s length arrangement.

In General

In a cost contribution agreement, the participants share the contributions and risks involved in an endeavour.

Types of CCAs

Two types of CCAs are commonly encountered:

- those established for the joint development, enhancement, maintenance, protection or exploitation of intangibles or tangible assets (“development CCAs”); and

- those for obtaining services (“services CCAs”).

While each particular CCA should be considered on its own facts and circumstances, a key difference between these two types of CCAs will often be that the former are expected to create ongoing, future benefits for participants. In contrast, the latter will often create current benefits only.

The characteristics of a CCA

- the arrangement is made between at least two related parties,

- each party’s responsibility for the costs is defined by a formula that the parties have agreed on, and

- each party’s share of the costs must reflect its share of the overall expected benefits to be received under the arrangement.

Example

In Year 1, a multinational group comprised of Company A and Company B decided to develop an intangible, which is anticipated to be highly profitable based on Company B’s existing intangibles, its track record and its experienced research and development staff.

Company A performs, through its own personnel, all the functions expected from an independent entity providing funding for a research and development project:

- including the analysis of the intangible at stake and the anticipated profits that can be derived from the investment, the evaluation of the funding risk,

- including the risk that further investment may be required to complete the project, and of the capacity of Company A to take that risk, and the making of decisions to bear, cover, or mitigate that risk.

The particular intangible in this example is expected to take five years to develop before possible commercial exploitation. If successful is anticipated to have value for 10 years after initial exploitation.

Company A and Company B decide to undertake the development through a CCA.

Under the CCA:

- Company A will provide all funding associated with the intangible development (the development costs are anticipated to be RM100 million per year for 5 years).

- Company B will contribute to using its existing intangibles and will perform and control all activities related to the development, maintenance, and exploitation of the intangible.

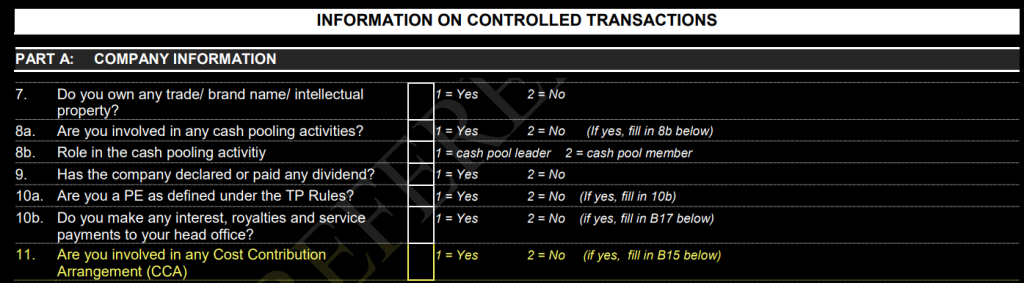

Form C Requires Additional Disclosures

According to the information provided in Section A of the Appendix of Form C for YA 2022, taxpayers who carry out controlled transactions under sections 139 and 140A must disclose: Are they involved in any Cost contribution arrangement (CCA)?

Enter ‘1’ if they are involved in any CCA and disclose the amounts in B15.

Enter ‘2’ if they are not involved in any CCA, or it’s not relevant.

Our website's articles, templates, and material are solely for reference. Although we make every effort to keep the information up to date and accurate, we make no representations or warranties of any kind, either express or implied, regarding the website or the information, articles, templates, or related graphics that are contained on the website in terms of its completeness, accuracy, reliability, suitability, or availability. Any reliance on such information is therefore strictly at your own risk.

Keep in touch with us so that you can receive timely updates |

要获得即时更新,请与我们保持联系

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/