Section 107C of the Malaysian Income Tax Act 1967 outlines the rules and procedures for companies, limited liability partnerships, trust bodies, and co-operative societies to estimate their tax payable and make payments by instalments.

Here’s a summary of the key points from this section:

1. **Annual Estimate**: Every company, limited liability partnership (LLP), trust body, and co-operative society must estimate their tax payable for each year of assessment to the Director General (subsection 107C(1)).

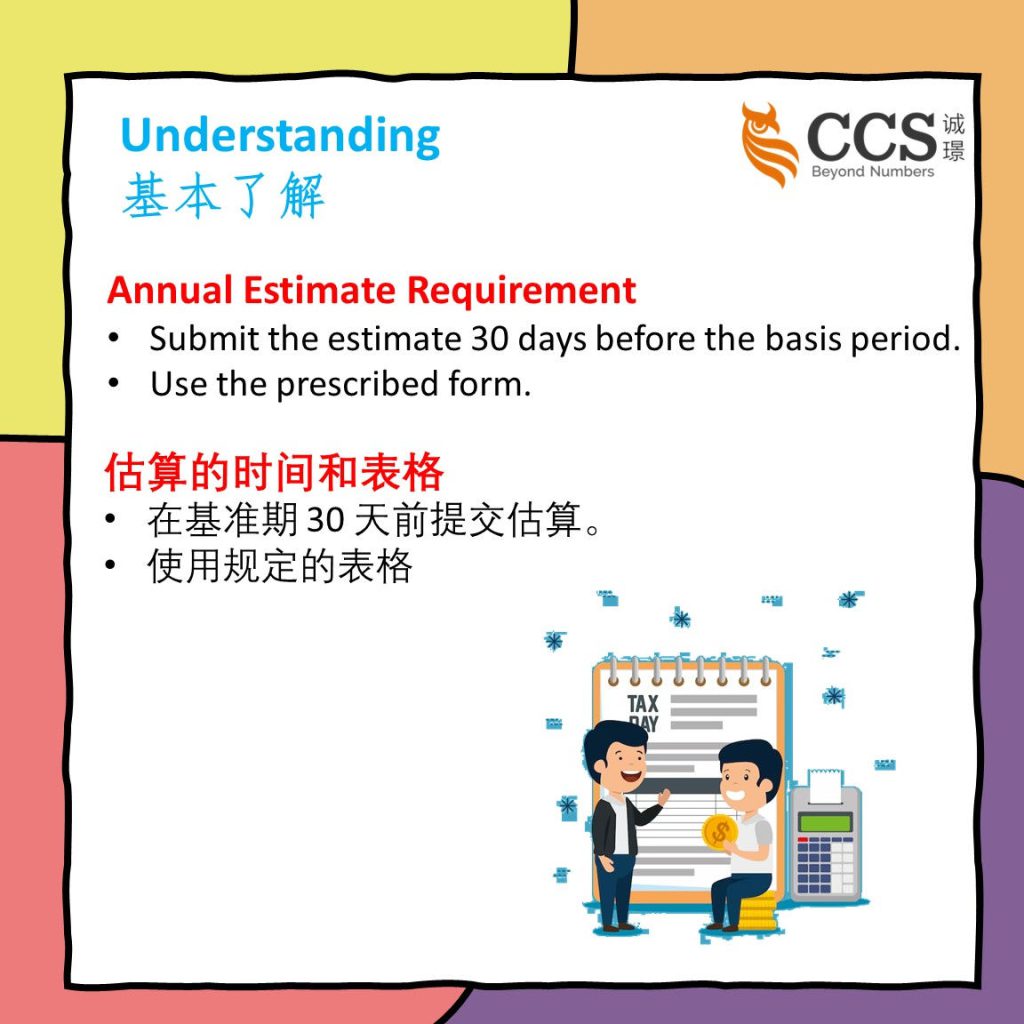

2. **Timing and Form**: The estimate of tax payable should be made in the prescribed form and submitted to the Director General not later than thirty days before the beginning of the basis period for that year of assessment (subsection 107C(2)).

