Amendments to MFRS 17 Insurance Contracts

The IASB has been monitoring the implementation of IFRS 17 Insurance Contracts since it was announced in May 2017. IFRS 17 is one of the largest accounting changes in insurance in the last decade, impacting insurance firms’ entire operating model. During the meeting in October 2018, the Board came up with a list of 25 […]

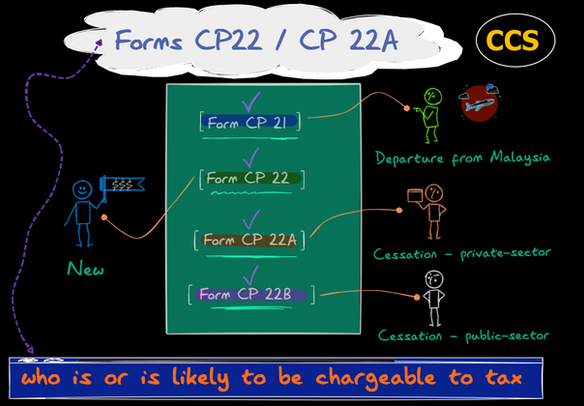

IRBM’s Response to CTIM on Forms CP 22 / CP 22A

Mandatory adoption of Prescribed Forms CP 21, CP 22, CP 22A and CP 22B effective from 1 January 2022 Effective January 1, 2021, under the amendments to subsections 83 (2), (3), and (4) of the Income Tax Act 1967, Forms CP 21, CP 22, CP 22A, and CP 22B must be submitted by the employers […]

Conceptual Framework for Financial Reporting | 财务报告概念框架

Introduction Since its founding in 2001, the International Accounting Standards Board (IASB) has had a profound impact on the global landscape of financial reporting for companies. But it was the International Accounting Standards Committee (IASC), during its 27 years of existence from 1973 to 2000, that laid the groundwork for the International Accounting Standards Board […]

What Function Does the International Auditing and Assurance Standards Board(IAASB)Play?

The International Auditing and Assurance Standards Board, also known as the IAASB, is responsible for setting the International Standards on Auditing (ISAs). It is an independent body that sets international standards of high quality on aspects of: The International Auditing and Assurance Standards Board were established in March 1978. Before that, it was known as […]

Independence

According to IESBA, ‘… enables the auditor to form an opinion without being affected by influences that would compromise the auditor’s professional judgement. Independence of mind will allow the auditor to act with integrity and exercise objectivity at all times during the course of the audit. Independence of mind will also allow the auditor to […]

Improving Audit Quality 2: What is Audit Quality?

Sadly, there is no one agreed-upon definition of what constitutes a quality audit. The Center for Audit Quality (CAQ) identifies the following as the two primary pillars around which audit quality is built: (*) Independence refers to external auditors’ interests being independent of those of company management Several elements determine the quality of an audit; […]

Improving Audit Quality 3: An Overview of ISQM 1 – Firm’s System of Quality Management

What? The International Standard on Quality Management 1 (ISQM 1) – Quality Management for Firms that Perform Audits or Reviews of Financial Statements, or Other Assurance or Related Services Engagements strengthens firms’ quality management systems by taking a robust, proactive, and effective approach to quality management. The standard encourages firms to design a system of quality […]

Improving Audit Quality 1: An Overview

Back to N Years Ago When I was younger (wow, this makes me feel so old), audit quality was not really a “thing.” I watched my superiors perform audits they believed to be sufficient, and my colleagues and I were taught to follow in their footsteps. We conducted what we believed to be good audits […]

ISQC 1: Documentation of the System of Quality Control

对质量控制制度的记录 Para 57 The firm shall establish policies and procedures requiring appropriate documentation to provide evidence of the operation of each element of its system of quality control. (Ref: Para. A73–A75) 会计师事务所应当制定政策和程序,要求形成适当的工作记录,以对质量控制制度的每项要素的运行情况提供证据。 (参见:第 A73-A75 段) Para 58 The firm shall establish policies and procedures that require retention of documentation for a period of time sufficient […]

ISQC 1: Monitoring

Monitoring 监控 Monitoring the firm’s quality control policies and procedures 监控会计师事务所的质量控制政策和程序 Para 48 The firm shall establish a monitoring process designed to provide it with reasonable assurance that the policies and procedures relating to the system of quality control are relevant, adequate, and operating effectively. This process shall: 会计师事务所应当制定监控政策和程序,以合理保证与质量控制制度相关的政策和程序具有相关性和适当性,并正在有效运行。监控过程应当: Evaluating, Communicating and Remedying Identified Deficiencies […]