Filing Programme for Year 2022 – Resident Individuals (Knowledge Workers, Expert Workers, Non-Citizen Workers Holding Key Positions) & Non-Resident Individuals – PDF

Program Memfail BN 2022

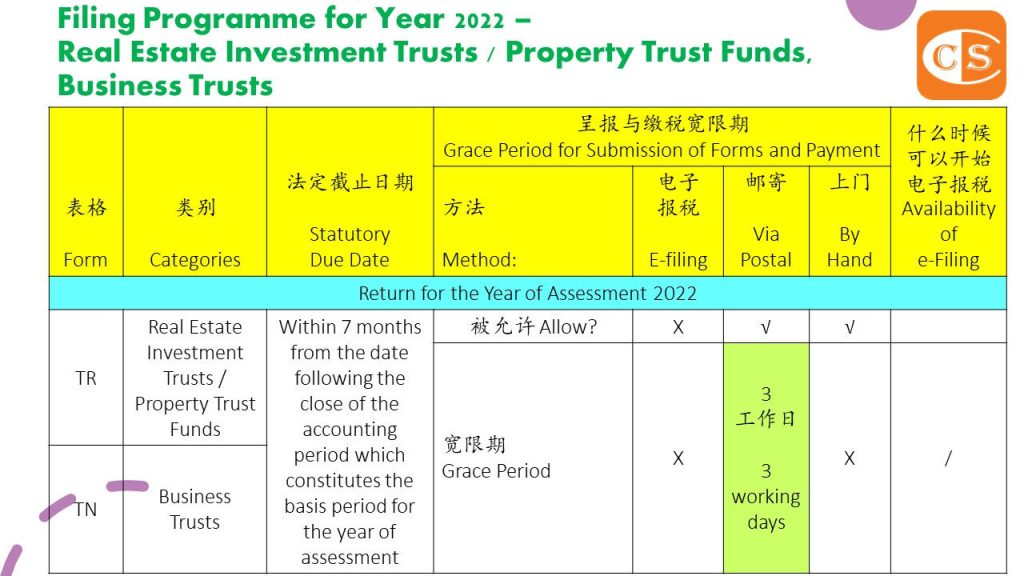

1. The IRB has released the Filing Program for the year 2022. According to the filing programme, the statutory filing and tax payment due dates, as well as the grace period and manner of submission for the various return forms, are all specified.

2. It is available on the IRB’s website at www.hasil.gov.my (Forms > Filing Programme for the Year 2022).

3. The statutory income tax filing deadlines for Resident Individuals (Knowledge Workers / Expert Workers / Non-Citizen Workers Holding Key Positions) and Non-resident Individuals (Including Knowledge Workers) are:-

👉 30 April if Do NOT Carry On Business

👉 30 June if Carry On Business

4. The Inland Revenue Board also has good news for taxpayers with regard to the grace period:-

👉 3 more working days if filing by post

👉 15 more working days if filing online

5. To download

✍️ https://www.ccs-co.com/post/what-snew21-2022

🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻

1. 内陆税收局已经发布了2022年的申报安排。 根据该申报安排,法定申报 [Statutory Filing] 和缴税日期 [Tax Payment Due Dates],以及各种申报表格的宽限期 [Grace Period] 和提交方式 [Manner of Submission]都有明确规定。

2. 此项发布可以在内陆税收局 (IRB) 的网站上找到:www.hasil.gov.my (Forms > Filing Programme for Year 2022)。

3. 对于对于知识工作者/专业工作者/担任重要职务的非公民的马来西亚税务居民 [Tax Resident] 以及非马来西亚个人税务居民 [Non-resident Individuals] 的法定所得税申报截止日期为:

👉 4月30日,如果没有商业收入

👉 6月30日,如果有商业收入

4. 内陆税收局也为纳税人捎来好消息,宽限期方面:

.👉 如果是通过邮寄的话,多3个工作日

👉 如果是通过网上提交,则多15个工作日

5. 下载 ✍️ https://www.ccs-co.com/post/what-snew21-2022

🌼🌼🌼🌼🌼🌼🌼🌼🌼🌼

Latest Updates #近期更新

1. The Publication of MIA’s Practice Review Annual Report 2020/2021

[MIA 2020/2021年 的实践审查年度报告]

2. Special Income Remittance Programme to Malaysian Residents

[源自外国汇入马来西亚的收入 特别报税方案]

3. Post-implementation Review of IFRS 9 — Classification and Measurement

[国际财务报导准则第9号之 施行后检讨 —分类及衡量]

