The Inland Revenue Board of Malaysia (HASiL) has issued responses to CTIM’s feedback/comments on Transfer Pricing related issues as follows:-

- HASiL Responses to CTIM’s Feedback/Comments on Form C, Year of Assessment 2022 – Transfer Pricing related disclosures dated 17 October 2022.

- HASiL Responses to CTIM’s Feedback/Comments on Minimum Transfer Pricing Documentation Template (Pin 1/2022) As Published By The Inland Revenue Board Of Malaysia (IRBM) On 10 November 2022 dated 19 November 2022.

IRBM’s Responses to CTIM’s Feedback/Comments on Form C, Year of Assessment 2022 – Transfer Pricing related disclosures dated 17 October 2022

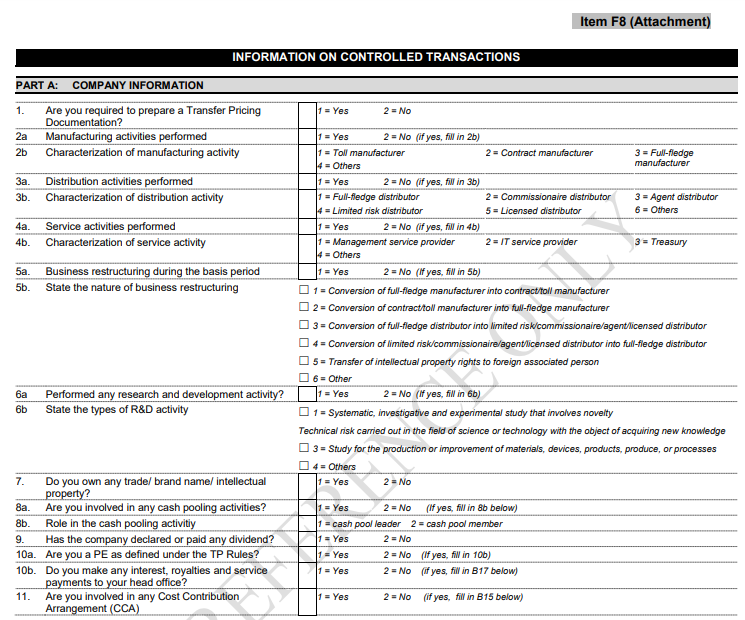

F8 – Part A- Items 2, 3 and 4 of Form C

The characterisation of a company can only be arrived at after the company performs detailed functions, assets employed and risks (“FAR”) analysis.

The FAR analysis is usually prepared by the company in conjunction with the requirement to prepare a comprehensive TPD.

The part discusses comments from CTIM (Chartered Tax Institute of Malaysia) on Form C, YA 2022, related to Transfer Pricing disclosures.

The part covers three issues that CTIM has raised and the corresponding responses from IRBM (Inland Revenue Board of Malaysia).

Issue No 1

CTIM:

Companies below the threshold can opt to prepare a simplified TPD that does not include a detailed FAR analysis.

For this category of companies (i.e. companies below the threshold), how would the IRB expect the characterisation to be supported?

IRBM:

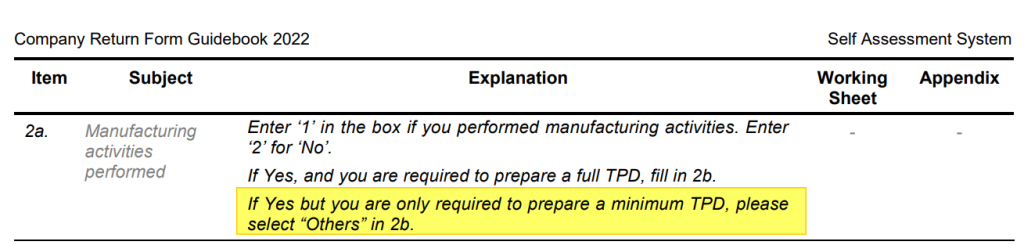

Taxpayers who are required to prepare full TPD should answer Part A – items 2(b), 3(b) and 4(b).

Taxpayers who only prepare minimum TPD are NOT required to answer Part A – items 2(b), 3(b) and 4(b).

CTIM further comments: A taxpayer who prepares minimum TPD is required to answer 2(a), 3(a) and 4(a).

Unless these are marked as “No”, it is mandatory to complete (b).