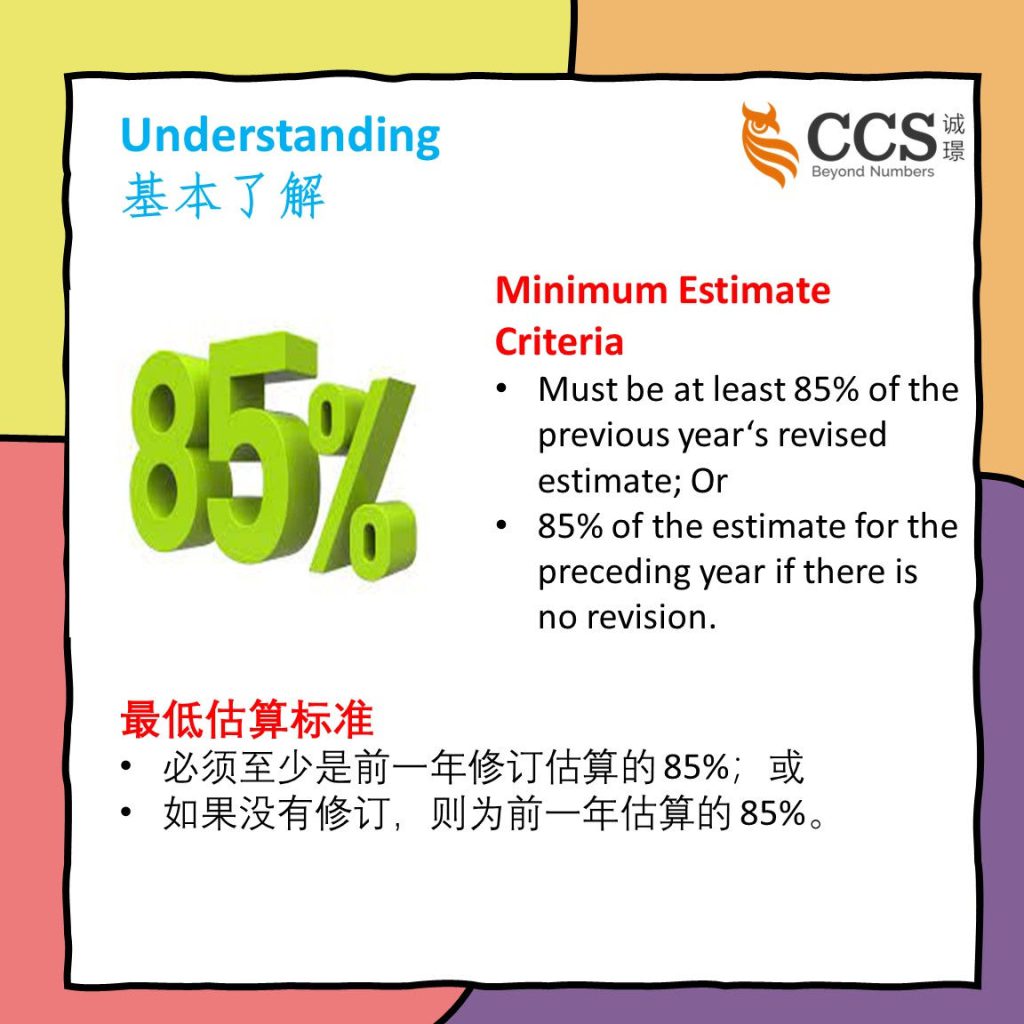

3. **Minimum Estimate**: The estimate should not be less than 85% of the revised estimate of tax payable for the immediately preceding year of assessment, or if no revised estimate is furnished, it should be at least 85% of the estimate for the immediately preceding year (subsection 107C(3)).

4. **New Companies**: For new companies (other than a company to which subsection (4A) applies), limited liability partnerships, trust bodies, or co-operative societies commencing operations during a year of assessment, there are specific requirements and timeframes for providing estimates (subsection 107C(4)). Section 107C(4) Explanation:

When a company, limited liability partnership, trust body, or co-operative society starts operating in a year of assessment, and the basis period for that year is not less than six months, Section 107C(4) comes into play.

This section establishes two key requirements for these new entities:

a) The estimate of their tax payable for that year of assessment should be made in the prescribed form and furnished to the Director General within three months from the commencement date of operations.

b) Subsections (2) and (3) of Section 107C (which pertain to the timing and minimum estimate) shall apply to the company beginning from the second year of assessment.

Illustrative Example:

Let’s say a new company in Malaysia, XYZ Sdn Bhd, started its operations on 1 April 2023.

