The Risk-Based Audit: Overview

The auditor’s overall objectives, as stated in ISA 200.11, can be summarised as follows: Reasonable Assurance Reasonable assurance is a high but not absolute level of assurance. It is obtained when the auditor has obtained sufficient appropriate audit evidence to reduce audit risk (that is, the risk that the auditor expresses an inappropriate opinion when […]

The International Standards on Auditing (ISAs)

Structure of the ISAs | 国际审计准则的结构 The ISAs have a standard structure, as outlined below. Introduction An explanation of the purpose and scope of the ISA, including how the ISA relates to other ISAs, the subject matter of the ISA, specific expectations on the auditor and others, and the context in which the ISA is […]

Salary to Senior Citizens, IRB disallowed Double deduction claim, CCS Successfully defends

In claiming a Double Tax Deduction for remuneration paid to an employee who reaches the age of 60 in the middle of the year, is the remuneration to be prorated to exclude the portion of his remuneration that relates to the period prior to reaching the age of 60? Few senior citizen employees of our […]

When doing a Risk Assessment on a client, what does an auditor look at?

Because risk is such a significant component of an audit, it is of the utmost significance that auditors approach risk evaluation with the utmost caution. The auditor is tasked with several overall objectives, one of which is to identify the risks that a company faces (both business risk and the risk of material misstatement) and […]

What is the concept of ‘Materiality’, and how is it applied in an Audit?

The word “materiality” basically means how important or significant something is in relation to the financial statements as a whole. ISA 320 Materiality in Planning and Performing an Audit says [defines] the following about the term: ‘A matter is material if its omission or misstatement would reasonably influence the economic decisions of users taken on […]

IRBM consented to withdraw the petition to wind up the company.

When the taxpayer came to us, it was in breach of his statutory responsibility under Section 77A(1) of the Income Tax Act 1967 (the Act) for not submitting or filing his tax return for the YA 2020 within the time due to MCO. This was because the taxpayer needed help to finalise their accounts due […]

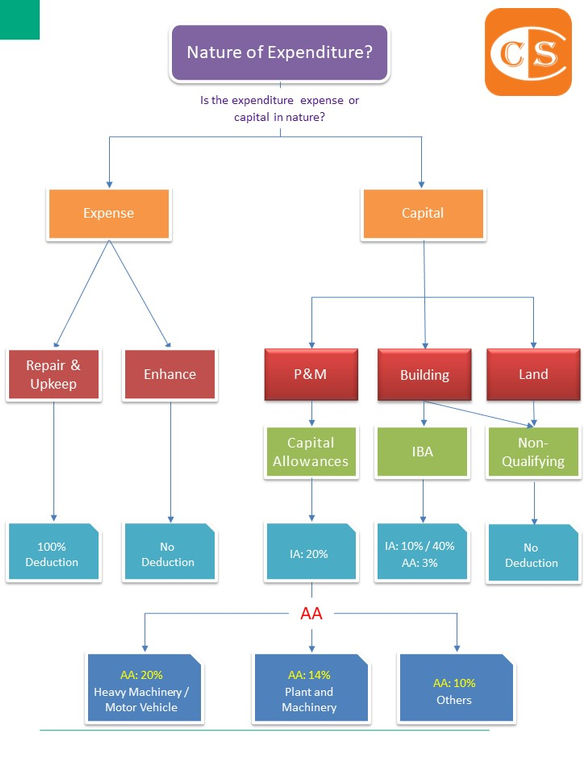

Determining Qualifying Expenditure for Capital Allowances & ”Repair or Upkeep”

Capital Allowances are a complex tax technical area largely governed by case law and precedent. As illustrated in Fig. below, before calculating the Capital Allowances available in respect of capital expenditure incurred, two criteria must be considered: 资本津贴在税收技术领域来说是一个复杂概念,主要受案例法 (Case Law) 和先例的制约。 如上图所示,在计算发生的资本支出可获得的资本津贴额之前,首先必须考虑两个标准:- Expenses on Repairs and Renewals In most cases, a person can reduce their […]

马来西亚税收局提出上诉,反对肾脏基金会的免税地位法律申请

翻译自新闻来自:当今大马的新闻 案情背后:1970年,马来西亚内陆税收局 (IRB) 根据1967年所得税法令 (ITA) 第44(6)(a)条授予国家肾脏基金会 (National Kidney Foundation, NKF) 免税地位。 然而,在2019年的税务审计 (Tax Audit) 后,据称 IRB 决定撤销免税地位,并在2020年7月向NKF提出税务评估 (Tax Assessment)。 NKF 于同年9月17日提出法律质疑,并将 IRB 列为被告。 根据司法审查申请的副本,该基金会寻求法院的命令,撤销 IRB 在2020年6月17日的信函中据称撤销其免税地位的决定。 NKF 声称 IRB 的这项决定是 #非法的、#无效的、#不合法的和/ #或超越权限的、#不合理的和 / #或不讲道理的,等等。 NKF 要求法院宣布 “#被申请人在法律上无权对像申请人这样的慈善组织施加任意和单方面的条件,#而这些条件并没有包含在批准信中和 / #或传达给申请人“。 根据基金会主席 Zaki Morad Mohamad Zaher 博士支持司法审查的宣誓书副本,申请人认为 IRB 未能理解 ITA 的规定,即经批准的慈善组织,只要其机构不以盈利为主要目的,其为慈善目的而获得的收入可免于纳税。 有关的 ITA 条款是第44(6)条和该法案附表6的第13段一起阅读。 NKF 辩称,IRB 没有考虑到上级法院的既定法律先例,即由于既得权利原则的适用,经批准的慈善组织有权获得免税。 […]

How does the Auditor plan for an Audit of Financial Statements?

Planning an audit is one of the most integral parts of the audit. Without a sufficient planning programme on the auditor’s part, there is a significant risk that a material misstatement (or many material misstatements) will be missed. This will lead to the auditor expressing an inaccurate audit opinion, in addition to additional implications. Planning […]

What happens when an Auditor finds a Material Error?

The ability of the auditor to express an opinion as to whether or not the financial statements reflect a true and fair view (or present fairly in all material respects) of the company’s financial situation is the fundamental objective of the audit. During the course of their work, the auditor is required to maintain a […]