Section 103 of the Income Tax Act outlines the provisions related to the payment of tax.

Here are the key points:

Due Date for Tax Payment (Subsections 1, 1A, and 2):

Tax payable under an assessment for a year of assessment is generally due and payable on the due date.

The due date varies based on the type of taxpayer (e.g., company, individual) and is specified in subsection 12.

Immediate Payment for Certain Assessments (Subsection 2):

For specific assessments under sections 90(3), 91, 92, 96A, or increased assessments under section 101(2), the tax is due and payable on the person assessed at the place specified in the notice.

Late Payment Penalties (Subsections 3, 5, and 7):

If tax is not paid by the due date, late payment penalties may apply.

The penalty is ten per cent of the unpaid tax and is recoverable as if it were tax due and payable under the Act.

Instalment Payment Option (Subsection 7):

The Director General has the discretion to allow tax to be paid by instalments, and default in payment of any instalment may lead to the imposition of penalties.

Remission of Penalties (Subsection 9):

The Director General may, for good cause shown, remit the whole or any part of the penalty imposed for late payment.

Collection from Husband or Wife (Subsection 10):

In cases where section 45(2) applies for a year of assessment, the tax attributable to the total income of the wife or husband may be collected from the electing spouse.

Formula for Determining Tax Portion (Subsection 11):

A formula is provided to determine the portion of tax attributable to the total income of the electing spouse in cases where section 45(2) applies.

Definition of Due Date (Subsection 12):

The “due date” is defined based on the type of taxpayer, specifying the last day for payment.

- in the case of a company, trust body, co-operative society or limited liability partnership the last day of the seventh month from the date following the close of the accounting period;

- in the case of a person referred to under paragraph 77(1)(a), 30 June in the year following the year of assessment; and

- in any other case other than the cases referred to in paragraphs (a) and (b), 30 April in the year following the year of assessment.

These provisions aim to ensure the timely payment of taxes, provide penalties for late payments, and offer some flexibility through instalment options. The section also addresses specific scenarios, such as joint assessments for spouses.

