The Inland Revenue Board of Malaysia (IRBM) has issued their responses dated 16 February 2023 to CTIM members’ issues dated 18 January 2023 on the following: –

- Deduction for Expenses in relation to the Cost of Detection Test of Covid-19 for Employees [P.U. (A) 404/2021 as amended by P.U. (A) 291/2022]

- Qualifying Plant Allowances for Computers and Information Technology Equipment, and Cost of Provision of Computer Software [P.U. (A) 187/1998 and P.U. (A) 272/1999]

- Income Tax (Deduction For Incorporation Expenses) Rules 2003 [P.U. (A) 475/2003] as amended by P.U. (A) 472/2005

- Amended Guidelines On Tax Deduction Of Secretarial Fees And Tax Filing Fees From YA 2022 Onwards dated 17 August 2022

In this article, we will see IRBM’s response regarding item no. 1, which is the Deduction for Expenses in relation to the Cost of Detection Tests for Covid-19 for Employees [P.U. (A) 404/2021 as amended by P.U. (A) 291/2022].

Income Tax (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) Rules 2021 [P.U. (A) 404/2021]

On 20th October 2021, the Income Tax (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) Rules 2021 [P.U. (A) 404/2021] were gazetted.

You may read the above Rules in full at the official website of the Attorney-General’s Chambers or download it from the attachment below:-

These Rules have effect from the year of assessment 2021 and state that: –

- for a given year of assessment,

- Malaysian-resident employers can claim an additional deduction (in addition to any other deduction allowed under Section 33 of the ITA 1967)

- for the expenses incurred on COVID-19 detection tests conducted for their employees

- between 1st January 2021 and 31st December 2021

- when calculating their adjusted income from the business.

To claim this additional deduction, the employer must produce a receipt and certification issued by a medical practitioner registered with the Malaysian Medical Council or a medical practitioner registered outside Malaysia that confirms the provision of COVID-19 detection tests to their employees.

Income Tax (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) (Amendment) Rules 2022

On September 9, 2022, the Income Tax (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) (Amendment) Rules 2022 [P.U.(A) 291] were gazetted.

You may read the above Rules in full at the official website of the Attorney-General’s Chambers or download it from the attachment below:-

The rules state that for the purpose of claiming the additional deduction, the receipt and certification issued by a medical practitioner registered outside Malaysia can only be used for expenses incurred outside Malaysia.

In addition to this, employers can also produce receipts and COVID-19 detection test results of their employees issued by a health facility listed in the List of Laboratories Conducting RT-PCR Test for COVID-19 to the COVID-19 Management Guidelines in Malaysia No. 5/2020 (refer to Annex 4a) issued by the Ministry of Health Malaysia.

You may read the above List in full at the official website of the MOH or download it from the attachment below:-

These options can be used as an alternative to the certification by a medical practitioner registered with the Malaysian Medical Council. The Amendment Rules will apply from YA 2021 onwards.

Since the new Para 2(3)(b) which was inserted into the P.U. (A) 404/2021by the P.U. (A) 291/2022, reads as follows:

a receipt and result of the detection test of Coronavirus Disease 2019 (COVID-19) of its employees issued by a health facility listed in the List of Laboratories Conducting RT-PCR Test for Covid-19to the COVID-19 Management Guidelines in Malaysia No. 5/2020 issued by the Ministry of Health Malaysia which remains in force in relation to the costs of RT-PCR detection test incurred for its employee.

