IRBM’s Response to CTIM on Forms CP 22 / CP 22A

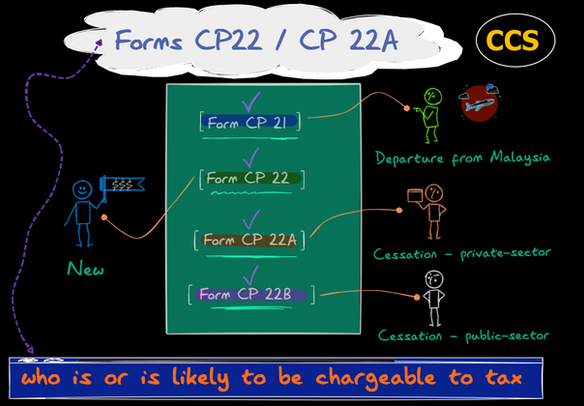

Mandatory adoption of Prescribed Forms CP 21, CP 22, CP 22A and CP 22B effective from 1 January 2022 Effective January 1, 2021, under the amendments to subsections 83 (2), (3), and (4) of the Income Tax Act 1967, Forms CP 21, CP 22, CP 22A, and CP 22B must be submitted by the employers […]

The Difference between a Contractor / Freelancer and an Employee

1. The decision to report a person’s income on Form E is based on whether or not he is an employee, not on whether there are EPF or SOCSO contributions or not. 2. As a result, the employer must determine if the individual is an employee, a contractor, or a so-called freelancer before proceeding. 🌻🌻🌻🌻🌻🌻🌻🌻🌻 […]

CP22, PCB, Form E & EA, CP22A, CP21: Employer’s Liability to Employees for Tax Purposes

1. Employers have distinct responsibilities for tax purposes at various periods of an employee’s life, from the time he first joins the company until he leaves or dies, depending on the circumstances. 🌻🌻🌻🌻🌻🌻🌻🌻🌻 1. 在税务上,从员工入职开始一直到他离职或去世,在不同的阶段,雇主都有着不同的责任。 10

Tax Treatment on Final Tax under Section 77C(1)

1. On 3 May 2021, the LHDNM issued a Practice Note to explain the Final Tax’s tax treatment under the provisions of subsection 77C (1) of the Income Tax Act 1967 (ACP). 2. The Income Tax Return Form (ITRF / BNCP) is optional to be submitted to IRBM by taxpayers with one Employment Income ONLY […]

Audit Framework For Employer: Effective from October 1, 2021

1. The Audit Framework for Employer was released by Lembaga Hasil Dalam Negeri (LHDNM) on October 1, 2021, and went into effect on October 1, 2021. 2. This Framework lays forth the rights and duties of audit officers, employers, and tax agents, with the goal of ensuring that employer audits are carried out fairly, openly, […]