Introduction

The purpose of this checklist, among other things, is for each member to perform a self-assessment exercise on the quality control policies and procedures at the firm level.

Part I of the checklist is organised around the elements detailed in the ISQC1 [*}.

Part II will deal with issues that the Institute would expect the member to comply with during the execution of any assurance engagement under ISA 700.

This form can also be downloaded from the Institute’s website at www.mia.org.my.

However, ISQM 1 replaces ISQC 1, Quality Control for Firms that Perform Audits and Reviews of Financial Statements and Other Assurance and Related Services Engagements. Firms are required to have systems of quality management designed and implemented in accordance with ISQM 1 by December 15, 2022

Part I: ISQC 1 Compliance

Element 1: Leadership Responsibilities For Quality Within the Firm

- Is a person designated to assume responsibility for the firm’s quality control system?

- Does your firm have an up-to-date Quality Control Manual appropriate to your practice’s size and operating characteristics?

- Does your practice allocate sufficient resources for developing, documentation and supporting its quality control policies?

- Does your firm have a mechanism to ensure that operational responsibility for the quality control system has been appropriately assigned by the firm’s chief executive officer or managing board of partners?

Element 2: Ethical Requirements

- Do your practice document policies and procedures designed to assure the firm that the practice and its personnel comply with the fundamental principles of professional ethics, which include integrity, objectivity, professional competence and due care, etc.?

- Do you take into consideration (including documentation) whether members of the engagement team have complied with major ethical requirements?

- Are there procedures to identify threats to professional independence under the Institute’s code of ethics?

- Does your practice monitor compliance with policies and procedures relating to independence?

- For all audits of financial statements of listed entities, is there a rotation of the engagement partner and the engagement quality control reviewer after a specified period?

Element 3: Acceptance & Continuance Of Client Relationship & Specific Engagements

- Does your practice put in place a mechanism to consider the integrity of the client accepted?

- Does your practice put in place a mechanism that can determine that it is competent to perform the engagement and has the capabilities, time and resources to do so?

- Does your practice obtain adequate and relevant information as necessary in the following circumstances :

- before accepting a new engagement?

- when deciding whether to continue an existing engagement?

- when considering acceptance of a new engagement with an existing client?

- Where issues have been identified and the practice decides to accept or continue the client relationship or a specific engagement, is there any mechanism to ensure adequate documentation to record how the issues were subsequently resolved?

Element 4: Human Resources

- Does the firm establish policies and procedures designed to provide it with reasonable assurance that:

- it has sufficient personnel with the capabilities, competence and commitment to ethical principles necessary to perform its engagement under professional standards and regulatory and legal requirements; and

- to enable the firm or engagement partners to issue reports that are appropriate in the circumstances

- Does your practice monitor the professional development of its professional staff at regular intervals?

- Is there a standard procedure where the identity and role of the engagement partner are communicated to key members of the client management and those charged with governance upon the commencement of the engagement?

- Do you think you have the appropriate capabilities, competence, authority and time to perform your role as an engagement partner for ALL engagements?

- Are appropriate staff with the necessary capabilities, competence and time being assigned to perform engagements to enable the firm or engagement partners to issue appropriate reports in the circumstances? (Consider the knowledge of the relevant industries, ability to apply professional judgment etc.)

Element 5: Engagement Performance

- Are our policies and procedures being put in place to ensure appropriate documentation of the work performed and the timing and extent of the review?

- Have appropriate policies and procedures been put in place to ensure significant judgment made during the audit has since been documented?

- Are review responsibilities determined on the basis that more experienced engagement team members review work performed by less experienced team members?

- Are there mechanisms to ensure that conclusions from internal or external consultations are documented and implemented?

- Are there any mechanisms in your firm that deal with and resolve differences of opinion within the engagement team?

- Does your firm ensure that engagement quality control reviews (EQCR) are performed on auditing listed entities’ financial statements and other engagements the firm may deem appropriate before the firm issues reports?

- Does your practice establish policies and procedures setting out:-

- the nature, timing and extent of an EQCR;

- criteria for the eligibility of EQCR; and

- documentation requirement for EQCR.

- Do your practice’s policies and procedures address the appointment of engagement quality control reviewers and establish their eligibility through

- the technical qualifications required to perform the role, including the necessary experience and authority; and

- the degree to which an engagement quality control reviewer can be consulted on the engagement without compromising the reviewer’s objectivity?

- Period of service before rotation for specific audit engagements regarding financial statements of listed entities?

