On 14 May 2020, the IASB issued ‘Onerous Contracts — Cost of Fulfilling a Contract (Amendments to IAS 37)‘ amending the standard regarding costs a company should include as the cost of fulfilling a contract when assessing whether a contract is onerous.

As a result, the Malaysian Accounting Standards Board (“MASB”) issued the amendments to MFRS 137 Provision, Contingent Liabilities and Contingent Assets.

The amendments are effective for annual reporting periods beginning on or after 1 January 2022.

Entities, however, can early apply the amendments before their effective date.

《国际会计准则第37号 — 负债拨备、或有负债和或有资产》于2020年5月14日作出修订,阐明了企业在评估合同是否构成亏损合同时,需要将哪些类型的成本计入“履行合同的成本”。

因此,马来西亚会计准则委员会(”MASB”)发布了对马来西亚财务报告准则第137号(MFRS 137)- 负债拨备 [Provision]、或有负债 [Contingent Liabilities] 及或有资产 [Contingent Assets] 的修订。

企业应于 2022 年 1 月 1 日以后开始之年度报导期间适用该等修正内容,并得提前适用。

企业若提前适用该等修正内容,应揭露该事实。

What are Onerous Contracts?

First, what is an onerous contract?

MFRS 137 Provisions, Contingent Liabilities and Contingent Assets defines an onerous contract as:-

“a contract in which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it.

The unavoidable costs under a contract reflect the least net cost of exiting from the contract, which is the lower of the cost of fulfilling it and any compensation or penalties arising from failure to fulfil it.”

什么是“亏损性合同”

首先,什么是什么是“亏损性合约”?

马来西亚财务报告准则第137号(MFRS 137)「负债拨备、或有负债及或有资产」将亏损性合同(Onerous Contract)定义为:

"本准则所定义之亏损性合同是指一项合约,其义务履行所不可避免之成本,超过 预期从该合约获得之经济效益。

合同之不可避免成本是取消合同之最小净成本, 其为履行合同而发生之成本与怠于履行合同而发生之补偿或罚款之孰低者。”

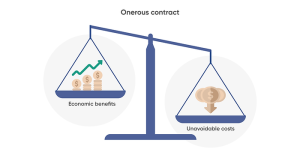

The graph on the left depicts the link between Economic Benefits and Unavoidable Costs.

左图描述了经济效益和不可避免的成本之间的联系。

Entities are required to measure and recognise a provision for an onerous contract according to paragraph 66 of MFRS 137 where the contract in question meets the criteria for being an onerous contract.

A provision is an obligation whose date and amount are unknown at this time.

The recognition of a provision is justified on the grounds that an entity is now obligated to pay the specified cost or provision amount in order to meet the requirements of a particular contract.

根据马来西亚财务报告准则第137号(MFRS 137)第66段,如果有关合同符合”亏损性合同”的标准,实体必须衡量和确认亏损性合同的准备。

负债拨备 [Provision] 是一种债务,其日期和金额目前还不清楚。

我们现在就需要确认拨备的理由是,一个实体现在有义务支付特定的成本或拨备金额,以满足特定合同的要求。

Example

The CCS Chocolate Company is in the business of manufacturing chocolate candy.

It has a noncancelable lease on a building in Kepong, that it uses for production.

The lease will end on December 31 of the second year, and to be classified as an operating lease for accounting purposes [Note 1].

The annual lease payment is RM120,000. In December Year 1, the company closes its Kepong facility and move its production plant to JB.

The company does not have high hopes that it will be possible to sublease the building that is situated in Kepong.

There is no predicted future economic benefit from the lease, hence the contract is onerous. The unavoidable cost of fulfilling the lease contract for Year 2- of RM120,000 should be expensed and recorded as a provision on December 31,

The amendments to MFRS 137 are specifically to address the determination of the cost of fulfilling a contract.

The determination of the cost of fulfilling a contract is important in order to assess whether the contract is onerous.

As a result, Paragraphs 68A, 94A and 105 are added and paragraph 69 is amended.

Para 68A

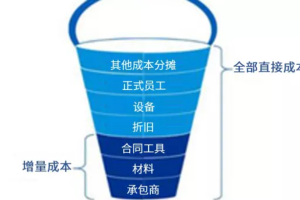

The cost of fulfilling a contract comprises the costs that relate directly to the contract. Costs that relate directly to a contract consist of both:

- the incremental costs of fulfilling that contract—for example, direct labour and materials; and

- an allocation of other costs that relate directly to fulfilling contracts—for example, an allocation of the depreciation charge for an item of property, plant and equipment used in fulfilling that contract among others.

履行合同之成本包含与该合同直接相关之成本。与合同直接相关之成本由下列两者所组成:

- 履行该合同之増额成本 ─ 例如:直接人工及原料;及

- 与履行合同直接相关之其他成本之分摊 ─ 例如:履行该合同所使用之不动产、厂房及设备项目之折旧费用之分摊等。

Para 69

Before a separate provision for an onerous contract is established, an entity recognises any impairment loss that has occurred on assets used in fulfilling the contract (see MFRS 136).

企业在为亏损性合同建立一单独负债播备之前,应对履行该合同所使用之资产已发生之任何减损损失先予认列(见马来西亚财务报告准则第 136 号)。

Para 94A – Transitional Provisions

Onerous Contracts — Cost of Fulfilling a Contract [Onerous Contracts—Cost of Fulfilling a Contract issued by IASB in May 2020] added paragraph 68A and amended paragraph 69.