The system does not allow (b) to be left blank unless the response to (a) is “No”.

IRBM Comment (on 29.12.2022):

New updates will be made for Q 2(a), 3(a) and 4(a) for the taxpayer who answered ‘Yes” and prepared minimum TPD.

Further clarification will be provided in the explanatory notes in Form C 2022 Guidebook.

The latest amendments have already been uploaded to IRBM’s website:-

Issue No 2

CTIM asked whether a company should tick “NO” for the questions in Part A – items 2(a), 3(a), and 4(a) if their business activity does not fall under any of the three types of characterisation.

IRBM:

Confirmed that the company should tick “NO” for the questions in Part A – items 2(a), 3(a) and 4(a).

Issue No 3

Apart from the specified categories of manufacturing, distribution and services, other industry types are not covered therein.

CTIM Comment:

Please advise under which category the taxpayer should declare the following types of business activities:

i. Property development

ii. Construction

iii. Logistics

iv. Oil Palm Plantation

v. Other activities not elsewhere specified

IRBM Comment:

If a company is involved in the above or other industries/business activities and does not perform manufacturing, distributing and service activities, the taxpayer may answer ‘NO’ in Part A – items 2(a),3(a) and 4(a).

CTIM further comments:

Construction and Logistics can be viewed as ‘Services’.

To have the least exceptions when filling Borang C (i.e., fit most business activities within the categories of Manufacturing, Distribution or Services, it may be better to place (ii) and (iii) under 4(a) “Yes” and 4(b) “Others”.

IRB can consider adding a field for remarks if “Others” is selected – this is to clarify the exact nature of the business. To obtain accurate information for risk-based case selection, relevant and adequate disclosure must be made.

IRBM Comment(on 29.12.2022)

The industries where the taxpayer belongs should be reflected in the Business Code under Item A1 – Part I.

Taxpayers under the listed industries above may select “Others” if does not involve in any manufacturing, distribution or service activities.

IRBM’s Responses to CTIM’s Feedback/Comments on Minimum Transfer Pricing Documentation Template (Pin 1/2022) As Published By The Inland Revenue Board Of Malaysia (IRBM) On 10 November 2022, dated 19 November 2022 as below:

Feedback/comments on:

- General

- Company information

- Group information

- Controlled transactions

- Pricing policy(For Each Type of Controlled Transaction)

1. General The IRBM has provided a PDF template entitled “Minimum Transfer Pricing Documentation (MTPD)” that applies to a person who falls outside the scope of paragraph 3.1 of the Malaysian TP Guidelines.

CTIM Comments: a) We would like the IRBM to confirm that taxpayers who meet the requirements for preparing an MTPD according to the TP Guidelines can use the template to submit in TPD in the future and that this is a form of documentation that the IRBM will accept.

Also, please confirm that if the taxpayer fills out this template, he or she doesn’t need to fill out any other report (limited/simplified/minimal report) to meet the TPD requirement for the same year. IRBM Comments:

Yes. b) Kindly clarify if the MTPD template is just a guide and if taxpayers can choose to prepare a minimal TP report if it has all the categories and information listed in the IRBM template.

We suggest that the templates serve as a general guide or checklist for what IRBM expects in an MTPD since the current template doesn’t work for taxpayers with multiple business sources. IRBM Comments:

Yes, the template serves as a guide only. Taxpayers may provide additional information where needed. c) If the taxpayer does not include all the required information in the MTPD template, does this mean they are no longer contemporaneous? What would be the implication? IRBM Comments:

Yes, the requirement for contemporaneous documentation has been stated in the rules.

Guidance for preparing minimum TPD has also been explained in MTPGL 2012.

Failure to prepare will be penalised under Section 113B ITA 1967. d) In view of the above and if the template is tantamount to TP documentation, will the documentation be regarded as an acceptable TPD if the taxpayer has not performed/does not include a benchmarking analysis?

How does the IRBM expect the taxpayer to justify the arm’s length nature of the RPTs in the absence of a benchmarking analysis? IRBM Comments:

Considering the costs and resources involved in preparing the benchmarking analysis, we are willing to consider other analysis methods to ensure that the arm’s length principle is being met.

Based on TP Rules 2012, other methods which provide the highest degree of comparability between the transactions are also acceptable.

e) We note that the taxpayer must indicate the entity’s characterisation in filling out the template (however, the template does not encapsulate a functional analysis).