This is the beginning of its basis period for the year of assessment 2023.

Here’s how Section 107C(4) would apply to XYZ Sdn Bhd:

- XYZ Sdn Bhd must estimate its tax payable for the year of assessment 2023 and furnish this estimate to the Director General by July 1, 2023 (within three months from the date of commencement of operations).

- For the year of assessment 2023, the estimate of tax payable provided by XYZ Sdn Bhd should meet the requirements specified in Section 107C(2) and Section 107C(3).

- In subsequent years (beginning with the year of assessment 2024), XYZ Sdn Bhd will follow the standard procedures for estimating tax payable as outlined in Section 107C, including adhering to the timing and minimum estimate rules.

This ensures that new companies have specific guidelines for estimating their tax liabilities when they commence operations during a year of assessment, and it also sets the groundwork for their tax estimation procedures in the following years.

5. **Monthly Instalments**: When an estimate is furnished, the tax amount is to be paid in equal monthly instalments based on the number of months in the basis period (subsection 107C(5)).

6. **Revised Estimates**: Companies can provide revised estimates during the sixth or ninth month of the basis period, and the payment is adjusted accordingly (subsection 107C(7)).

7. **Electronic Submission**: Estimates or revised estimates must be submitted electronically (subsection 107C(7A)).

8. **Director General’s Discretion**: The Director General may direct companies, limited liability partnerships, trust bodies, and co-operative societies to make payments by instalments and can also remit amounts under certain circumstances (subsection 107C(8) and subsection 107C(11)).

9. **Penalties**: Failure to pay instalments on time can result in penalties (subsection 107C(9)).

10. **Tax Recovery**: In cases where tax payable under an assessment exceeds the estimate by more than 30%, additional penalties may apply (subsection 107C(10)).

11. **Penalty**: This subsection outlines a penalty if they fail to estimate their tax payable, and no prosecution under Section 120 has been instituted against them for this failure. In such cases, the tax payable is increased by a sum equal to 10% of the tax payable, and this additional sum is recoverable as if it were tax due and payable under the Act. The provision encourages companies to comply with the tax estimation requirement and avoid penalties. (Section 107C(10A))

12. **Tax Collection**: Nothing within Section 107C shall prevent tax collection from a person to whom this section applies. The tax collection can proceed per Section 103, and the enforcement of the tax payment can be carried out under Section 106. (subsection 107C(11A)).

13. **Accounting Period**: In cases of failure to make up accounts, the tax increase or sum remains recoverable (subsection 107C(11B)).

14. **Definitions**: The section includes definitions of terms like “due date” and “revised estimate” (subsection 107C(12)).

Special consideration

Section 107C(4A) of the Malaysian Income Tax Act 1967 exempts certain companies from estimating their tax payable for the year of assessment and the immediately following year if they meet specific criteria related to paid-up capital.

Section 107C(4B) outlines conditions under which this exemption does not apply, particularly when ownership is linked to related companies.

Section 107C(4C) defines the term “related company” for the purpose of these provisions.

Section 107C(4A):

This subsection exempts certain companies from the requirement to estimate their tax payable under Section 107C.

Companies that first commence operations in a year of assessment and meet specific criteria related to paid-up capital are not required to estimate their tax payable for that year.

The exemption is applicable for the year of assessment and the immediate following year, or in the case of companies with no basis period, for the immediate two following years, provided their paid-up capital for ordinary shares is two million five hundred thousand ringgit or less.

Section 107C(4B):

This subsection specifies conditions under which the exemption in Section 107C(4A) does not apply.

It outlines scenarios where companies are not eligible for the exemption, such as when more than 50% of the paid-up capital in respect of ordinary shares is directly or indirectly owned by a related company.

Section 107C(4C):

This subsection defines the term “related company” as a company with paid-up capital in respect of ordinary shares of more than two million and five hundred thousand ringgit at the beginning of the basis period for a year of assessment.

These provisions provide exemptions and conditions related to estimating tax payable for companies that have recently commenced operations based on their paid-up capital and ownership structure.

Companies in Malaysia need to comply with these provisions to ensure accurate tax estimation and payment.

Compliance with these regulations helps avoid penalties and ensures that companies, limited liability partnerships, trust bodies, and co-operative societies meet their tax obligations as per the Malaysian Income Tax Act 1967.