Exploring The IESBA Code Installment 7 – Inducements, Including Gifts and Hospitality

1. Inducements are defined in the IESBA Code as “anything used to influence the behaviour of another individual.” 2. At times, this influence occurs naturally as a result of commercial relationship development, but at other times, the incentive is intended to improperly encourage someone to act unethically. 3. Inducements can range from conventional business partners’ […]

Exploring The IESBA Code Installment 6- Conflicts of Interest

1. Conflicts of interest are the type of situation that is most directly associated with the principle of objectivity. All PAs are prohibited from compromising their professional or business judgement as a result of bias, a conflict of interest, or the undue influence of others, according to the Code. 2. Having conflicts of interest isn’t […]

Exploring The IESBA Code Installment 5 – Independence

1. Among other things, the International Independence Standards (IIS) mandate that professional accountants (PAs) in public practice be independent when doing audits, reviews, or other assurance engagement, in addition to adhering to the fundamental principles. 2. Independence is closely linked to the principles of integrity and objectivity and is an important element of serving the […]

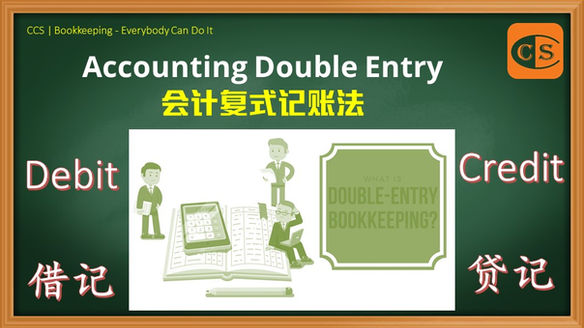

10 – Accounting Double Entry System

Bookkeeping – Everyone Can Do It 10 – Accounting Double Entry System – PDF 1. 在复式会计系统下,每项交易至少影响两个不同的账户。 2. 一个或多个账户应被借入 [Debited] ,一个或多个账户应被贷入 [Credited] ,以使账目平衡。 3. 当一项交易只有两个账户受到影响时,应直接进行分录。 4. 此外,当一项交易对两个以上的账户有影响时,应该建立一个复合分录。现在就让我们来看看这个例子。 5. 加入我们的 Telegram – http://bit.ly/YourAuditor 🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻 1. A double-entry accounting system is one in which every transaction impacts at least two different accounts. 2. One or more accounts should […]

Exploring The IESBA Code Installment 4 – The Conceptual Framework – Step 3

Exploring The IESBA Code Installment 4 – The Conceptual Framework – Step 3 Addressing Threats 1. The IESBA Code helps professional accountants (PAs) meet their responsibility to act in the public interest. 2. The Code provides a conceptual framework that specifies a three-step approach that all PAs can apply to identify, evaluate and address threats […]

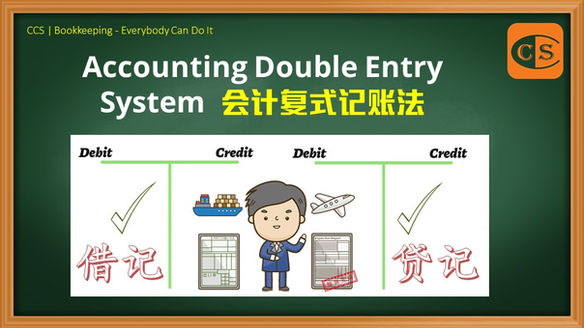

9 – Accounting Double Entry System

Bookkeeping – Everyone Can Do It 9 – Accounting Double Entry System – PDF 1. 在复式会计系统下,每项交易至少影响两个不同的账户。 2. 一个或多个账户应被借入 [Debited] ,一个或多个账户应被贷入 [Credited] ,以使账目平衡。 3. 当一项交易只有两个账户受到影响时,应直接进行分录。 4. 此外,当一项交易对两个以上的账户有影响时,应该建立一个复合分录。 5. 加入我们的 Telegram – http://bit.ly/YourAuditor 🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻 1. A double-entry accounting system is one in which every transaction impacts at least two different accounts. 2. One or more accounts should […]

Exploring The IESBA Code 3 – The Conceptual Framework-Evaluating Threats

1. Professional accountants are guided by a set of core principles that assist them in fulfilling their responsibilities to operate in the public’s best interests. 2. It is necessary to assess any potential challenges to compliance with the fundamental principles. 3. Therefore, the next step is to evaluate whether the identified threats are at an […]

1 – Malaysian Labour Law and Dispute Resolution System

Malaysian Labour Law and Dispute Resolution System – PDF 1. Employment relationships and industrial relations are inevitably fraught with conflict. Labor disputes can and do arise as a result of the conflict. 2. Next, we will share the necessary legal knowledge in the workplace through articles. 3. The Labor Act (EA) and Industrial Relations Act […]

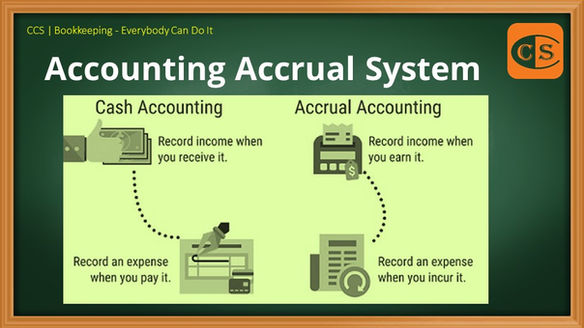

8 – Accounting Accrual System

Bookkeeping – Everyone Can Do It 8 – Accounting Accrual System – PDF 1. 现金会计系统 [Cash Accounting System] 和权责发生制会计系统 [Accrual Accounting System ] 是现有的两类会计系统。 2. 在现金会计系统中,只有在支付或收到款项时才会记录为费用和收入。因此,每一笔钱的流入都被认为是收入,每一笔钱的流出都被认为是支出。 3. 绝大多数公司都使用权责发生制会计系统。正因为如此,公司可以在收入和支出产生后立即记录,而不考虑什么时候才会收到或支付款项。 4. 加入我们的 Telegram – http://bit.ly/YourAuditor 🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻 1. A cash accounting system and an accrual accounting system are the two types of accounting systems available. 2. Only when […]

Exploring The IESBA Code Installment 2 – The Conceptual Framework – Step 1

1. When undertaking audits, reviews, and other assurance engagements, auditors and assurance practitioners are required to maintain independence. 2. They, too, must employ the conceptual framework in order to identify, evaluate, and address threats to independence. 3. Join our Telegram 👉 https://t.me/YourAuditor/2535 🌻🌻🌻🌻🌻🌻🌻🌻🌻🌻 1. 在进行审计、审查和其他鉴证业务时,审计师和鉴证从业人员必须保持独立性。 2. 他们也必须采用概念框架,以鉴定、评价和处理对独立性的威胁。 3. 加入我们的 Telegram 群 👉 https://t.me/YourAuditor/2535 🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳 EXPLORING […]