IRBM’s Response to CTIM on the Tax Corporate Governance Framework (TCGF) & TCGF Guidelines

The new Tax Corporate Governance Framework (“TCGF“), dated April 11, 2022, as well as the Guidelines for the TCG Framework (Guidelines), has been published on the website of the Inland Revenue Board of Malaysia (“IRBM”). The TCG Framework and these Guidelines are intended to be read in conjunction with one another. For further information, see […]

IRBM’s Response to CTIM on e-C 2022 (3)

Regarding Form e-C 2022, CTIM has offered feedback and comments to the Inland Revenue Board of Malaysia (IRBM). The Inland Revenue Board of Malaysia issued its response on 29 July 2022 and 2 August 2022, respectively. Despite this, on 11 August 2022, CTIM provided IRBM with additional feedback and comments on the form e-C 2022 […]

IRBM’s Response to CTIM on e-C 2022 (2)

We would like to inform you that the Inland Revenue Board of Malaysia (IRBM) has disseminated a revised version of the Company Return Form (Form C) for the Year of Assessment 2022. To download a PDF copy of the return – https://t.me/YourAuditor/3259 Chartered Tax Institute of Malaysia’s Previous Feedback Regarding Form e-C 2022, the Chartered […]

Double Tax Deduction for the Cost of Detection Test of Covid-2019

In the exercise of the powers conferred by paragraph 154(1)(b) read together with paragraph 33(1)(d) of the Income Tax Act 1967 [Act 53], the Minister, on September 9, 2022, gazetted the Income Tax (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) (Amendment) Rules 2022 (P.U. […]

IRBM’s Response to CTIM on Profiling Issues

According to what the CTIM has been told, the Intelligence and Profiling Department of the Inland Revenue Board of Malaysia (IRBM) has been making requests for information involving tax practitioners and their clients (such as the names, identity card numbers, tax reference numbers, contact numbers, etc.) to gather data from tax practitioners and other industries […]

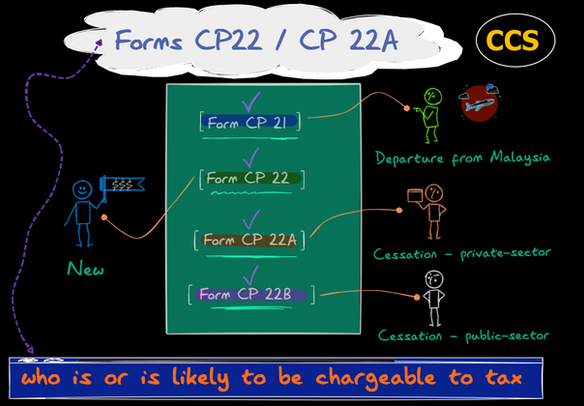

IRBM’s Response to CTIM on Forms CP 22 / CP 22A

Mandatory adoption of Prescribed Forms CP 21, CP 22, CP 22A and CP 22B effective from 1 January 2022 Effective January 1, 2021, under the amendments to subsections 83 (2), (3), and (4) of the Income Tax Act 1967, Forms CP 21, CP 22, CP 22A, and CP 22B must be submitted by the employers […]

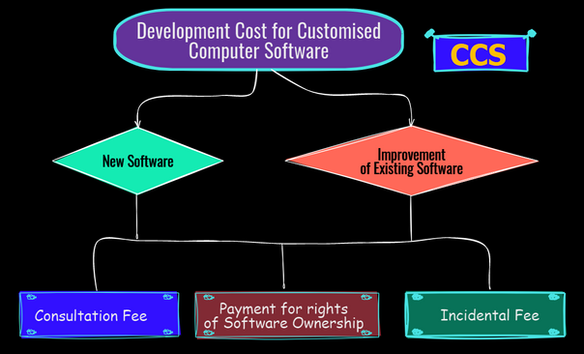

IRBM’s Response to CTIM’s Development Cost for Customised Computer Software

Income Tax (Capital Allowance) (Development Cost for Customised Computer Software) Rules 2019 On 3 October 2019, the Minister, in the exercise of the powers conferred by paragraphs 154(1)(b), 33(1)(d) and paragraphs 10 and 15 of Schedule 3 to the Income Tax Act 1967 [Act 53], gazetted the Income Tax (Capital Allowance) (Development Cost for Customised […]

The latest updates and issues in claiming RA for Manufacturing Activities

The Reinvestment Allowance (RA) is an incentive provided to Malaysian resident companies involved in the manufacturing industry and specified agriculture sector. The purpose of this incentive is to encourage these companies to reinvest and grow their companies. Eligibility to Claim Reinvestment Allowance For these companies to be eligible for the RA incentive, they must have […]

LHDN Responses to CTIM Comments on FAQ on 2% Withholding Tax Deducted from Payment by Payer Company

1. Following the publication of a frequently asked question (FAQ) by the Inland Revenue Department (IRD) on the 2% withholding tax deducted from payments made by payer companies to agents, dealers, and distributors, the CTIM wrote to the Inland Revenue Department on 5 April 2022 requesting clarification on a number of points that had been […]

LHDNM responses to clarification sought on FAQ on deferment of CP204 & CP500 installments

LHDNM Responses – Deferment of CP204 & CP500 payment 12