Amendments to MFRS 3 – Reference to the Conceptual Framework

The Accounting Requirements for Business Combinations have not been altered due to the amendments made to MFRS 3 Business Combinations; instead, MFRS 3’s reference to the Conceptual Framework for Financial Reporting has been brought up to date. In addition, the amendments make it clear that contingent assets should not be recognised at the acquisition date. An […]

Annual Improvements to MFRS Standards 2018–2020

Annual Improvements provide a mechanism for dealing efficiently with a collection of minor amendments to MFRS Standards. The Annual Improvements to MFRS Standards 2018–2020 covers amendments to: An entity shall apply that amendment for annual reporting periods beginning on or after 1 January 2022. Earlier application is permitted. If an entity applies the amendment for […]

Amendments to MFRS 101 on classification of Liabilities as Current or Non-Current

On 23 January 2020, the International Accounting Standards Board (often known as the “IASB”) published amendments to paragraphs 69 to 76 of the IAS 1 Presentation of Financial Statements. The amendments clarify: In this context, the Malaysian Accounting Standards Board (commonly known as “MASB”) has decided to implement the same amendments for MFRS 101. Amendments […]

Amendments to MFRS 112 on deferred tax related to Assets and Liabilities

TIAS 12 Income Taxes When an entity recognises assets or liabilities for the first time, under IAS 12, the entity is exempted from recognising any deferred taxes. There has been a degree of ambiguity regarding the applicability of this exemption to circumstances in which an asset and a liability are simultaneously recognised in the course […]

Amendments to MFRS 17 Insurance Contracts

The IASB has been monitoring the implementation of IFRS 17 Insurance Contracts since it was announced in May 2017. IFRS 17 is one of the largest accounting changes in insurance in the last decade, impacting insurance firms’ entire operating model. During the meeting in October 2018, the Board came up with a list of 25 […]

Amended Guidelines on Application for Stamp Duty Relief

The IRB published the following guidelines on March 24, 2022: The Guidelines take the place of the previous Guidelines, which were issued on February 26, 2019. These guidelines were issued to explain the procedures involved in applying for stamp duty relief in the reconstruction or amalgamation of companies provided under Section 15 of the Stamp […]

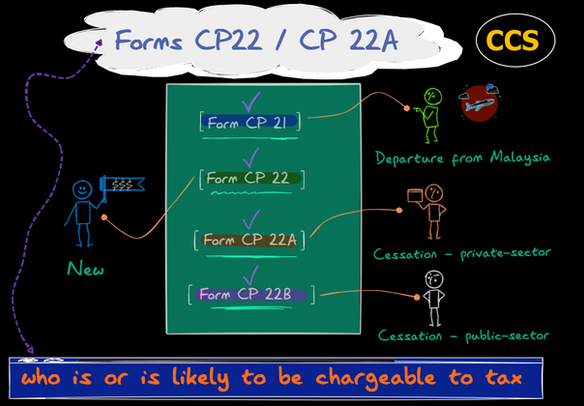

IRBM’s Response to CTIM on Forms CP 22 / CP 22A

Mandatory adoption of Prescribed Forms CP 21, CP 22, CP 22A and CP 22B effective from 1 January 2022 Effective January 1, 2021, under the amendments to subsections 83 (2), (3), and (4) of the Income Tax Act 1967, Forms CP 21, CP 22, CP 22A, and CP 22B must be submitted by the employers […]

Implementation of e-TT system for TT / EFT and Interbank GIRO (IBG) Payment Methods

IRBM released a Media Release on implementing an e-TT system for Telegraphic Transfer (TT) / Electronic Fund Transfer (EFT) and Interbank GIRO (IBG) payment methods on March 3, 2022. The Media Release can be found here:- Beginning on April 1, 2022, this new system will be in place and be known as the e-TT system. […]

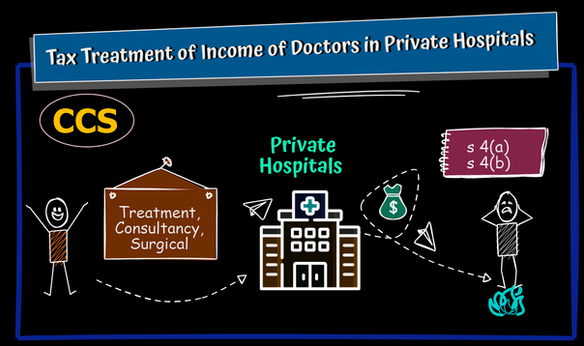

Tax Treatment on the Income of Doctors in Private Hospitals

I am sure many of you will still remember the widespread allegation that doctors (from now on referred to as the doctor) who provide medical services (e.g., treatment, consultancy, surgical, etc.) in Private Hospitals were evading taxes many years ago, and LHDN conducted audits as a result. It is not only permissible but common to […]

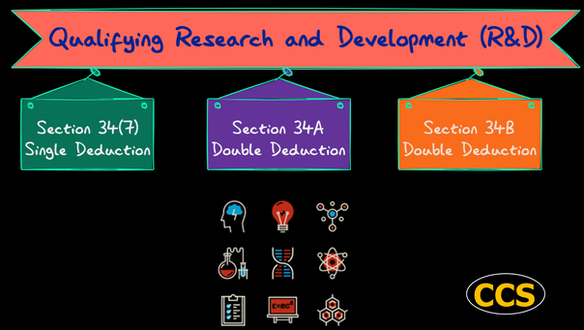

Guidelines on the application procedure for a Special Deduction in respect of a Qualifying R&D

Guidelines on the application procedure for a special deduction in respect of a Qualifying R&D On August 13, 2020, the guidelines on the application procedure for a special deduction in respect of a qualifying research and development (R&D) were issued by the Inland Revenue Board of Malaysia (“IRBM”). These guidelines explain the application process for an […]