Clinic and Taxman Lock Horns Over Expense Deductions

A clinic wanted to reduce some of their expenses on their tax return. But the taxman looked deeper into some of the expenses, including: and didn’t seem to agree. Instead, the clinic said these expenses were related to caring for patients and selling healthcare products and were, therefore, very important expenses for the business. However, […]

Sales Incentives Ruled Business Expenses, Not Entertainment

Here is an analysis of the Khind-Mistral (Borneo) Sdn Bhd tax case: Introductory Paragraph This is an income tax case involving the deductibility of sales incentive trips provided by Khind-Mistral (Borneo) Sdn Bhd (“Company”) to its dealers who achieved sales targets. The trips were claimed as deductible expenses under Section 33(1) of the Income Tax […]

Navigating the Rules: Traveling Expenses and Tax Deductions

Introduction The deductibility of travel expenses has been a common issue disputed between taxpayers and tax authorities. Several landmark UK tax cases have established important principles that guide the resolution of such disputes in Malaysia as well. Revenue Law Under Malaysian tax law, expenses are deductible under Section 33(1) if they are wholly and exclusively […]

Initial Financing Costs Sink Manufacturers’ Tax Appeal

PM v DGIR, PR v DGIR, PI v DGIR 20.1.2020 The petitioners are called PM, PR, and PI, which seem to be abbreviations for company names. Obtaining financing can be costly for businesses, but can those costs be deducted against taxable income? Three manufacturing companies found out that the answer is often no, as tax […]

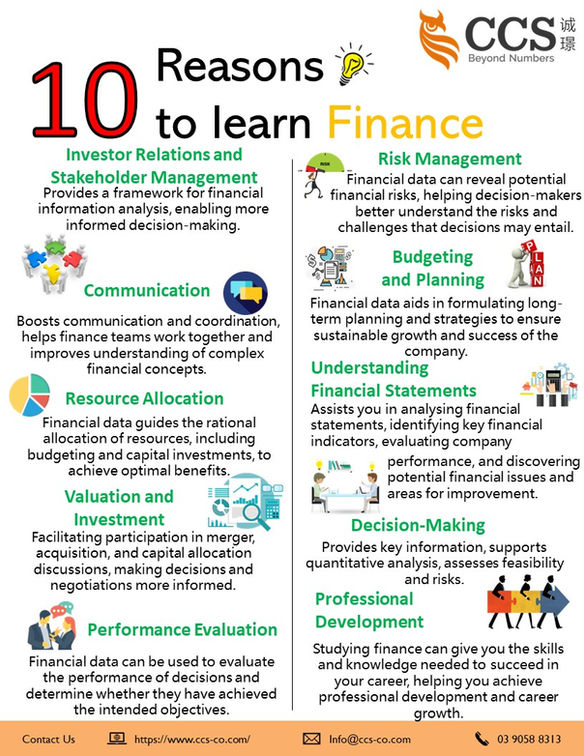

10 Reasons to Learn Finance

Disclaimer: The articles, templates, and other materials on our website are provided only for your reference. While we strive to ensure the information presented is current and accurate, we cannot promise the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk. If you intend […]

Trading or Investing? Court Draws the Line for Investors for Tax Purposes

Dr Zanariah Ramli v Ketua Pengarah Hasil Dalam Negeri Court of Appeal 2013 Introduction This case involved an appeal by the Inland Revenue Board (IRB) against the Special Commissioners of Income Tax (SCIT) decision, which held that profits made by Dr Zanariah Ramli from buying and selling bonds were capital gains not subject to income […]

Deduction for Expenses in relation to Listing on Main, ACE Market or LEAP Market

Effective from the year of assessment 2018 until the year of assessment 2023, the Minister makes the Income Tax (Deduction for Expenses in relation to Listing on the Main Market, Access, Certainty, Efficiency (ACE) Market or Leading Entrepreneur Accelerator Platform (LEAP) Market of Bursa Malaysia Securities Berhad) Rules 2023 [PUA 235_2023] under paragraph 154(1)(bb) of […]

Luxury Apartment Developer Fails to Prove Gains are Capital, Taxed as Trading Income Instead

BEVERLY TOWER DEVELOPMENT SDN BHD v. KETUA PENGARAH HASIL DALAM NEGERI High Court Malaya, Kuala Lumpur 10 August 2022 This was an appeal by Beverly Tower Development Sdn Bhd against the decision of the Special Commissioners of Income Tax (“SCIT”), which held that the gains from the disposal of 50 apartment units were trading receipts […]

Deduct or Not Deduct? – The Murky Tax Waters Around Bumiputera Quota Release Payments (Discount)

This involves two court cases where property development companies claimed a tax deduction on payments made to the state housing authority to obtain the release of unsold Bumiputera quota units to be sold to non-Bumiputera buyers. Case No 1: Ketua Pengarah Hasil Dalam Negeri v Taman Equine (M) Sdn Bhd Case No 2: Ketua Pengarah […]

Income Tax (Exemption) Order 2023: 5-year Tax Exemption for Manufacturers Relocating to Malaysia

The Income Tax (Exemption) Order 2023, which is deemed to have taken effect from the year of assessment 2021, introduces a tax exemption for existing manufacturing companies that relocate their operations to Malaysia. To qualify, companies must: The tax exemption is on statutory income derived from qualifying new manufacturing activities. It is equivalent to the […]