Income Tax (Costs of Renovation and Refurbishment of Business Premise)(Amendment) Rules 2021 – PDF

P.U (A) 481 – Income Tax (Costs of Renovation and Refurbishment of Business Premise)(Amendment) Rules 2021 – As at 27 December 2021

P.U. (A) 381 – Income Tax (Costs of Renovation and Refurbishment of Business Premise)(Amendment) Rules 2020 – As at 28 December 2020

1. On 27 December 2021, the Minister, in the exercise of the powers conferred by paragraph 154(1)(b) read together with paragraph 33(1)(d) of the Income Tax Act 1967 [Act 53], gazetted the Income Tax (Costs of Renovation and Refurbishment of Business Premise)(Amendment) Rules 2021 [P.U. (A) 481].

2. These Rules have effect from the year of assessment 2022 to amend Subrule 3(1) of the Income Tax (Costs of Renovation and Refurbishment of Business Premise) Rules 2020 [P.U. (A) 381/2020]

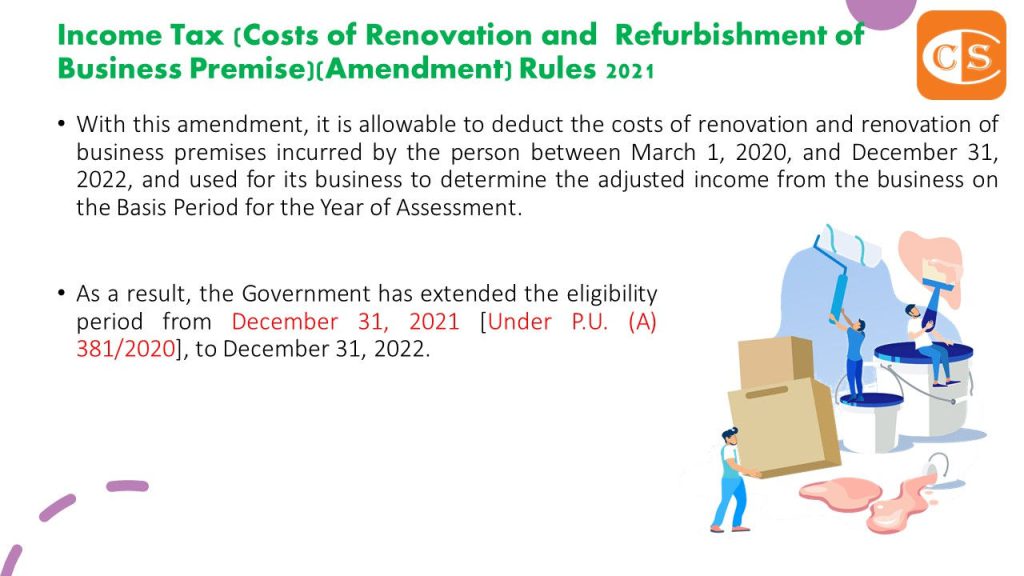

3. With this amendment, it is allowable to deduct the costs of renovation and renovation of business premises incurred by the person between March 1, 2020, and December 31, 2022, and used for its business to determine the adjusted income from the business on the Basis Period for the Year of Assessment.

4. As a result, the Government has extended the eligibility period from December 31, 2021 [Under P.U. (A) 381/2020], to December 31, 2022.

5. Join our Telegram: http://bit.ly/YourAuditor

🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻

1. 2021 年 12 月 27 日,部长行使 1967年所得税法令 [法案53] 第154(1)(b) 段和第33(1)(d)段所赋予的权力,在宪报上颁布了 2021年所得税 (营业场所翻修和翻新费用)(修正案) 细则 [P.U. (A) 481]。

2. 此细则从2022年评估年度起生效,主要是为了修订 2020年所得税(营业场所翻修和翻新费用) 细则 [P.U (A) 381/2020] 第3(1)条例。

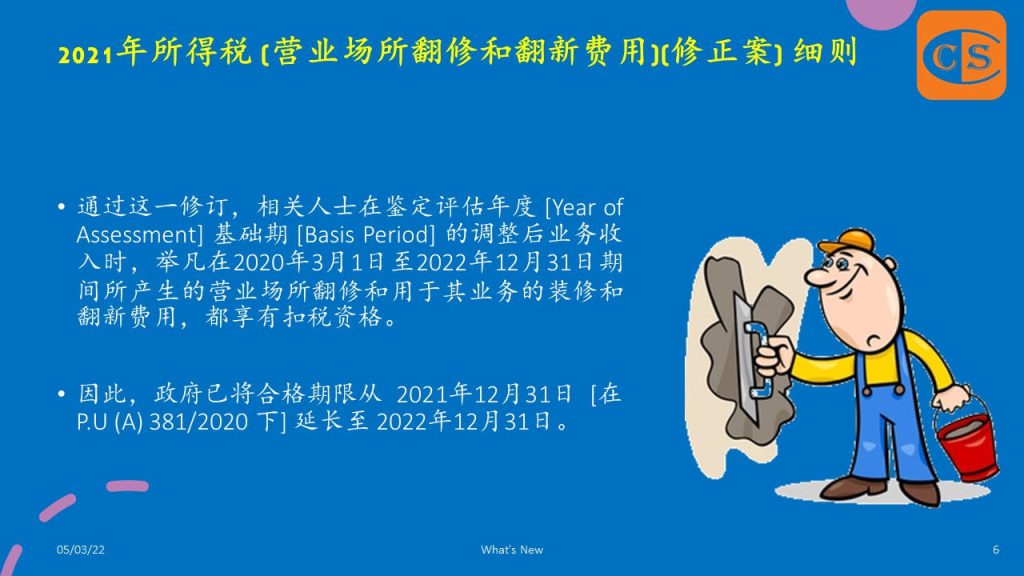

3. 通过这一修订,相关人士在鉴定评估年度 [Year of Assessment] 基础期 [Basis Period] 的调整后业务收入时,举凡在2020年3月1日至2022年12月31日期间所产生的营业场所翻修和用于其业务的装修和翻新费用,都享有扣税资格。

4. 因此,政府已将合格期限从 2021年12月31日 [在 P.U (A) 381/2020 下] 延长至 2022年12月31日。

5. 加入我们的 Telegram: http://bit.ly/YourAuditor

🌼🌼🌼🌼🌼🌼🌼🌼🌼🌼