Element 6: Monitoring

- Does your practice put in place any policies and procedures designed to provide it with reasonable assurance that the quality control system is relevant, adequate, operating effectively and complied with in practice?

- Does the firm inspect a selection of completed engagements on a cyclical basis which ordinarily spans no more than three years?

- Does the practice at least annually communicate the quality control system monitoring results to engagement partners and other appropriate individuals within the firm, including the chief executive officer or the managing board of partners?

- Does your firm have a mechanism that deals with complaints and allegations that work performed by your firm fail to comply with professional standards and regulatory and legal requirements?

- Does your firm have established policies and procedures requiring appropriate documentation to provide evidence of the operation of each element of its system of quality control?

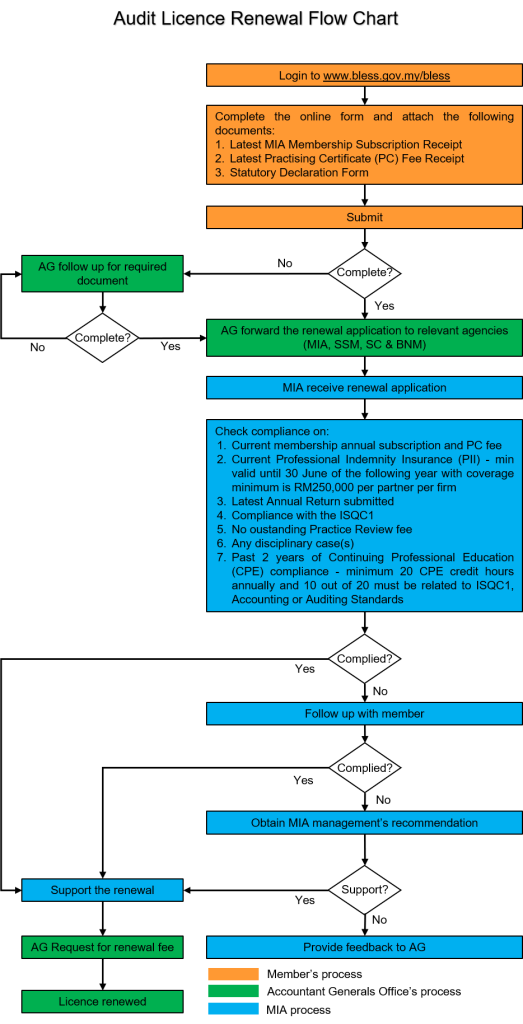

MIA – Audit Licence Renewal Flowchart

PART II: PERFORMANCE OF AUDIT ENGAGEMENT

- Does your practice utilise audit programmes, pre-printed forms, questionnaires and/or checklists to ensure proper documentation of audit or review procedures and basis to support pertinent issues?

- Does your practice have an established system for second-person reviews?

- Does your practice have a systematic method of file organisation?

- Does your practice issue engagement letters and consider whether engagement letters should be reissued?

- Does your practice mechanism in place to ensure compliance with the regulations and auditing guidelines for specialised industries? (Consider BAFIA, Capital Market Services Act 2007, property developers licensing requirements etc.)

- Does your practice have any mechanism to ensure sufficient knowledge of the client’s business and system has been obtained, and this significantly affects the engagement?

- Does your practice evaluate the review of the internal control system of its clients, where appropriate?

- Does your practice employ documentation to assist in determining that the results of the evaluation and testing of the internal control systems are taken into account in determining the nature, extent and timing of substantive procedures?

- Does your practice have a mechanism to ensure sufficient and appropriate substantive tests (including analytical review) are performed even in situations where internal controls are relied upon?

- Does your practice use checklists or documentation to arrive at valid conclusions to form an opinion?

- Does your practice have a mechanism to ensure that the requirements for an audit report are duly complied with?

- Where qualified audit reports are deemed necessary, does your practice have an established second-person review system?

*Quick note to Audit Firms:

Firms are recommended to research the requirements of the three new quality management standards that have been adopted by the International Auditing and Assurance Standards Board (IAASB). These standards are scheduled to become effective on December 15, 2022.

The standards, which include the International Standards on Quality Management ISQM 1 and ISQM 2, as well as the International Standard on Auditing ISA 220 Revised, are an evolution from a traditional, more linear approach to quality control.

They are intended to create a more robust System of Quality Management for Firms that use the standards developed by the International Auditing and Assurance Standards Board (IAASB). The new standards provide an approach to audit quality management that is robust, scalable, and proactive. This approach is essential to ensuring that the auditing profession will continue to be trusted and viable in the future.