Section 107C pertains to the estimation of tax payable and the payment of tax by instalments for companies, limited liability partnerships, trust bodies, or co-operative societies.

Here’s a breakdown of the key provisions:

Estimation of Tax Payable (107C(1)-(3)):

Entities must provide an estimate of their tax payable for each assessment year to the Director General.

This estimate, made in the prescribed form, should be furnished no later than thirty days before the start of the basis period for that assessment year.

The estimate should not be less than 85% of the revised estimate of tax payable for the immediately preceding year, or 85% of the estimate of tax payable for the immediately preceding year if no revised estimate is furnished.

Commencement of Operation (107C(4)-(4C)): If a company begins operations in an assessment year with a basis period of at least six months, it must submit its tax estimate within three months from the commencement of operations (107C(4)(a)).

Subsections (2) and (3) apply starting from the second year of assessment for such entities (107C(4)(b)).

However, if a resident company incorporated in Malaysia commences operations, certain subsections (1), (2), and (3) do not apply under specific conditions (107C(4A)).

Subsection (4B) outlines conditions where the provisions of subsection (4A) do not apply, primarily related to the ownership structure of the company.

“Related company” in subsection (4C) is defined as a company with a paid-up capital in respect of ordinary shares exceeding two million and five hundred thousand ringgit at the beginning of the basis period for an assessment year.

Payment by Instalments (107C(5)-(8)): Entities furnishing estimates must pay the amount in equal monthly instalments, starting from the second month of the basis period (107C(5)).

For entities commencing operations, payments begin from the sixth month of the basis period (107C(6)).

Revised estimates can be provided in the sixth or ninth month of the basis period, with adjustments to instalments based on the differences between the revised estimate and prior instalments (107C(7)).

Electronic Submission (107C(7A)):

Estimates and revised estimates must be submitted electronically in accordance with section 152A.

Director General’s Discretion and Penalties (107C(8)-(11)):

The Director General may direct entities to make payments at different times and amounts, treated as a deemed revised estimate (107C(8)).

Penalties, including a ten percent increase, apply for unpaid instalments (107C(9)).

Additional penalties apply if the tax payable under an assessment exceeds the estimate by more than thirty percent (107C(10)).

Further penalties apply if no estimate is furnished, and no prosecution is initiated under section 120, and tax is payable based on assessment (107C(10A)).

Remission and Collection (107C(11)-(11B)):

The Director General has discretion to remit penalties in certain circumstances (107C(11)).

Nothing in this section prevents tax collection or enforcement according to sections 103 and 106 (107C(11A)).

In case of a failure to make up accounts, penalties based on the prior accounting period remain recoverable (107C(11B)).

Definitions (107C(12)):

Defines “due date” as the fifteenth day of a calendar month.

“Revised estimate” refers to an estimate made in the ninth month of the basis period or, if not made, the revised estimate in the sixth month of the basis period.

Finance (No. 2) Bill 2023

The proposed amendments to Section 107C of the Income Tax Act 1967 introduce changes related to the estimation of tax payable and payment by instalments for companies, with a specific focus on ownership structures and the disposal of capital assets.

Let’s break down the amendments and discuss their potential tax impacts:

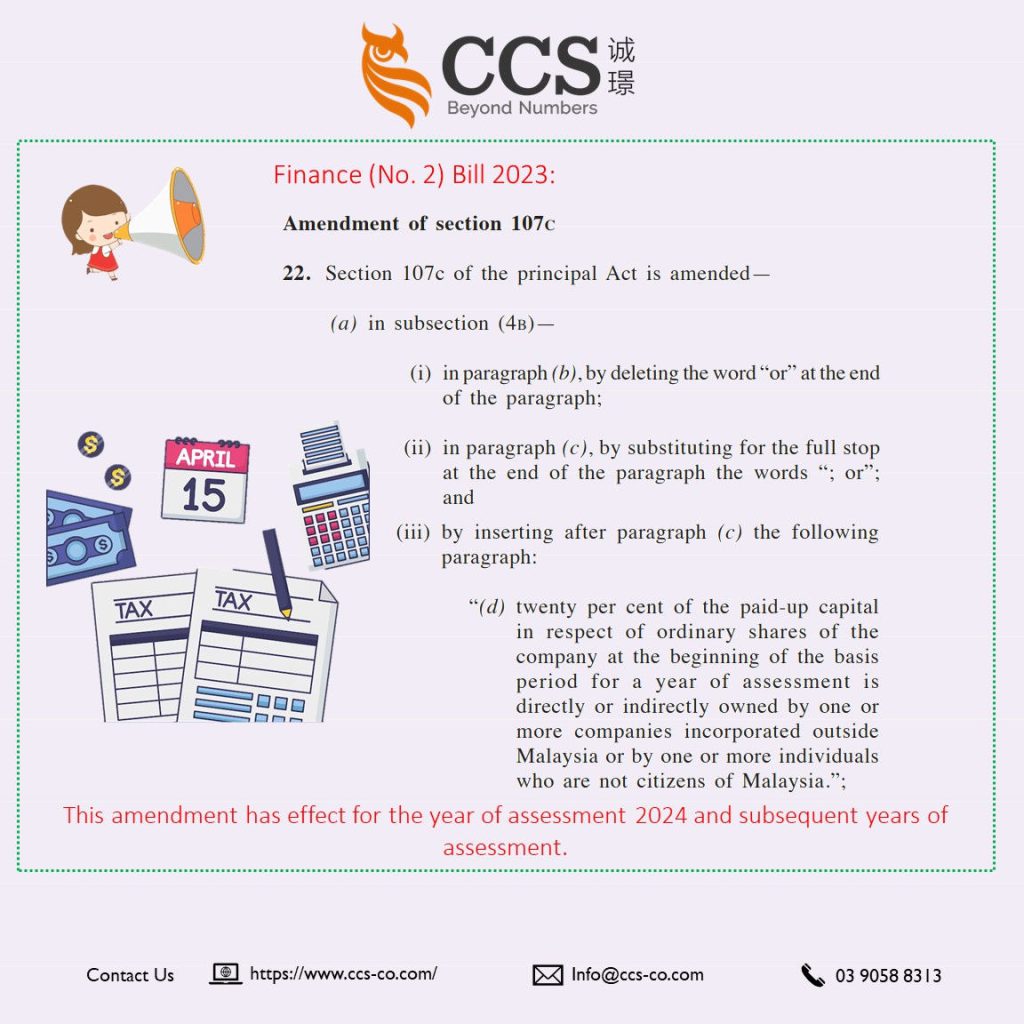

1. Amendment to Subsection 107C(4B):

Nature of the Amendment:

- Paragraphs (b) and (c) of subsection (4B) are modified.

- Paragraph (b) sees a change in punctuation.

- Paragraph (c) is extended, and a new paragraph (d) is added.

Summary:

- The amendment broadens the conditions under which the provisions of subsection (4A) do not apply.

- Previously, conditions were related to the ownership structure within Malaysia. Now, the amendment extends this to include cases where twenty percent of the paid-up capital in respect of ordinary shares is directly or indirectly owned by companies incorporated outside Malaysia or by individuals who are not citizens of Malaysia.

Tax Impact:

- Companies falling under the new conditions in paragraph (d) may be exempted from certain provisions of subsection (4A).