Extending from this, is the taxpayer required to perform a functional analysis to justify the characterisation of the entity?

IRBM Comments:

Amendments will be made where taxpayer only needs to disclose their principal activity.

f) What is the effective date for the use of this template?

IRBM Comments:

This template is a guide to provide assistance to taxpayers in preparing minimum TPD. There is no effective date nor legal impact in using this template.

g) Reference Box on top of page 1 – Based on the updated version of the Malaysian Transfer Pricing Guidelines 2012 (MTPGL), the reference should be Paragraph 1.3.1 instead of 3.1. In addition, it is proposed that Paragraph 1.3.2 be included for the taxpayer’s additional reference. It is proposed that the wordings in the reference box be revised to:

“This template is only for the person who falls outside the scope of paragraph 1.3.1 of the Malaysian Transfer Pricing Guidelines. The TP documentation requirement for a person under this category is described in paragraph 1.3.2 of the guidelines”

IRBM Comments:

The amendment has been made and uploaded on the website.

2. Company information

CTIM Comments:

Characterisation of business activity [Item A6] a) Characterisation is determined based on performing functions, assets and risks (FAR) analysis of the taxpayers in relation to the intercompany transactions. As the template issued by the IRBM for maintaining the MTPD does not require the taxpayer to prepare a full FAR analysis, we propose to re-word/ rename the “Characterisation” to ‘Principal activity of the business. IRBM Comments: Please refer to our answer in Q1 (e). b) We note that per the MTPD template, the disclosure required in relation to functional characterisation differs from the disclosure required in Form C, which also requires taxpayers to characterise their business activities (under Part A – item 2b, 3b and 4b fields, as relevant). In line with the recent IRBM clarification/feedback provided to CTIM in relation to TP Related Disclosure in Form C for Year of Assessment 2022 (dated 6 October 2022), taxpayers who only prepare the MTPD are not required to answer Part A – item 2b, 3b and 4b fields in Form C. As such, the characterisation of business activity should be consistent with the IRBM’s clarification.

c) If the taxpayer is engaged in both manufacturing and distribution, is the taxpayer required to characterise both business segments? This is on the assumption that the taxpayer has two separate business segments. Or is the taxpayer only required to characterise the main revenue contributor?

As mentioned above, for taxpayers who qualify for MTPD, CTIM would like to propose that characterisation is unnecessary in line with the IRBM’s clarification on 6 October 2022.

IRBM Comments: The issues under Q2 (b) and (c) has been resolved with the changes made to item A6.

Industry code

d) For the above information on Industry – please confirm if this follows the MSIC Code / Business code per Form C?

For taxpayers with more than one business source, please confirm that the industry code follows that of Form C.

IRBM Comments:

Yes, it follows the Business code as per Form C. Taxpayers can provide more than one business code.

3. Group Information

Item B3 – 7 – The taxpayer may be a part of a large Malaysian or Multinational Group with several subsidiary or affiliate companies. However, the taxpayer may only have related party transactions with one or a few of the other related entities.

It is unclear whether the taxpayer must fill in the details of every related entity in Part B.

This also refers to the global organisational chart, whereby the taxpayer must include all direct and indirect subsidiaries, associated companies and other related companies in the group.

CTIM Comments General comment on group information a) Items B1 – B7 require additional disclosures beyond what is normally included by taxpayers in their MTPD. Also, the details required are not consistent with the Paragraph 11.2.4 (a), (c) and (d) of MTPGL. IRBM Comments:

Para 11.2.4(a) in the MTPGL requires taxpayers to submit the organisational structure, including a global organisation chart. Other information under this part should be extracted from Form C. b) The template’s purpose should be to simplify compliance (especially for SMEs). There should be a balance between the extent of information expected from companies within and outside the scope of Paragraph 1.3.1 of MTPGL.

The following information mandated in the template would create an additional administrative burden and require disproportionate effort relative to the benefit of providing the information: i. Address and TIN of shareholders and subsidiaries/affiliates; Taxpayers should be able to provide TIN numbers for companies in Malaysia. They may also provide TIN numbers for those outside Malaysia, if available. ii. Entire global organisation structure; and iii. Reporting lines between the management of the company’s business and its associated persons, including the description of the individuals to whom the business reports and the countries in which such individuals maintain their principal offices. IRBM Comments:

Information for b) ii. and b) iii. is disclosed in the Masterfile.