4. Adoption of ISQM 1, ISQM 2 and ISA 220 (Revised)

[ISQM 1、ISQM 2 和 ISA 220 (修订版)的采纳]

5. Movable Property Security Interest (MPSI) Bill

[动产担保权益法案]

6. IFRS Foundation announcement on the International Sustainability Standards Board (ISSB)

[国际财务报告准则基金会关于国际可持续发展 准则委员会的公告]

7. MASB Updates No.1 November 2021 – IFRS Interpretations Committee (IFRIC) Agenda Decisions

[马来西亚会计准则委员会 [MASB] 2021年11月第1号更新 – 国际财务报告准则解释委员会(IFRIC)议程决定]

8. MASB Updates No.1 November 2021 – IASB Project on Equity Method

[MASB 2021年11月第1号更新 – 会计准则理事会关于权益法 [Equity Method] 的项目]

9. Bursa Malaysia issues updated Corporate Governance Guide

[马来西亚证券交易发布更新的 公司治理指南]

10. Amendments to the By-Laws (on professional ethics, conduct and practice) of MIA

[对 MIA 章程 (关于职业道德、行为和实践)的修订]

11. Labuan Business Activity Tax (Requirements for Labuan Business Activity) Regulations 2021

[2021年纳闽商业活动税 (纳闽商业活动的要求)条例]

12. Pembangunan Sumber Manusia Berhad (Exemption of Levy) (No. 2) (Amendment) Order 2021 [2021 年人力资源发展有限公司 (免征征税)(第 2 号) (修订) 指令]

13. Income Tax (Exemption) (No. 11) Order 2021

[2021年所得税 (豁免)(第11号) 指令]

14. Income Tax (Exchange of Information) Rules 2021 – Request for Information

[2021年所得税 (信息交流) 细则 – 要求提供信息]

15. Stamp Duty (Exemption) (No. 11) 2021 (Amendment) Order 2021

[2021 年印花税(豁免) (第 11 号)(修订) 指令]

16. Income Tax (Exemption) (No. 13) 2013 (Amendment) Order 2021

[2021年所得税 (豁免)(第 13 号) 2013年(修订) 指令]

17. Income Tax Double Deduction for the Sponsorship of Scholarship to Malaysian Student

[赞助马来西亚学生奖学金的 所得税双重扣税]

18. Double Deduction for Expenditure on Provision of Employees’ Accommodation

[雇员住宿费用双重扣税]

19. Starting from the YA 2022, Company Secretarial and Tax Filing Fees can claim Deduction even not PAID

[2022课税年度开始,公司秘书费及报税费用,没还钱也可以扣税了]

20. “MIA SMPs Channel” – a Dedicated Telegram Channel for SMPs

[中小会计事务所 (SMPs) 专用 Telegram 频道]

21. EPF: extension of 9% statutory contribution rate for Employees

[EPF: 延长雇员9% 的法定缴款率]

22. Income Tax (Industrial Building Allowance) (Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (工业建筑津贴)(敦拉萨国际贸易中心 Marquee 地位公司)(修订) 细则]

23. Income Tax (Accelerated Capital Allowance)(Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (资本津贴加速)(敦拉萨国际贸易中心Marquee 地位公司)(修订) 细则]

24. Income Tax (Deduction for Relocation Costs for Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (敦拉萨国际贸易中心 Marquee 地位公司 搬迁费用的扣除)(修订) 细则]

25. Income Tax (Deduction for Rental Payments) (Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (租金扣除) (敦拉萨国际贸易中心 Marquee 地位公司)(修订) 细则]

26. Income Tax (Exemption) (No. 4) 2013 (Amendment) Order 2021

[2013年所得税 (豁免)(第4号) (修订) 指令]

27. Income Tax (Exemption) (No. 12) Order 2021

[2021年所得税 (豁免)(第12号) (修订) 指令]

28. Special Deduction for Reduction of Rental to SMEs extended to 30.6.2022

[中小型企业租金特别扣税延长至2022年6月]

29. Special Deduction for Reduction of Rental to Non-SMEs Tenants extended to 30.6.2022

[非中小型企业租户租金特别扣税 延长至2022年6月]

30. Costs of Renovation and Refurbishment of Business Premise is allowable up to 31.12.2022

[营业场所翻修和翻新费用 扣税至2022年12月31日]

31. Tax Residents to be exempted from tax on the foreign-sourced income until Dec 31, 2026

[税务居民源自国外的收入将被免征税至2026年12月31日]

