This chart describes e-Invoice requirements for business expenses.

It distinguishes between situations where e-Invoices are not required and those where self-billed e-Invoices are mandatory.

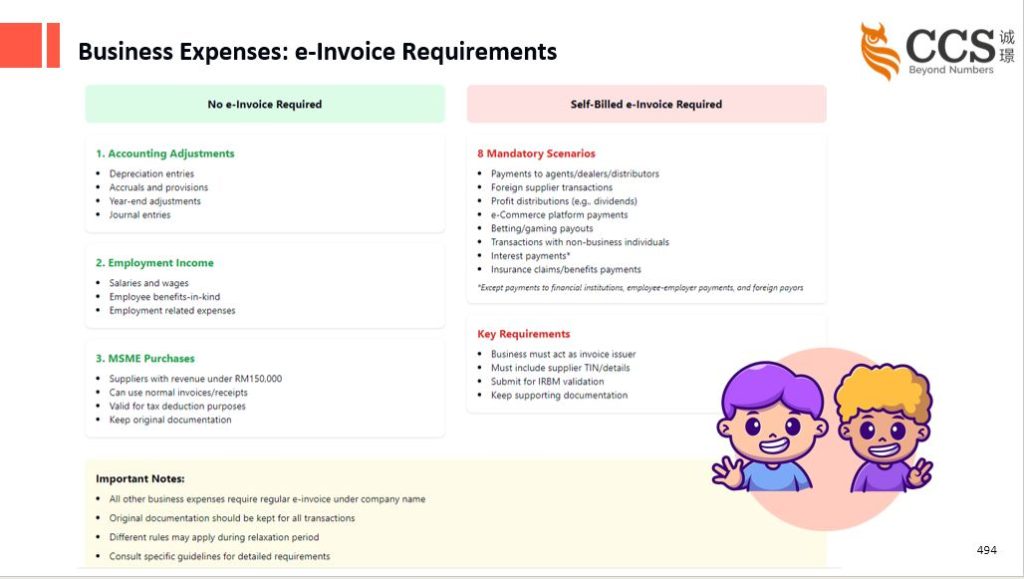

1. No e-Invoice Required

These expenses do not require an e-Invoice. Businesses can use normal invoices or receipts for these categories:

- Accounting Adjustments:

Includes depreciation entries, accruals, and year-end adjustments.

Example: Recording depreciation for company machinery at year-end. - Employment Income:

Covers salaries, wages, and employee-related benefits.

Example: Monthly salary payments to employees or medical benefits paid by the employer. - MSME Purchases:

Purchases from suppliers with annual revenue below RM150,000.

Example: Buying office supplies from a small local business earning less than RM150,000 annually.

2. Self-Billed e-Invoice Required

8 Mandatory Scenarios require businesses to issue self-billed e-Invoices:

- Payments to agents/dealers/distributors

Example: Commission payments to a distributor for product sales. - Foreign supplier transactions

Example: Paying a foreign software company for licensing fees. - Profit distributions (e.g., dividends)

Example: Distributing annual dividends to company shareholders. - e-Commerce platform payments

Example: Paying fees to an e-commerce platform like Lazada or Shopee. - Betting/gaming payouts

Example: A gaming company paying out winnings to players. - Transactions with non-business individuals

Example: Renting a space from an individual for a corporate event. - Interest payments

Example: Paying interest on loans to private lenders (not financial institutions). - Insurance claims/benefits payments

Example: Insurance reimbursements for company vehicles or property.

Key Requirements for Self-Billed e-Invoices

- The business must issue the e-Invoice itself.

- Supplier details and tax information (TIN) must be included.

- The e-Invoice must be validated by the IRBM (Inland Revenue Board of Malaysia).

- Proper documentation must be maintained for audits.

Important Notes

- All other business expenses require regular e-Invoices under the company’s name.

- Retain original documentation for all transactions.

- Special rules may apply during the transition/relaxation period.

- Refer to specific guidelines for details on compliance.

此图描述了企业费用的电子发票要求,区分了无需开具电子发票的情况和必须开具自开电子发票的情况。

1. 无需开具电子发票

以下费用类别无需电子发票,企业可使用普通发票或收据:

- 会计调整:

包括折旧分录、应计项目以及年终调整。

例子:在年终记录公司设备的折旧费用。 - 员工收入:

包括工资、薪水以及与员工相关的福利。

例子:向员工支付月薪或为员工支付医疗福利。 - 微型企业采购 (MSME Purchases):

向年收入低于RM150,000的供应商采购。

例子:从年收入低于RM150,000的小型本地企业购买办公用品。

2. 必须开具自开电子发票

以下8种场景必须开具自开电子发票:

- 支付给代理/经销商/分销商

例子:向分销商支付产品销售佣金。 - 外国供应商交易

例子:支付给外国软件公司的许可费用。 - 利润分配(例如股息)

例子:向公司股东分配年度股息。 - 电子商务平台支付

例子:支付给Lazada或Shopee等电子商务平台的费用。 - 博彩/游戏支出

例子:游戏公司向玩家支付奖金。 - 与非商业个人的交易

例子:租用个人的场地举办公司活动。 - 利息支付

例子:支付给私人贷款人的贷款利息(非金融机构)。 - 保险索赔/福利支付

例子:公司车辆或财产的保险赔偿。

自开电子发票的关键要求

- 企业需自行开具电子发票。

- 必须包含供应商的详细信息和税号 (TIN)。

- 发票必须经过马来西亚税务局 (IRBM) 验证。

- 保存完整的文档以备审计。

重要说明

- 其他业务费用需以公司名义开具常规电子发票。

- 所有交易需保留原始文档。

- 在过渡期/宽限期内可能有特殊规则适用。

- 请参阅具体指南以获取合规细节。