A taxpayer may submit the Masterfile if the document is made available by the Ultimate Holding Company/ CbCR Reporting Entity. c) For items B3 to B6, we suggest documenting the legal entity name and country of tax residence of only subsidiaries and affiliates with whom the taxpayer had related party transactions during the financial period. IRBM Comments:

This information can be extracted from the global organisation chart if the group provides the information. d) The same suggestion also applies to the Global Organisation Chart. For MNEs, there may be several legal entities within the Group. Covering every legal entity in the chart would be an administrative burden for the taxpayer. Instead, the Global Organisation Chart should be limited to the related companies with whom the taxpayer had related party transactions during the financial period. This is consistent with the requirement of paragraph 11.2.4(a), which states that : “… the taxpayer’s worldwide organisational and ownership structure (including global organisation chart and significant changes in the relationship, if any), covering all associated persons whose transactions directly or indirectly affect the pricing of the documented transactions.” IRBM Comments:

This information can be extracted from the global organisation chart if the group provides the information. Details on global organisation/subsidiaries/affiliates e) Please explain the definition of “Affiliate Companies”. Kindly clarify the terminology for subsidiaries and affiliates. IRBM Comments:

In general, the affiliate is used primarily to describe a business relationship wherein one company owns less than a majority stake in the other company’s share.

Address f) Please confirm if the “Address” here refers to Registered Address or the Address of the Business Premise? IRBM Comments: Address of the Business Premise g) This information does not fall within the documentation requirements for the preparation of an MTPD as outlined in Para 11.2.4 (a), (c) and (d) of the 2017 TPGL. As such, we would suggest removing this disclosure requirement from the MTPD template. IRBM Comments: The requirement of this information is stipulated under Para 11.2.4(c)(ii) of the MTPGL. Tax Identification Number (TIN) h) This information does not fall within the documentation requirements for the preparation of an MTPD as outlined in Para 11.2.4 (a), (c) and (d) of the 2017 TPGL.

As such, we suggest removing this disclosure from the MTPD template. IRBM Comments: The Tax Identification Number (TIN) refers to Income Tax Reference Number. During the 2022 Budget Speech tabled in the Dewan Rakyat on Friday, 29 October 2021, the government announced the implementation of a tax identification number (TIN) to be implemented beginning year 2022 to broaden the income tax base.

Please refer to frequently asked questions on implementing the tax identification numbers published on 31 December 2021. i) Please confirm if that TIN does not apply to companies outside Malaysia. This would entail a significant amount of work for taxpayers, defeating the MTPD template’s purpose. IRBM Comments: The Tax Identification Number (TIN) can be provided if available. Organisational chart j) Under item B7.3 Description of the management, kindly provide an example of the IRBM’s expectation from the taxpayer in providing the said chart

. IRBM Comments: Depends on how the taxpayer’s group structure is organised.

4. Controlled transactions

CTIM Comments

- Item 1 – Particulars of Transactions with Related Companies Outside Malaysia and

- Item 2- Particulars of Transactions with Related Companies In Malaysia

a) We request that IBM consider inserting a new column to explain the “nature of the related party transactions”. This is because the ‘type of transaction’ may be insufficient for the readers to understand the detailed transaction.

Also, taxpayers may have difficulty recalling the transaction details in a tax audit. IRBM Comments: We take note of CTIM’s suggestion. This information is extracted from Form C, Part N for YA 2018 and prior or Item F8 (Attachment) of Form C YA 2019 onwards. Any Valid contract/ Commercial agreement b) If the taxpayer has entered into several agreements (e.g. 10 related party sales agreements), will a sample be sufficient to complete the template? What is the minimum sample agreement to be included?

Furthermore, in practice, third parties rarely enter into contracts for purchase of raw materials/sale of goods as these are normally documented by way of purchase orders, invoices etc.

As such, from an arm’s length behaviour perspective, it is not practical for related parties to maintain such agreements. IRBM Comments: Any document that supports the pricing policy is acceptable. % of Related Party Transactions/Total Transactions c) Please provide the definition of “total transactions”. For instance, for C1 “sales/revenue”, it could mean % of related party sales over the taxpayer’s total sales.

Similarly, for C1 “purchases”, it could mean % of related party purchases over total purchases of the taxpayer.

