“Section 138 Certain Material to be Treated as Confidential” is read as follows:-

Section 138(1) [Classified person]

Subject to this section, every classified person shall regard and deal with classified material as confidential; and, if he is an official, he shall make and subscribe before the prescribed authority a declaration in the prescribed form that he will do so.

除本条另有规定外,每名机密人员均须将机密材料视为机密并订明处理;如他是官员,则须在订明清单前以订明表格作出签署注明声明及表明他会这样做。

Section 138(2) [Production and use of classified material]

No classified material shall be produced or used in court or otherwise except-

- for the purposes of this Act or another tax law;

- in order to institute or assist in the course of a prosecution for any offence committed in relation to tax or in relation to any tax or duty imposed by another tax law; or

- with the written authority of the Minister or of the person or partnership to whose affairs it relates.

不得在法庭或其他场合出示或使用机密材料,除非

- 为本法或其他税法的目的;

- 为了起诉或协助起诉与税收有关的任何罪行或与其他税法规定的任何税收或义务有关的罪行;或

- 获得部长或与其事务有关的个人或合伙企业的书面授权。

Section 138(3) [Limit on Court’s authority]

No official shall be required by any court—

- to produce or disclose classified material which has been supplied to him or another official otherwise than by or on behalf of the person or partnership to whose affairs it relates; or

- to identify the person who supplied that material.

法院不得要求任何官员:-

- 出示或披露由其本人或另一名官员提供的机密材料,但与该材料有关的个人或合伙企业或代表该个人或合伙企业提供的机密材料除外;或

- 确认提供材料者的身份。

Section 138(4) [Disclosure to Auditor-General: Director General’s publication of offenders]

Nothing in this section shall prevent—

- the production or disclosure of classified material to the Auditor-General (or to public officers under his direction and control) or the use of classified material by the Auditor-General, to such an extent as is necessary or expedient for the proper exercise of the functions of his office;

- the Director General from publicizing, from time to time in any manner as he may deem fit, the following particulars in respect of a person who has been found guilty or convicted of any offence under this Act or dealt with under subsection 113(2) or section 124—

- the name, address and occupation or other description of the person;

- such particulars of the offence or evasion as the Director General may think fit;

- the year or years of assessment to which the offence or evasion relates;

- the amount of the income not disclosed;

- the aggregate of the amount of the tax evaded and penalty (if any) charged or imposed;

- the sentence imposed or other order made:

Provided that the Director General may refrain from publicizing any particulars of any person to whom this paragraph applies if the Director General is satisfied that, before any investigation or inquiry has been commenced in respect of any offence or evasion falling under section 113 or 114, that person has voluntarily disclosed to the Director General or to any authorized officer complete information and full particulars relating to such offence or evasion.

本条的任何规定不得妨碍:-

- 向审计长(或受审计长指示及控制的公职人员)提供或披露机密资料,或审计长在适当履行其职能要求或合宜的范围内使用机密资料;

- 总监可以不时地以他认为合适的任何方式,公布被认定或判定犯有本法所规定的任何罪行或根据第 113(2)分节或第 124 节被处理的人的下列细节

- 此人的姓名、地址和职业或其他描述;

- 总监认为合适的有关犯罪或逃税的细节;

- 罪行或逃税行为所涉及的一个或多个评税年度;

- 未披露的收入数额;

- 所逃税款及被控或被处罚款(如有)的总额;

- 作出的判决或其他命令:

但如果总监确信,在开始对第 113 或 114 条所述罪行或逃税行为进行调查或查询之前,该人已自愿向总监或任何受权官员披露与该罪行或逃税行为有关的完整资料和全部详情,则总监可避免公布本段所适用的任何人的任何详情。

Section 138(5) [Definitions]

In this section—

“another tax law” means any Ordinance wholly repealed by this Act, any written law relating to estate duty, film hire duty, payroll tax or turnover tax and any other written law declared by the Minister by statutory order to be another tax law for the purposes of this section;

“classified material” means any return or other document made for the purposes of this Act and relating to the income of any person or partnership and any information or other matter or thing which comes to the notice of a classified person in his capacity as such;

“classified person” means—

- an official;

- the Auditor-General and public officers under his direction and control;

- any person advising or acting for a person who is or may be chargeable to tax, and any employee of a person so acting or advising if he is an employee who in his capacity as such has access to classified material; or

- any employee of the Inland Revenue Board of Malaysia;

“official” means a person having an official duty under or employed in carrying out the provisions of this Act.

