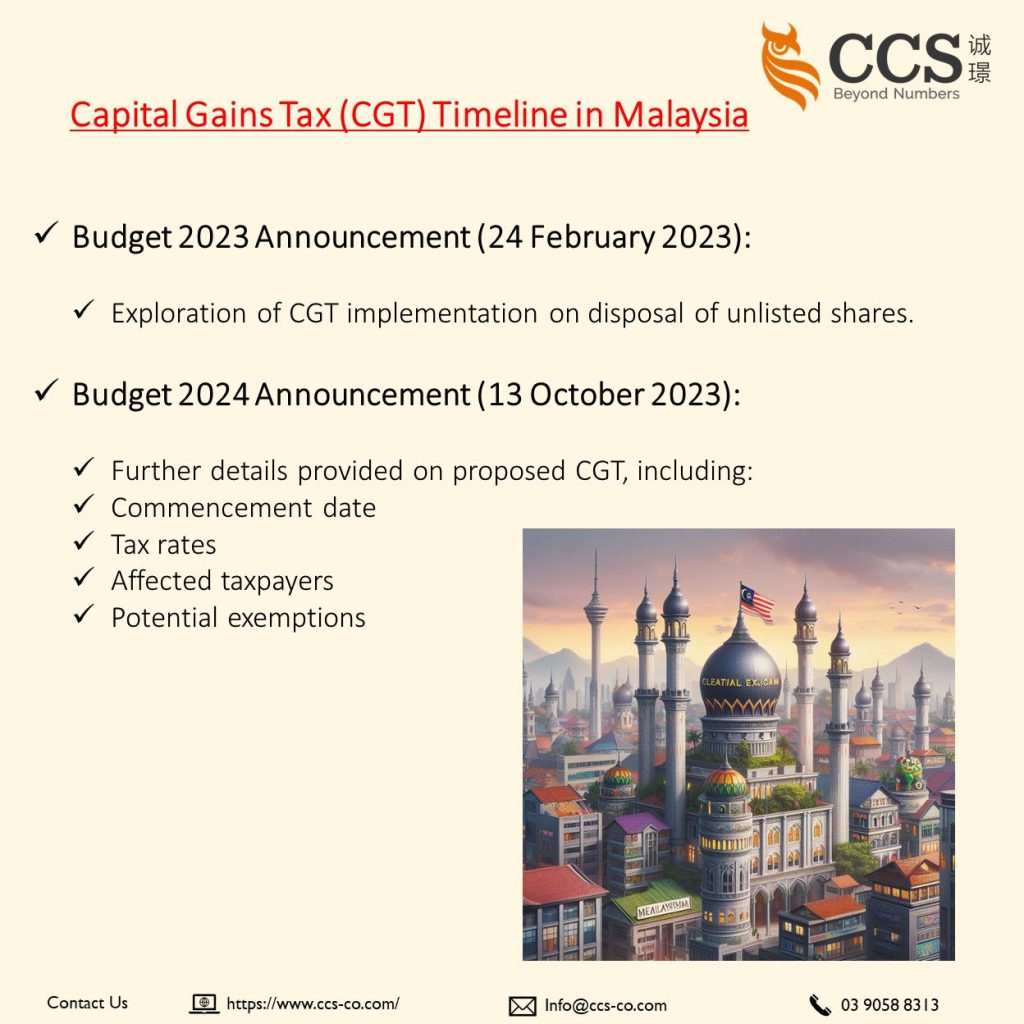

Following the re-tabling of Malaysia’s Budget 2023 on 24 February 2023, it was announced that the Government would explore the implementation of a capital gains tax (CGT) on the disposal of unlisted shares by companies at a reduced rate.

Subsequently, the Budget 2024 announcement on 13 October 2023 provided further elaboration on this proposal, including details such as the proposed commencement date, tax rates, affected taxpayers, and potential exemptions.

