Under Para 13(1) of the Income Tax Act 1967, The income of—

(a) an institution, organisation or fund approved for the purposes of section 44(6) so long as the approval remains in force;

(b) a religious institution or organisation in respect of any contribution received for charitable purposes in the basis year for a year of assessment provided such institution or organisation is not operated or conducted primarily for profit and is established in Malaysia exclusively for the purpose of religious worship or the advancement of religion; or

(c) an appropriate religious authority or a body or a public university approved for the purposes of subsection 44(11D) in respect of any wakaf or endowment received including the income derived therefrom in the basis period for a year of assessment, so long as the approval remains in force.

is exempted from Tax.

In summary, these provisions grant a tax exemption to the specified entities and organisations, provided they meet the outlined criteria and have the necessary approvals in force.

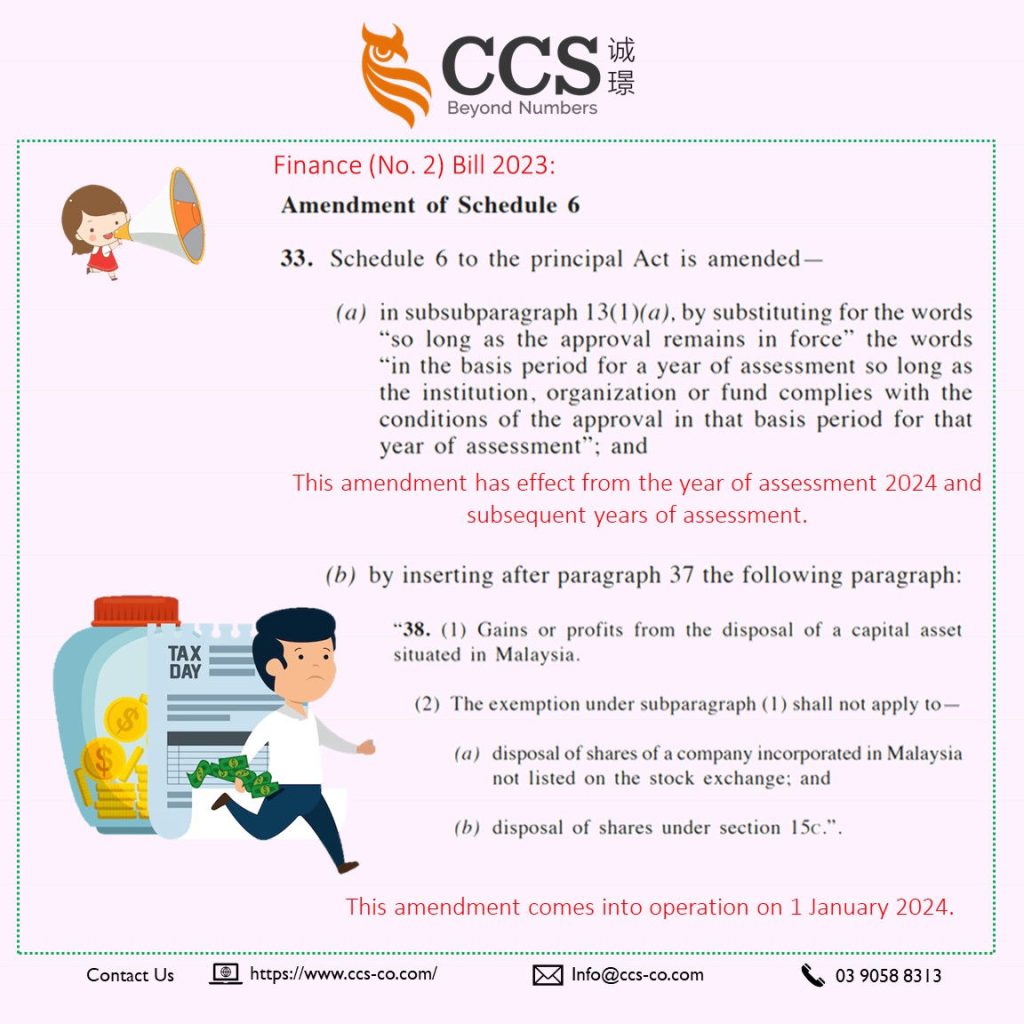

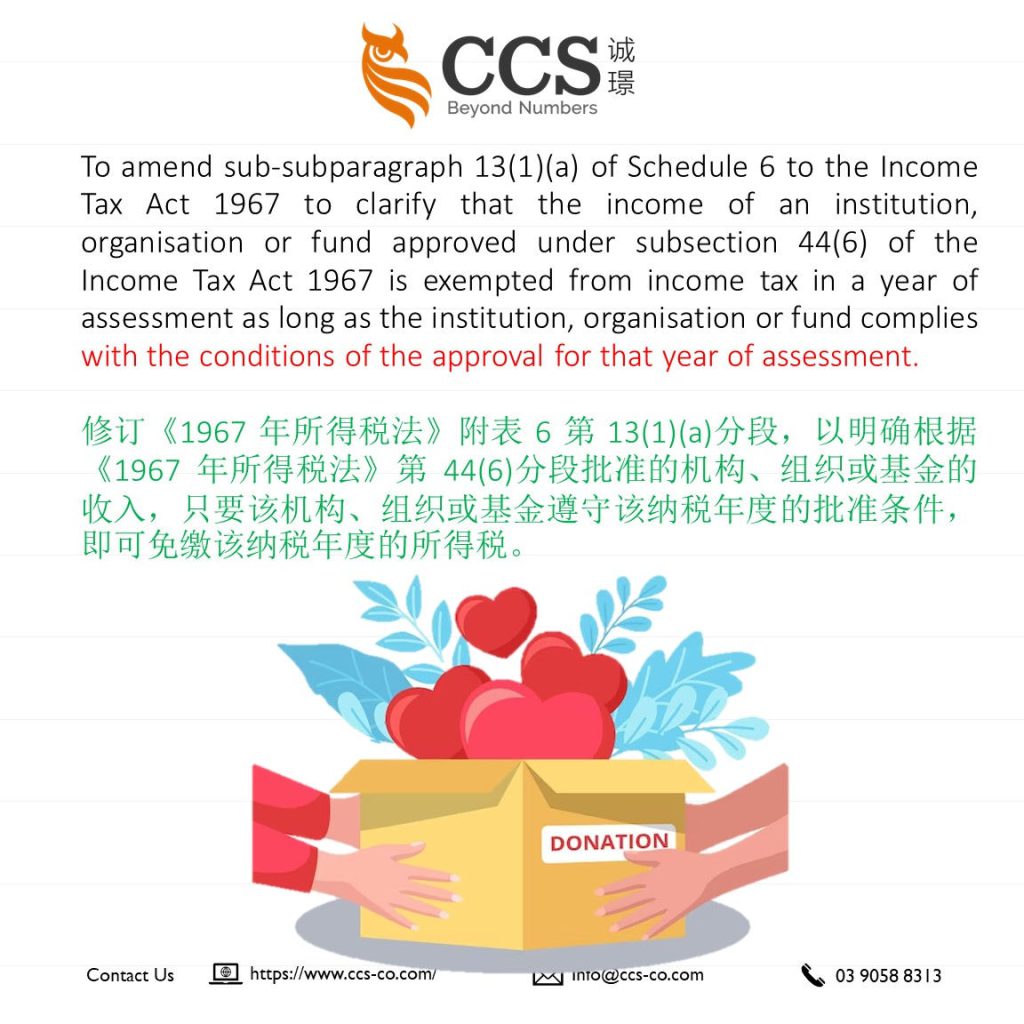

The proposed amendment to Schedule 6 of the Income Tax Act 1967 introduces an amendment to sub-subparagraph 13(1)(a), specifically addressing the conditions for tax exemption applicable to institutions, organisations, or funds approved under section 44(6).

The amendment replaces the existing wording “so long as the approval remains in force” with the phrase “in the basis period for a year of assessment so long as the institution, organisation, or fund complies with the conditions of the approval in that basis period for that year of assessment.”

This amendment signifies a change in the temporal aspect of compliance.

Previously, the tax exemption was contingent on the approval remaining in force over time.

The proposed amendment now ties the exemption to compliance with approval conditions during the specific basis period for a given year of assessment.

Example: Consider an educational institution approved under section 44(6) for tax exemption.

Under the previous wording, the institution enjoyed tax exemption as long as the approval was valid. With the proposed amendment, the institution must adhere to the approval conditions during the basis period for a specific year of assessment to qualify for tax exemption.