在本条中 :-

“另一税法 “是指被本法案完全废除的任何法令,与遗产税、电影租用税、工资税或营业税有关的任何成文法,以及部长通过法定命令宣布为本条所指的另一税法的任何其他成文法;

“机密材料 “是指为本法案的目的而制作的与任何人或合伙企业的收入有关的任何申报表或其他文件,以及机密人员以机密人员身份注意到的任何信息或其他事项或事物;

“机密人员 “指

- 官员

- 审计长及其领导和控制下的公职人员;

- 为应纳或可能应纳税款的人提供咨询意见或为其行事的任何人,以及如此行事或提供咨询意见的人的任何雇员(如果该雇员以此种身份接触机密材料);或

- 马来西亚税务局的任何雇员;

“官员 “是指根据本法令负有官方职责或受雇执行本法令规定的人员。

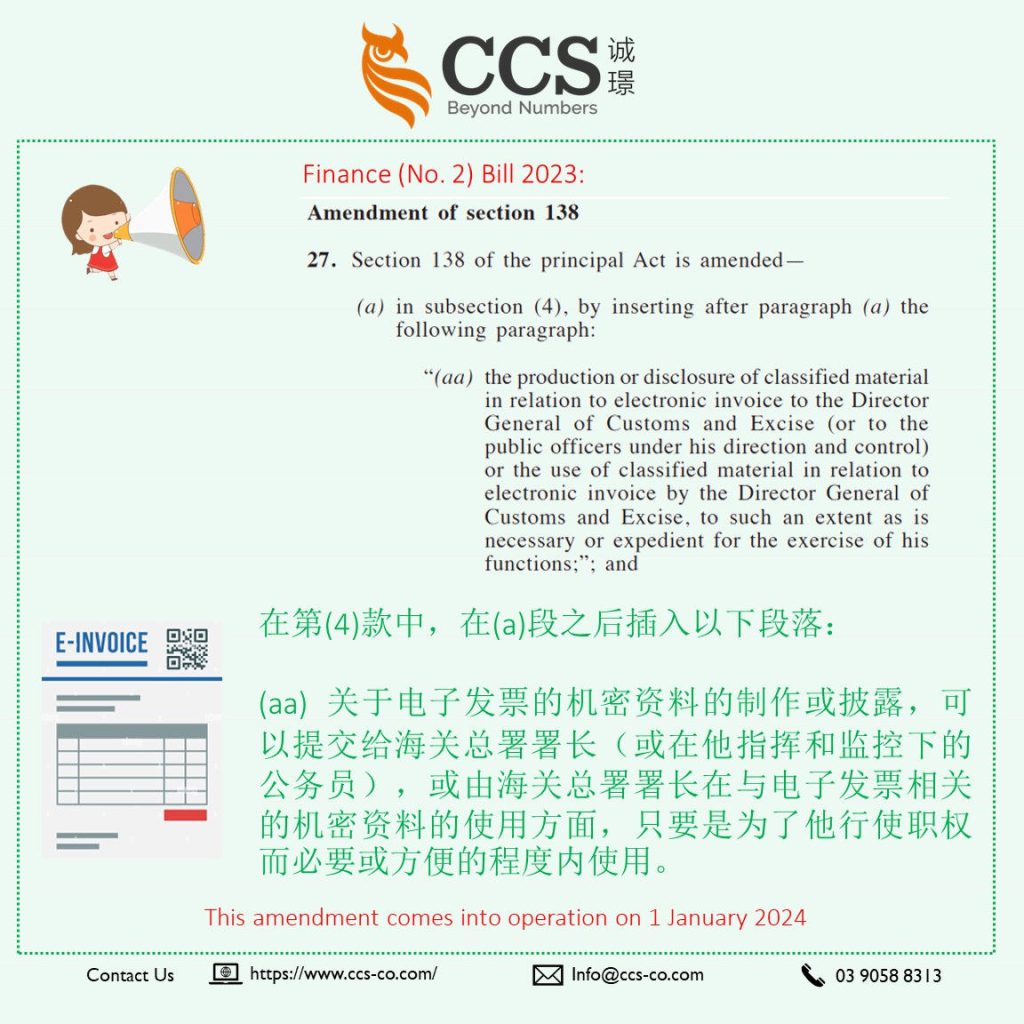

The proposed amendment to section 138 introduces changes in relation to classified material, specifically concerning electronic invoices.

