Implementation of e-TT system for TT / EFT and Interbank GIRO (IBG) Payment Methods

IRBM released a Media Release on implementing an e-TT system for Telegraphic Transfer (TT) / Electronic Fund Transfer (EFT) and Interbank GIRO (IBG) payment methods on March 3, 2022. The Media Release can be found here:- Beginning on April 1, 2022, this new system will be in place and be known as the e-TT system. […]

Tax Audit

A tax audit is at the top of the list of difficulties that no business wants. A tax audit might induce panic regardless of how carefully you operate your business. Remember that a tax audit is merely an annoyance for most business owners. However, it would help if you were prepared for this inconvenience. 税务审计是任何企业都不希望遇到的。无论你如何谨慎经营你的企业,税务审计可能会诱发恐慌。请记住,对大多数企业主来说,税务审计只是一种烦扰。然而,你必须为这种不便做好准备。 […]

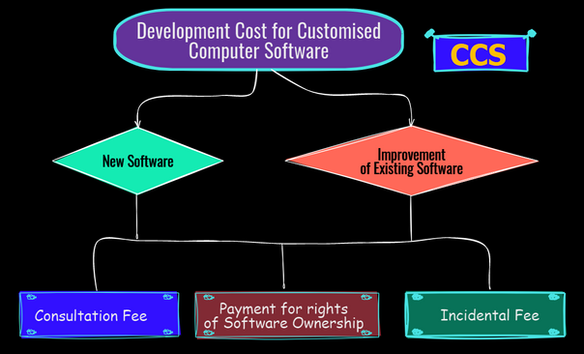

IRBM’s Response to CTIM’s Development Cost for Customised Computer Software

Income Tax (Capital Allowance) (Development Cost for Customised Computer Software) Rules 2019 On 3 October 2019, the Minister, in the exercise of the powers conferred by paragraphs 154(1)(b), 33(1)(d) and paragraphs 10 and 15 of Schedule 3 to the Income Tax Act 1967 [Act 53], gazetted the Income Tax (Capital Allowance) (Development Cost for Customised […]

The latest updates and issues in claiming RA for Manufacturing Activities

The Reinvestment Allowance (RA) is an incentive provided to Malaysian resident companies involved in the manufacturing industry and specified agriculture sector. The purpose of this incentive is to encourage these companies to reinvest and grow their companies. Eligibility to Claim Reinvestment Allowance For these companies to be eligible for the RA incentive, they must have […]

MOF – TERAS 2.0 for the Application and Renewal of Tax Agent Licence

In order to facilitate the application for and renewal of income tax agent licences, the MyCukai Single Sign On (SSO) has been upgraded to the TERAS 2.0 (“Treasury Authentication System 2.0”) authentication system. In order to continue with the process of renewing their income tax agent licences, users of MyCukai are needed to first register […]

Exemption Orders – Foreign-Sourced Income

Introduction Before the 1st of January 2022, Foreign sourced income remitted back to Malaysia was exempt from taxation per Schedule 6 paragraph 28 of the Income Tax Act 1967 (ITA). Budget 2022 The amendment to Schedule 6 paragraph 28 proposed by the Budget 2022 to take effect on 1 January 2022 will remove the exemption for […]

Tax Incentive for Investment in a Bionexus Status Company

Principal Rules – Tax Incentive According to the Income Tax (Deduction for Investment in a BioNexus Status Company) Rules 2016 [P.U.(A) 306/2016]: Amendment Rules On 22 June 2022, the Minister, in the exercise of the powers conferred by paragraph 154(1)(b) of the Income Tax Act 1967 [Act 53], gazetted the Income Tax (Deduction for Investment […]

2% WHT on payments made to agents, dealers & distributors: Amendment to the Procedure for Operation

Introduction Section 107D of the Income Tax Act of 1967 (ITA) was introduced on January 1, 2022, to compel companies making monetary payments to agents, dealers, or distributors originating from sales, transactions, or schemes to withhold tax at a rate of 2% on the gross amount. This pertains to payments to agents, dealers or distributors […]

Partnership Accounts

Keeping the books of a partnership is often done in the same manner as maintaining the books of a sole proprietorship, with the following exceptions: We have written some articles on partnership accounts that you might find helpful: Partnerships In Malaysia – Theory How does a Partnership Operate Special Accounts for Partnerships Partnership Formation Accounting […]

Taxation of Partnerships – Capital Allowance

Since a partnership is not a legal person it cannot own fixed assets. These, therefore, belong jointly to the individual partners. Those who own the plant or machinery and use it in the course of their trade, business, or profession are the ones who are generally eligible for the capital allowances. Nevertheless, a notable exemption is […]