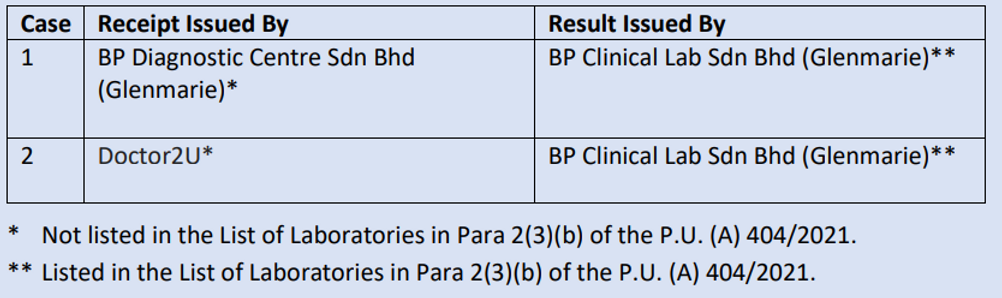

CTIM Comments: CTIM would like to seek IRBM’s confirmation that the following cases satisfy the provisions of Para2(3)(b) of the P.U.(A)404/2021:

Notes

- Doctor2U is an online platform that consolidates consultation and requests for medicines etc. Some companies with insurance use this platform.

- The screenshots of the receipts and the results can be viewed in the Appendix at the back of this paper.

It is a common practice, especially for smaller-scale clinics/health centres without a laboratory to conduct RT-PCR tests for Covid-19, to send their customers’ specimens to a third-party laboratory to complete the test. The laboratory will issue a receipt to their customers, i.e. the clinics/health centres, instead of the individual.

Feedback from LHDNM:

Referring to sub-sub para 2(3)(b) of the Income Tax Rules (Deduction for Expenses in relation to the Cost of Detection Test of Coronavirus Disease 2019 (COVID-19) for Employees) (Amendment) 2022 [P.U. (A) 291/2022], a receipt and COVID-19 detection test result issued by a health facility listed in the List of Laboratories Conducting RT-PCR Test for COVID-19 to the COVID-19 Management Guidelines in Malaysia No. 5/2020 issued by the Ministry of Health Malaysia (MOH) which is still in force, can be used as evidence for the RT-PCR test expenses incurred for an employee.

Based on the information provided, it was found that the COVID-19 detection test result submitted by CTIM, as attached, was issued by a private health facility listed under the List of Laboratories Conducting RT-PCR Test for COVID-19 to the COVID-19 Management Guidelines in Malaysia No.5/2020 issued by MOH.

Therefore, the expenses incurred by the employer for COVID-19 detection tests can be allowed as a deduction in determining the employer’s taxable income under P.U. (A) 291/2022.

Disclaimer:

The articles, templates, and other materials on our website are provided only for your reference.

While we strive to ensure that the information presented is current and accurate, we cannot guarantee the completeness, reliability, suitability, or availability of the website or its content, including any related graphics. Consequently, any reliance on this information is entirely at your own risk.

If you intend to use the content of our videos and publications as a reference, we recommend that you take the following steps:

- Verify that the information provided is current, accurate, and complete.

- Seek additional professional opinions, as the scope and extent of each issue, may be unique.

免责声明:

我们网站上的文章、模板和其他材料只供参考。

虽然我们努力确保所提供的信息是最新和准确的,但我们不能保证网站或其内容,包括任何相关图形的完整性、可靠性、适用性或可用性。因此,您需要承担使用这些信息所带来的风险。

如果你打算使用我们的视频和出版物的内容作为参考,我们建议你采取以下步骤:

- 核实所提供的信息是最新的、准确的和完整的。

- 寻求额外的专业意见,因为每个问题的范围和程度,可能是独特的。

Keep in touch with us so that you can receive timely updates

请与我们保持联系,以获得即时更新。

1. Website ✍️ https://www.ccs-co.com/ 2. Telegram ✍️ http://bit.ly/YourAuditor 3. Facebook ✍

- https://www.facebook.com/YourHRAdvisory/?ref=pages_you_manage

- https://www.facebook.com/YourAuditor/?ref=pages_you_manage

4. Blog ✍ https://lnkd.in/e-Pu8_G 5. Google ✍ https://lnkd.in/ehZE6mxy

6. LinkedIn ✍ https://www.linkedin.com/company/74734209/admin/