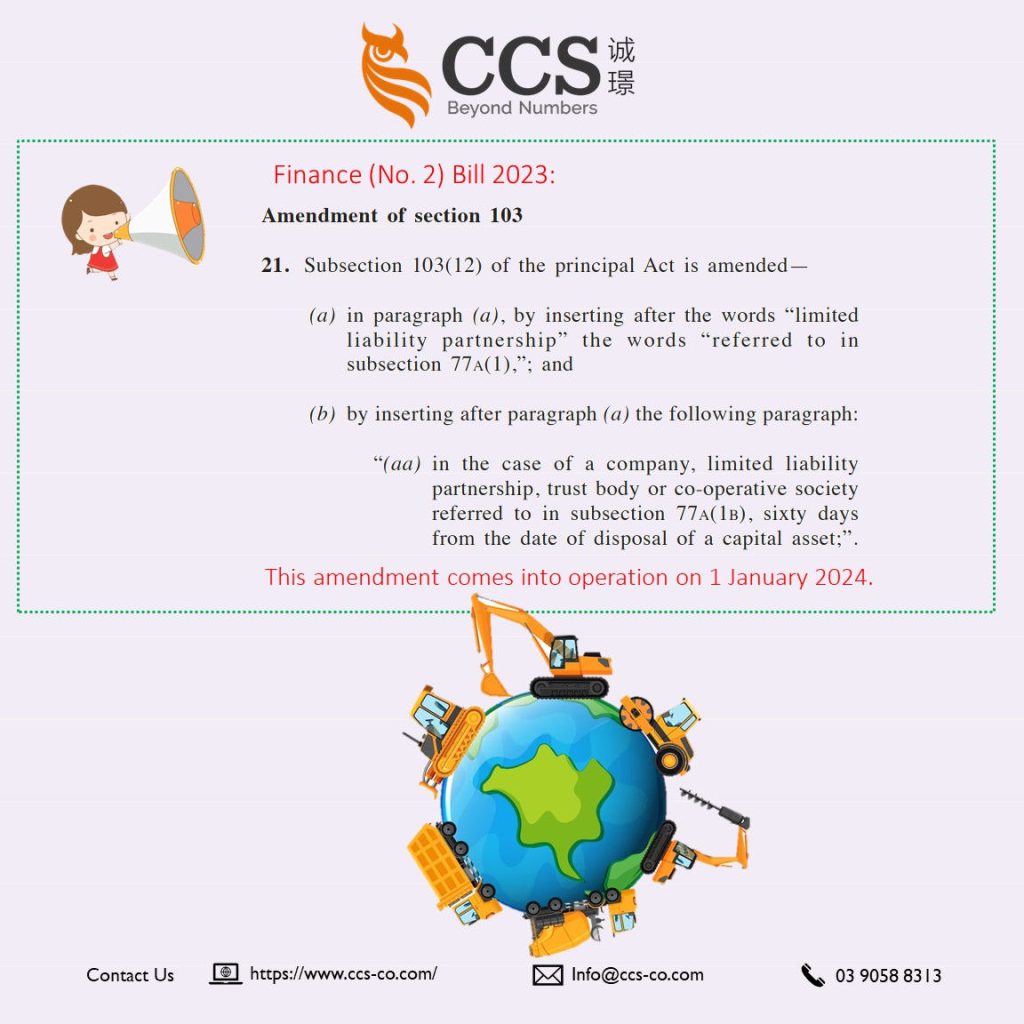

Finance (No. 2) Bill 2023

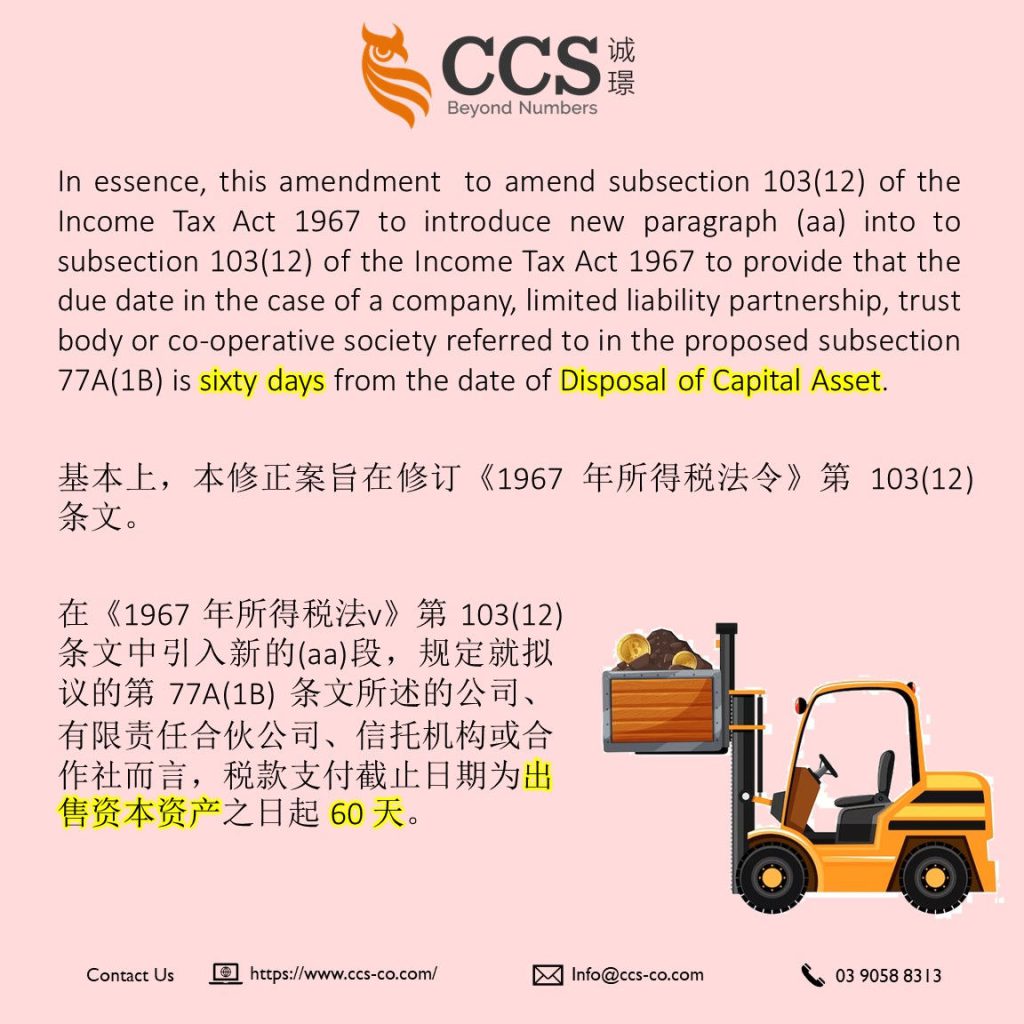

The proposed amendment to Subsection 103(12) of the Income Tax Act, as outlined in the Finance (No. 2) Bill 2023, introduces changes to the due date for certain taxpayers, specifically those mentioned in subsections 77A(1) and 77A(1B).