Tax Impact:

The impact of this amendment is that institutions, organisations, or funds approved under section 44(6) must ensure compliance with approval conditions during the relevant basis period to maintain their tax-exempt status for a specific year of assessment.

Failure to comply with the conditions during the specified basis period may result in the loss of tax exemption for that particular year.

Finance (No. 2) Bill 2023 also proposed to insert the following paragraph after paragraph 37:

“38. (1) Gains or profits from the disposal of a capital asset situated in Malaysia.

(2) The exemption under subparagraph (1) shall not apply to—

- disposal of shares of a company incorporated in Malaysia not listed on the stock exchange; and

- disposal of shares under section 15C.”.

The proposed insertion of paragraph 38 in the Finance (No. 2) Bill 2023 addresses the taxation of gains or profits from the disposal of a capital asset in Malaysia.

Below is an explanation, example, and the tax impact:

Explanation:

- Gains or Profits Inclusion: Paragraph 38(1) indicates that gains or profits derived from the disposal of a capital asset located in Malaysia will be exempted from taxation.

- Exemption Limitation: However, the exemption provided under subparagraph (1) is limited, and the subsequent conditions specify instances where the exemption will not apply.

- Exclusions from Exemption:

- Disposal of Shares: The exemption does not apply to the disposal of shares of a company incorporated in Malaysia that is not listed on the stock exchange.

- Disposal of Shares under Section 15C: The exemption is also not applicable to the disposal of shares under Section 15C.

Example:

Consider an individual who sells shares of a Malaysian company not listed on the stock exchange.

Under the proposed paragraph 38, the gains or profits from this disposal would not qualify for the exemption, and the individual would be subject to taxation on the capital gains.

Tax Impact:

The tax impact of this amendment is that gains or profits from the disposal of certain capital assets situated in Malaysia, specifically shares of non-listed Malaysian companies and shares under section 15C, will no longer be exempt.

Taxpayers involved in such transactions must be aware of these changes as they may increase tax liability for the specified disposals.