32. Export of Private Health Care Services – Tax Exemption

[出口私人保健服务 – 税务豁免]

33. Instruments in relation to an approved M & A – Stamp Duty Exemption

[与批准的合并或收购有关的文件 – 豁免征收印花税]

34. Double Tax Deduction for the Sponsorship of Scholarship to Malaysian Student

[赞助马来西亚学生奖学金,所得税双重扣税]

35. RM 20,000 Tax Rebate for the newly set up Company – ⚠️⚠️ Conditions apply ⚠️⚠️

[开新公司的2万令吉税务回扣是有条件的]

36. Finance Act 2021 has been Gazetted

[2021年财政法令已经在宪报颁布了]

37. IASB Exposure Draft ED/2021/9 Non-current Liabilities with Covenants (Proposed amendments to IAS 1)

[具合约条款之非流动负债 (国际会计准则第1号)]

38. 38. IASB Exposure Draft ED/2021/10 Supplier Finance Arrangements (Proposed amendments to IAS 7 and IFRS 7)

[国际会计准则理事会征求意见稿ED/2021/10 供应商融资安排 (对国际会计准则7和国际财务报告准则7的拟议修正)]

39. SST – Guide on Food & Beverages

[服务税 – 食品和饮料指南]

40. SST – Guide on Parking Services

[服务税 – 停车场服务指南]

41. SST – Guide on Motor Vehicle Services or Repair

[服务税 – 机动车服务或维修指南]

42. Double Tax Deduction for Expenditure in relation to Vendor Development Programme

[与供应商发展计划有关的支出双重扣税]

43. Tax Deduction for Investment in a Project of Commercialisation of Research and Development Findings

[研究与开发成果商业化项目投资 享有扣税资格]

44. FAQs on the implementation of Tax Identification Number, TIN

[这绝不是天上人间 而是TIN罗地网]

45. TP 1 表格,什么来的

[Something About “Form TP 1”]

46. Statutory Minimum Wages – Why Pay Raise is Important?

[法定最低工资 – 为什么加薪很重要]

47. Accelerated Capital Allowance For Excursion Bus

[购买游览巴士享有加速资本津贴]

48. Deferment of the implementation of 2% Withholding Tax on Payment [Commission] Made To Agent etc.

[ 推迟执行向代理商、经销商、分销商支付佣金的2%预扣税]

49. HRD Levy Payment for the newly registered employers for January 2022 has been Resumed

[新注册的雇主,2022年1月恢复支付人力资源开发基金]

50. Mandatory Adoption of Prescribed Forms CP21, CP22, CP22A, and CP22B

[强制性采用指定的表格 CP21、CP22、CP22A 和 CP22B]

51. 只有在扣押令下 IRB 才有权要求银行提供你的信息

[Power to call for bank information for purpose of making a Garnishee Order application by IRB]

52. Tax Concessions Due to COVID-19 Travel Restrictions expired on 31 December 2021

[新冠肺炎期间的行动限制所给予的税务宽免于2021年12月31日结束]

53. Initial Application of MFRS 17 and MFRS 9 – Comparative Information (Amendment to MFRS 17 Insurance Contracts)

[初次应用 MFRS 17 和 MFRS 9 – 比较信息 (MFRS 17 保险合同的修正)]

54. Filing Programme for Year 2022 – Employers

[2022年的申报安排 – 雇主 ]

55. Filing Programme for Year 2022 – Associations, Deceased Persons’ Estate and Hindu Joint Families

[2022年的申报安排 – 社团、死者遗产和印度教联合家庭]

56. Filing Programme for Year 2022 – Other Individuals

[2022年的申报安排 – 其他人士]

57. Filing Programme for Year 2022 – Individuals, Partnerships

[2022年的申报安排 – 个人、合伙企业]

https://ccsyourauditor.blogspot.com/2022/01/issue-no-192022-filing-programme-for.html

58. Filing Programme for Year 2022 – Trust Bodies and Co-Operative Societies

[2022年的申报安排 – 信托机构和合作社]

https://ccsyourauditor.blogspot.com/2022/01/issue-no-232022-filing-programme-for.html

🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳

👉 专业资讯送到你手中

1. 网站 ✍️ https://www.ccs-co.com/

2. Telegram ✍️ http://bit.ly/YourAuditor

3. Instagram ✍ http://tiny.cc/rojzrz

4. 部落格 ✍ https://lnkd.in/e-Pu8_G

5. Google ✍ http://tiny.cc/9oussz