An entity shall apply those amendments to contracts for which it has not yet fulfilled all its obligations at the beginning of the annual reporting period in which it first applies the amendments (the date of initial application).

The entity shall not restate comparative information. Instead, the entity shall recognise the cumulative effect of initially applying the amendments as an adjustment to the opening balance of retained earnings or other component of equity, as appropriate, at the date of initial application.

2020 年 6 月发布之「亏损性合同 ─ 履行合同之成本」新增第 68A 段,并修正第 69段。

企业应将该等修正内容适用于其第一次适用该等修正之年度报导期间开始日(初次适用日)时其尚未履行完所有义务之合同。

企业不需要重编对比资讯,反之企业应认列初次适用该等修正内容之累积影响数,以作为初次适用日之保留盈余或权益之其他组成部分(如适当时)期初余额之调整。

According to the definition, one of the considerations that go into evaluating onerous contracts is whether or not there are any unavoidable costs.

Therefore, assessing unavoidable costs itself demands extensive judgement by entities.

But what are “unavoidable costs”?

根据该定义,评估亏损性合同的考虑因素之一是 – 是否有任何不可避免的成本?

因此,评估“不可避免的成本”本身就要求各实体作出广泛的判断。

但究竟什么是 “不可避免的成本”?

What are Unavoidable Costs?

In the old version of MFRS 137, it is explained that the unavoidable costs associated with a contract reflect the lowest possible net cost of withdrawing from the contract.

The cost of withdrawing from a contract could be one of the following options:

- the penalty or compensation that an entity has to pay to the contracting party upon failing to fulfil its obligation;

- total costs to be incurred in fulfilling the obligation under the contract.

Accordingly, the lower of the two amounts (a and b) is the unavoidable costs.

Most contracts will outline the expected penalties or compensation that an entity must pay if it fails to meet its obligations. As a result, entities can quickly determine the amount of (a).

However, the difficulty encountered is in estimating the cost of fulfilling such an obligation (i.e. b). In general, entities consider two types of costs when assessing the cost of fulfilment:

- Incremental costs that entities anticipate incurring to fulfil the contract. Instances include direct labour and materials.

- Other costs include allocation of other general costs directly related to contract fulfilment, such as the depreciation of property, plant, and equipment used for the contract.

Why Amendments to IAS 37 & MFRS 137 are Needed

Previously, only incremental costs are considered by some entities when calculating the cost of fulfilling an obligation.

Other entities, on the other hand, determine the cost of fulfilment using the total cost method.

Under the total costs approach, entities take incremental expenses and other costs into consideration.

Consequently, there exist disparities in company practices.

The amendments to IAS 37 & MFRS 137 are intended to enhance the consistent application and execution of accounting standards.

The amendments provide that an entity must NOW account for both incremental and other costs [i.e. total costs] when calculating the cost of contract fulfilment.

What is the Logic Behind the Total Costs Approach?

- The inclusion of all costs provides users of financial statements with more useful information.

- It is likely that the benefits of giving such information outweigh the costs of obtaining such information.

- The inclusion of all contract-related costs, regardless of whether they are incremental costs or other costs, is consistent with other requirements in MFRS 137 and other accounting standards.

- 纳入所有成本为财务报表的使用者提供了更有用的信息。

- 提供这种信息的好处很可能超过获得这种信息的成本。

- 列入所有与合同有关的成本,无论它们是增量成本还是其他成本,都与 MFRS 137 和其他会计准则的其他要求一致。

What Costs constitute the Cost of Performing a Contract? | 哪些成本构成履行合同的成本?

The amendment clarifies that the “cost of performing a contract” also includes.

- Incremental costs – for example, direct labour and materials; and

- the apportionment of other direct costs – for example, the apportionment of depreciation on property, plant and equipment used in the performance of the contract.

Picture: KPMG

该修订阐明了“履行合同的成本”同时包括:

- 增量成本——例如,直接人工和材料;以及

- 其他直接成本的分摊金额——例如,履行合同时所用的不动产、厂场和设备项目的折旧费用的分摊。

The Impact on Entities

The amendments have had an impact on entities that use the incremental cost approach as their accounting policy previously.

With the adoption of the total cost approach, we expect more contracts to be onerous as a result of this amendment, as more costs will be included in determining the cost of performing the contract.

这些修正案对之前使用增量成本法作为其会计政策的实体产生了影响。

由于总成本法的采用,我们预计更多的合同会因为此修订而变成“亏损性合同”,这是因为更多的成本将被包括在确定履行合同的成本中。

[Note 1]: The accounting treatment of leases has undergone substantial change as a result of the implementation of IFRS 16, Leases. The most notable of these changes is that lessees are now required to recognise operating leases as a right-of-use (ROU) asset as well as lease liability.

When it comes to onerous contracts, these are governed by IAS 37, Provisions, Contingent Liabilities and Contingent Assets. This IFRS standard is applied to any contract for which the unavoidable costs of meeting the contract obligations exceed the economic benefits that are expected to be received under that contract. However, it is an intriguing question to explore whether or not IAS 37 and IFRS 16 can co-exist.

The International Accounting Standards Board came to the conclusion that it was unnecessary to stipulate any precise requirements for onerous contracts within IFRS 16.