In subsection (4), a new provision (paragraph (aa)) is added, allowing the production or disclosure of classified material related to electronic invoices to the Director General of Customs and Excise or public officers under his direction.

It also permits the use of classified material in relation to electronic invoices by the Director General for the exercise of his functions.

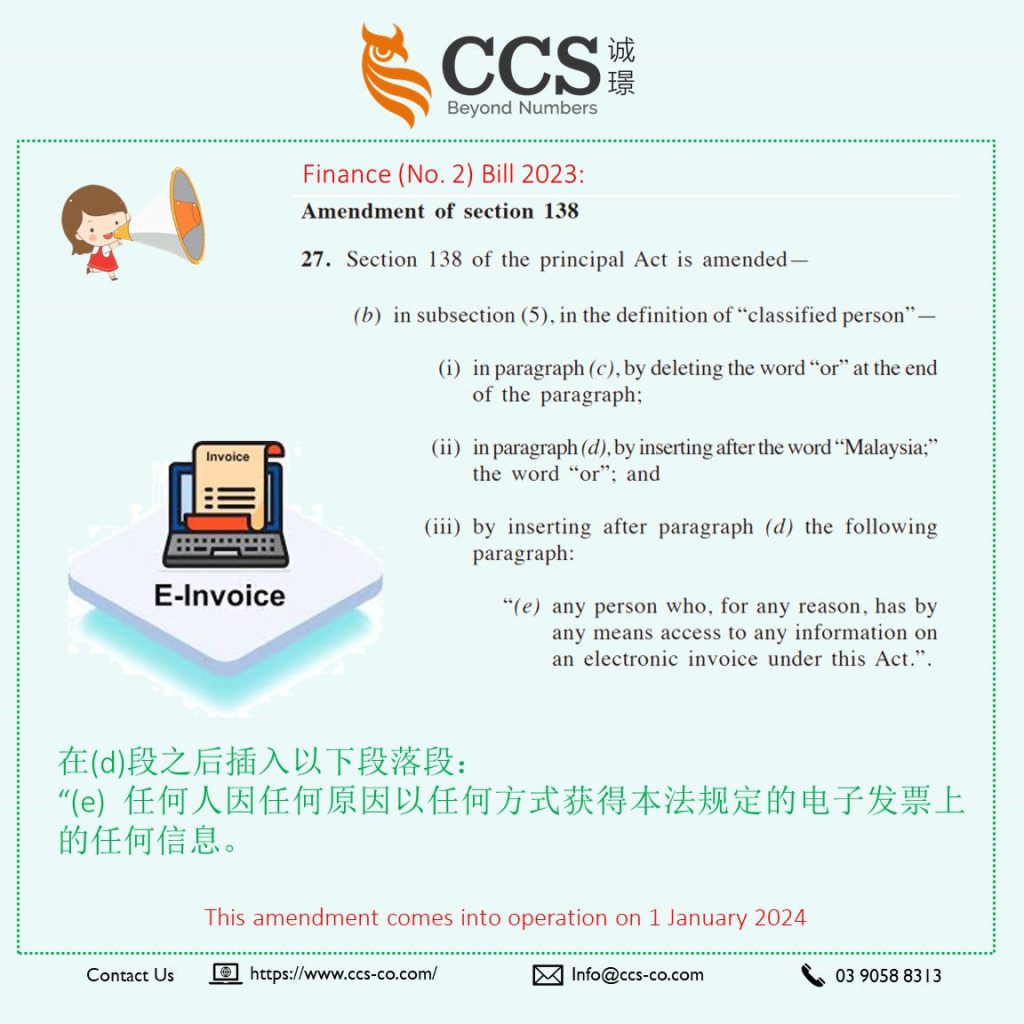

In subsection (5), the definition of “classified person” is expanded to include any person who, for any reason, has access to any information on an electronic invoice under this Act.

These amendments expand the scope of individuals who may handle classified material related to electronic invoices and outline the circumstances under which such handling is permissible.

The tax impact of these amendments is to enhance the regulatory framework around electronic invoices, allowing relevant authorities access to classified material for effective enforcement and oversight.

It aligns with the modernisation of tax processes, particularly concerning electronic documentation, and aims to ensure compliance and transparency in handling electronic invoice-related information.