However, having different denominators/bases can create challenges, especially regarding other income, royalty, management fees, rent, interest, etc., because these are generally incidental to the main business, and the taxpayer may not have similar transactions with third parties.

For simplicity, we suggest expressing all income statement’s controlled transaction items as a % of the net sales/revenue. This would already provide IRBM with an indication of the extent of controlled transactions relative to the overall business size of the taxpayer. For balance sheet items, such as loans, and sales and purchases of non-current assets, CTIM would like to suggest leaving the last column (i.e. % of Related Party Transactions/Total Transactions) blank because expressing these items as a % of net sales (or such other base) may be misleading. IRBM Comments: The term used in the template and the examples will be explained in the Guide Notes to the template which will be issued. d) Does the “Amount” of the loan to/from the associated person required in this template refers to the amount provided or received during the current year of assessment or the outstanding balance at the end of the year? IRBM Comments: The amount refers to the outstanding balance as of the year-end of the financial accounting period. e) Please clarify the purpose of disclosing the details on dividends received/ paid by the taxpayer, as these transactions fall outside the purview of TP. IRBM Comments: Amendments will be made to remove the item ‘Dividend’ in the template. Pricing policy (For Each Type of Controlled Transaction) CTIM Comments a) It is noted that this section requires taxpayers to provide the pricing policy for each type of controlled transaction.

This requirement is counter-productive because an MTPD is to ease the compliance burden of taxpayers who do not have substantially related party transactions.

As such, this section should be simplified by only requiring the disclosure of the pricing policy for the main/key-related party transaction(s).

The main/key-related party transaction(s) may be determined through the imposition of thresholds for each type of transaction.

Where the transaction amounts fall below a specific threshold, such transactions should be exempt from being covered within the MTPD template.

IRBM Comments: We take note of CTIM’s comments. Part of this issue has been addressed in the new draft of MTPGL.

b) Not every transaction is priced on a cost-plus-mark basis, as some could be negotiated on a competitive or market-based.

It will be impractical, especially for MTPD, which aims to reduce compliance costs for the taxpayer to determine the cost components and the markup the related companies applied.

IRBM Comments: The cost components refer to basis of costs used for the determination of price during the negotiation process. Other method can be used to explain the pricing as long as the taxpayer can justify how they compute. c) The MTPD template only requires taxpayers to disclose the formula adopted (which may include the element of costs and the anticipated profit mark-up). However, in the case where the transfer price is not on a cost plus basis, for example rental rate or interest rate, how would IRBM expect the taxpayer to disclose this. IRBM Comments: The determination of how the taxpayer derived the transaction price. The anticipated profit markup price does not refer to the transfer pricing method – cost-plus basis, as other methods are also acceptable. It generally refers to an estimated return expected for that particular transaction. The MTPD template does not restrict the taxpayer to disclose only the formula adopted method. It would depend on the TP method the taxpayer deems appropriate for the transaction. d) Sample pricing policy – are companies that meet the MTPD threshold required to prepare and maintain a pricing policy?

IRBM Comments: Any form of computation or documents can be provided to support the pricing mechanism used in the transaction. e) Comparability study – for clarity, it must be made clear whether a comparability analysis is required as opposed to “if any”.

From a practical perspective, it is almost impossible (unless there are clear CUPs) for a company to substantiate that its prices are at arm’s length without a comparability study or at least some form of a general benchmarking study.

IRBM Comments: We take note of CTIM’s comments. This issue has been addressed in the new draft of MTPGL.

f) The comparability study involves benchmarking. Where TNMM is applied, it is common for taxpayers outside the scope of Paragraph 1.3.1 to prepare one entity-level TNMM analysis to test all income statement’s controlled transactions (up to EBIT level) on an aggregate basis.

For example, a taxpayer may not perform separate benchmarking studies for related party purchases and related party sales. Instead, they might test these two transactions in aggregate through an entity-level TNMM analysis. This approach is administratively simpler and cost-effective.

As item D reads “For Each Type of Controlled Transaction”, please clarify that separate benchmarking studies for each controlled transaction would not be required in the MTPD, and the entity-level TNMM analysis (where applicable) will continue to be accepted by the IRBM.

IRBM Comments:

We take note of CTIM’s comments. This issue has been addressed in the new draft of MTPGL.