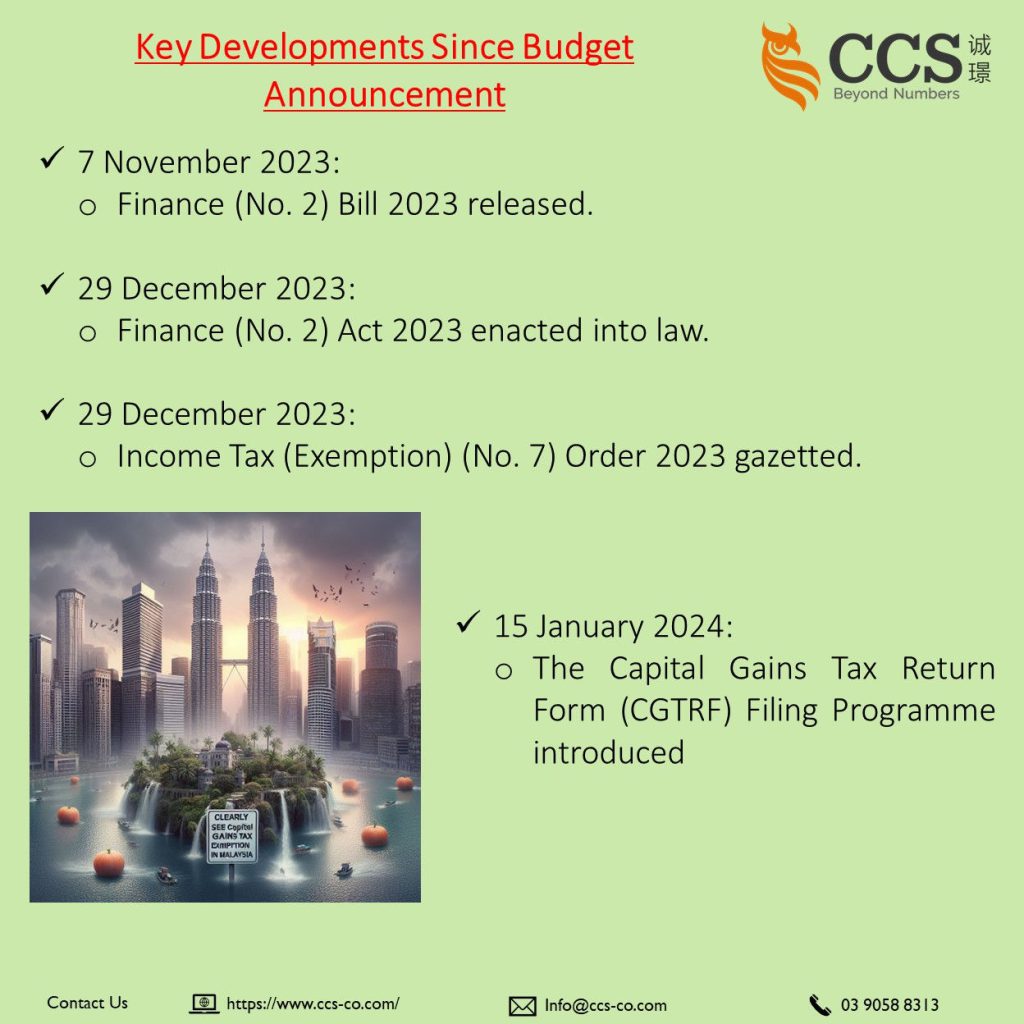

Since the Budget announcement, several developments have occurred:

- On 7 November 2023, the Finance (No. 2) Bill 2023 (Bill) was released and presented for its initial reading.

- On 29 December 2023, the Finance (No. 2) Act 2023 (Finance Act) was officially enacted into law after being gazetted. The Finance Act encompasses all the amendments proposed in the Bill.

- Additionally, on 29 December 2023, the Income Tax (Exemption) (No. 7) Order 2023 [P.U.(A) 410] (Exemption Order) was gazetted, providing exemptions related to CGT and deferring the effective date for CGT concerning certain disposals.

- On 15 January 2024, the Inland Revenue Board (HASiL) introduced the Capital Gains Tax Return Form (CGTRF) Filing Programme, which is set to take effect from 1 March 2024.

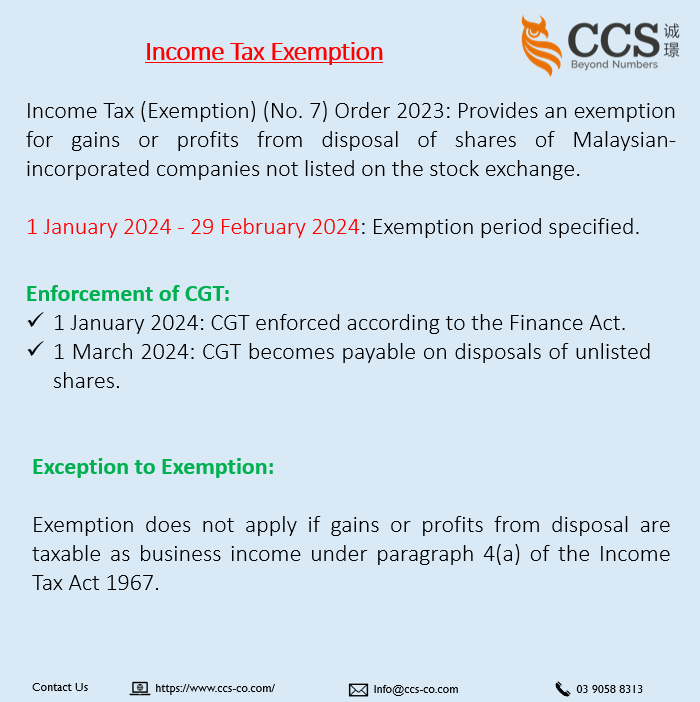

It is worth noting that according to the Finance Act, CGT will be enforced starting 1 January 2024.

However, the Income Tax (Exemption) (No. 7) Order 2023 [P.U. (A) 410/2023] provides that a company, LLP, trust body, or co-operative society is given an income tax exemption to any gains or profits received from the disposal of shares of a company incorporated in Malaysia not listed on the stock exchange.

This exemption applies to such disposals from 1 January 2024 to 29 February 2024.

Hence, CGT will only be payable on disposals of unlisted shares in Malaysian-incorporated companies from 1 March 2024.

The order specifies an exception to the exemption of income tax on profits or gains from the disposal of shares.

Specifically, the exemption does not apply to a disposal of shares where the gains or profits are taxable as business income under paragraph 4(a) of the Income Tax Act 1967.

This means that if the gains or profits from the disposal of shares are considered business income, they will not be eligible for the tax exemption outlined in the order.

Reference:

Income Tax (Exemption) (No. 7) Order 2023