Let’s break down the amendment and discuss its tax implications:

Insertion in Subsection 103(12) Paragraph (a):

- After the words “limited liability partnership” in paragraph (a), the amendment includes the phrase “referred to in subsection 77A(1),”.

- This implies that the due date specified in paragraph (a) now applies to entities falling under subsection 77A(1).

Insertion of Paragraph (aa):

- A new paragraph (aa) is introduced after paragraph (a). This paragraph pertains to the due date for tax payment for companies, limited liability partnerships, trust bodies, or co-operative societies referred to in subsection 77A(1B).

- The due date for this category is set as “sixty days from the date of disposal of a capital asset.”

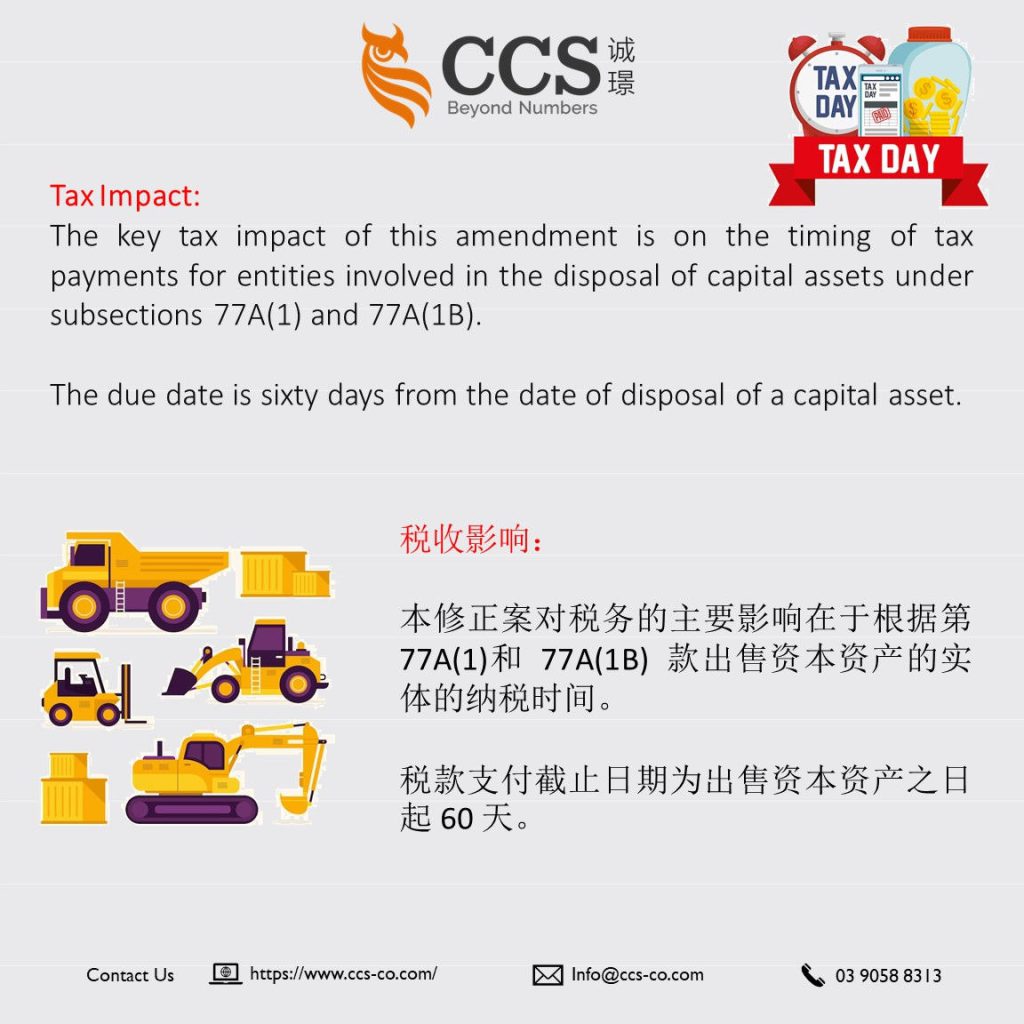

Tax Impact:

The key tax impact of this amendment is on the timing of tax payments for entities involved in the disposal of capital assets under subsections 77A(1) and 77A(1B).

The due date is sixty days from the date of disposal of a capital asset.

Conclusion:

In summary, the amendment aims to tailor the due date provisions for specific entities, recognising the unique circumstances related to the disposal of capital assets.

The sixty-day extension offers practicality in managing tax obligations for entities involved in such transactions.