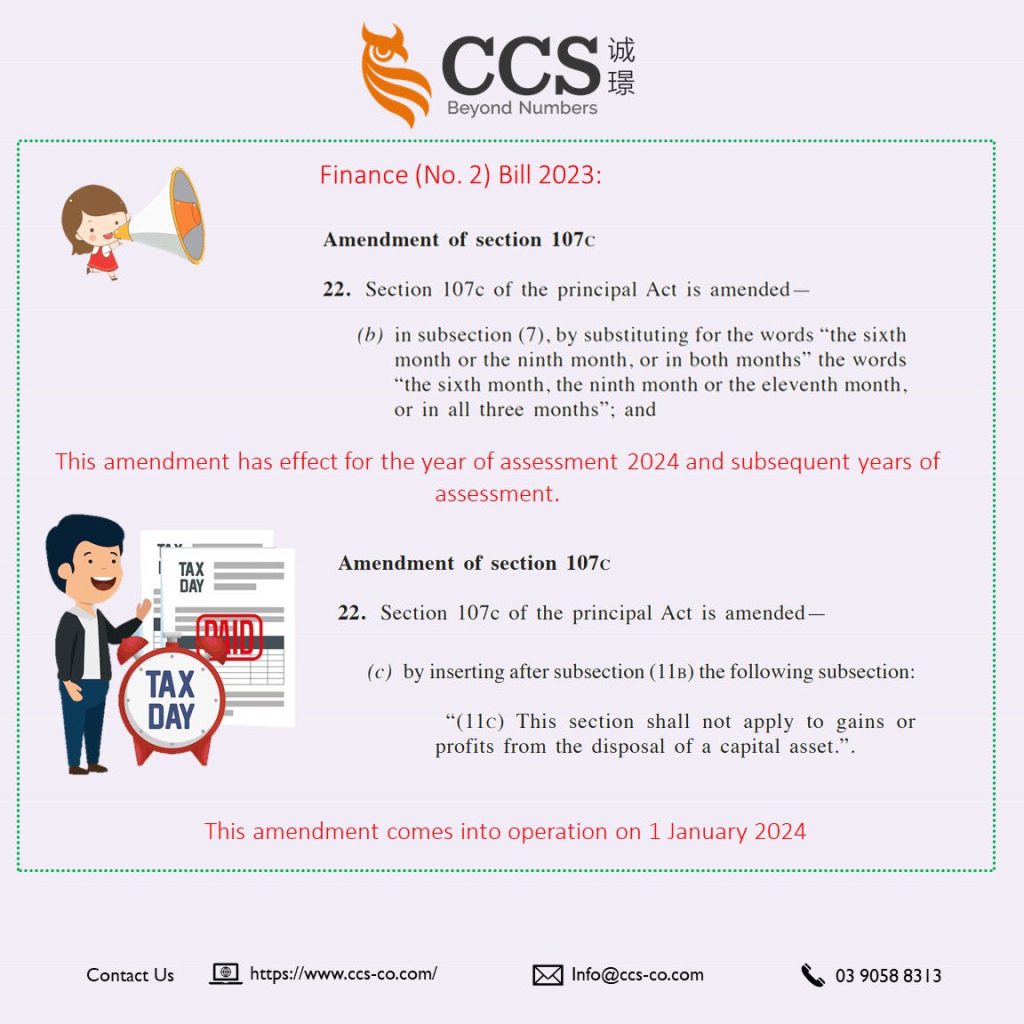

2. Amendment to Subsection 107C(7):

Nature of the Amendment:

- The amendment adjusts the wording related to the timing of revised estimates.

- The months specified for submitting revised estimates are expanded to include the eleventh month.

Summary:

- Entities can now furnish revised estimates in the sixth month, the ninth month, or the eleventh month of the basis period, or in all three months.

Tax Impact:

- This provides more flexibility for companies to adjust their tax estimates at additional points during the basis period. It allows for a more dynamic response to changes in financial circumstances.

3. Insertion of Subsection (11C):

Nature of the Amendment:

- A new subsection (11C) is added to Section 107C.

- This subsection explicitly states that Section 107C shall not apply to gains or profits from the disposal of a capital asset.

Summary:

- The amendment carves out an exception for gains or profits from the disposal of capital assets from the provisions of Section 107C.

Tax Impact:

- Gains or profits from the disposal of capital assets are excluded from the framework of Section 107C. This might impact how such gains are assessed, allowing for different treatment outside the scope of this section.

Overall, these amendments reflect changes in ownership criteria and provide more timing options for revised estimates.

The new subsection (11C) ensures that gains or profits from the disposal of capital assets are not subject to the provisions of Section 107C.

It is advisable for companies to consult with tax professionals to assess the implications for their particular situations.